Download as PDF, PPTX

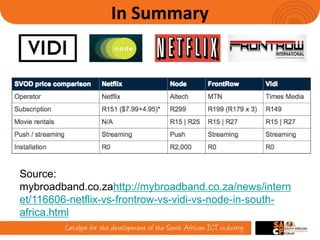

The document discusses the impact of over-the-top (OTT) services on traditional broadcasters and the strategies operators can adopt in response. It highlights the need for broadcasters to innovate and create partnerships to remain competitive amidst rising OTT threats, particularly in South Africa where broadband infrastructure is developing. The conclusion emphasizes the increasing competitiveness in the pay TV market as multiple operators explore launching OTT and on-demand offerings.