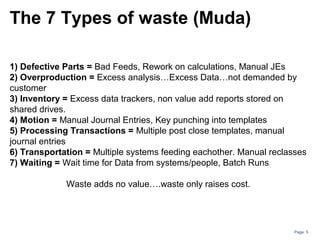

This document provides an overview of lean manufacturing principles from a finance perspective. It discusses how lean can help drive customer satisfaction by reducing waste, cycles, and improving delivery and quality. The key aspects of lean covered include eliminating the seven types of waste, 5S methodology to create a visual system, standard work, continuous improvement through kaizen, just-in-time production to eliminate waiting, and ensuring quality at the source. Examples of how these lean principles can be applied within finance functions are also provided.