Download as PDF, PPTX

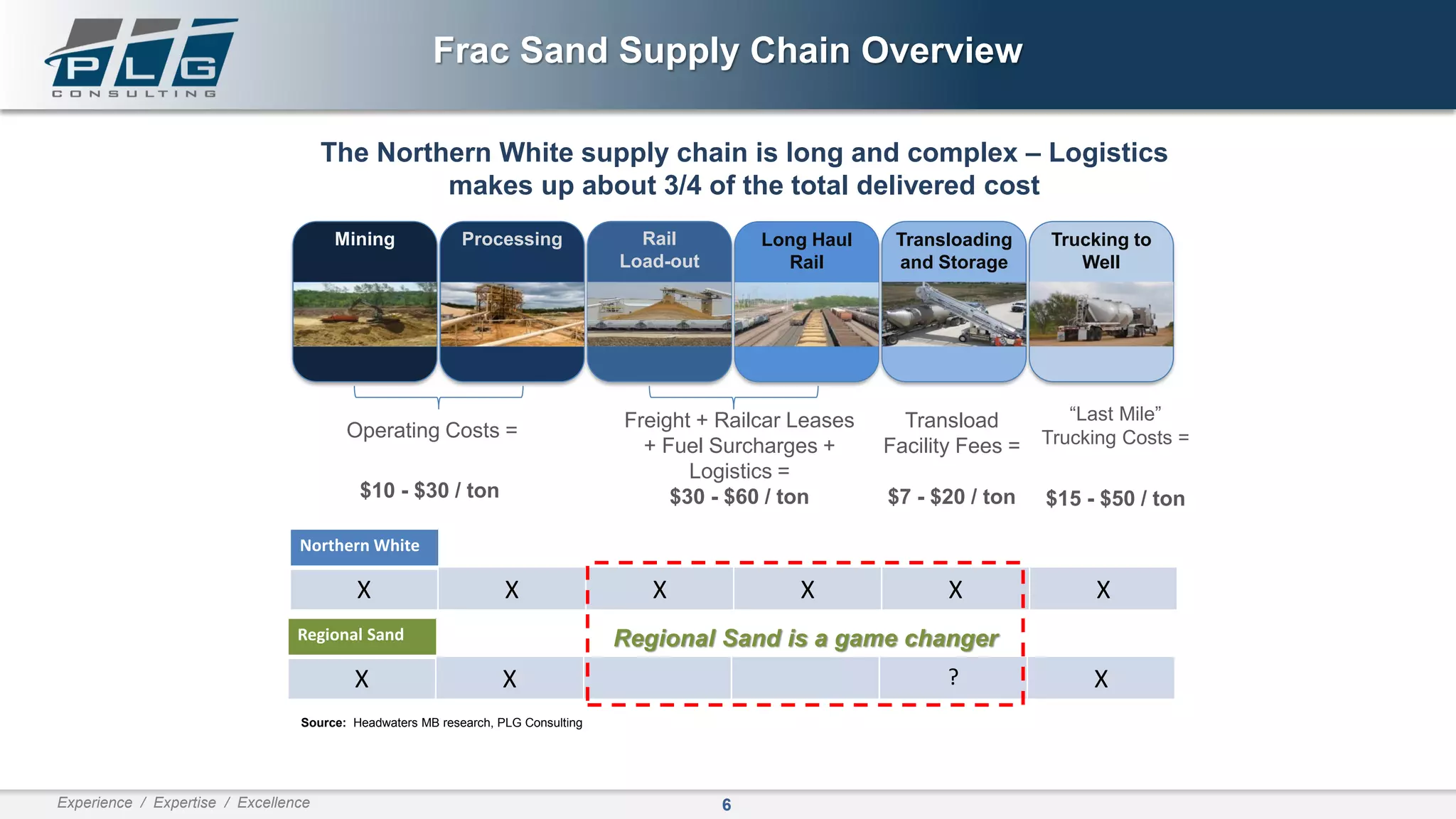

This document provides an overview and analysis of the frac sand supply chain and market. It discusses trends driving increased use of regional frac sand sources, such as higher intensity drilling increasing sand volumes used per well. The emergence of sand mines in the Permian Basin is a major development that could significantly reduce logistics costs. However, challenges for Permian sand include developing adequate infrastructure and workforce to support major volumes. The document also covers the impacts of new regulations on trucking and silica dust exposure.