Download as PDF, PPTX

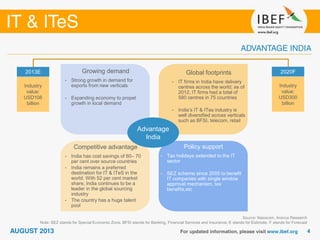

The Indian IT-BPM sector is projected to grow at a CAGR of 9.5% to reach USD 300 billion by 2020, driven by strong demand for exports and a large talent pool. India maintains a 52% share of the global outsourcing market, facilitated by cost competitiveness and significant foreign direct investment. The sector's growth is supported by evolving business dynamics, technological advancements, and increasing domestic demand, particularly from large enterprises and small to medium-sized businesses.