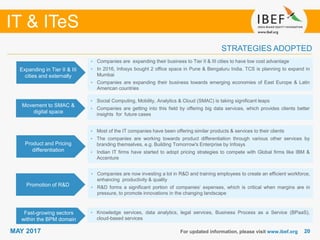

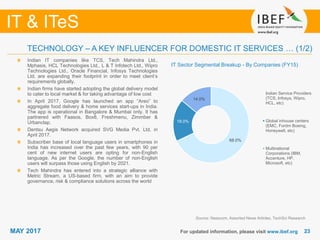

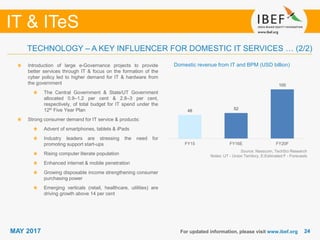

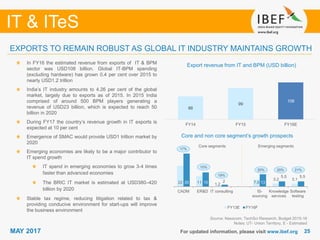

Download as PDF, PPTX

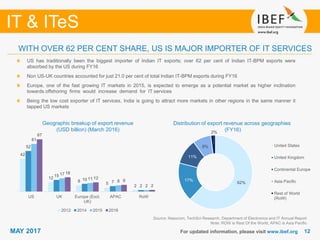

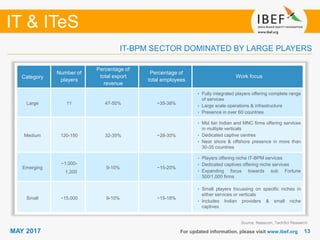

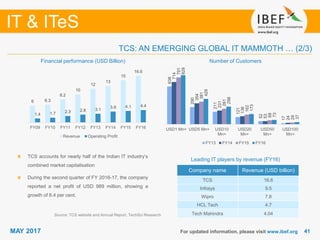

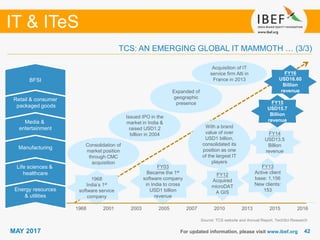

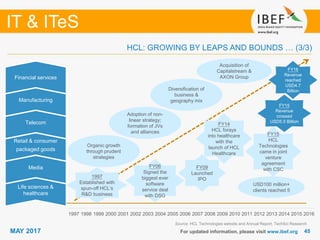

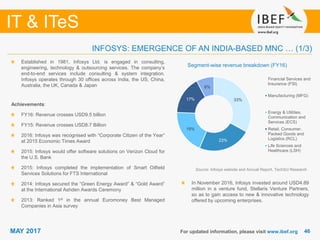

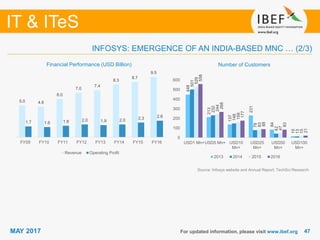

The IT & ITeS sector in India has grown significantly over the past decade and is expected to continue expanding rapidly. It is currently a $160 billion industry that exports over $100 billion annually, with the US being the largest importer of Indian IT services. The sector is dominated by a few large players that generate around half of total revenues. Important trends in the industry include the growth of global delivery centers, increased focus on R&D and engineering services, a shift to non-linear business models, and the adoption of new technologies. The industry is transforming from traditional outsourcing to offering broader digital solutions.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)