Download to read offline

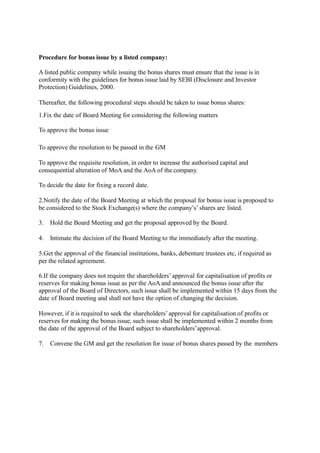

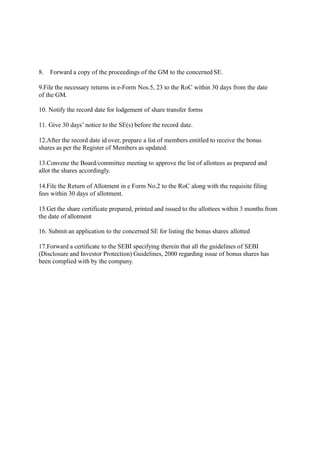

The document outlines SEBI guidelines for issuing bonus shares by listed and unlisted companies. For listed companies, SEBI guidelines must be followed which include issuing bonus shares from free reserves or share premium, not in lieu of dividends, and obtaining necessary shareholder approvals. The process for listed companies involves board approval, shareholder approval if required, intimating the stock exchange, and allotting shares within specified timelines. For unlisted companies, the process involves board approval, shareholder approval if required, filing necessary returns, and allotting shares within specified timelines as well.