Download as PDF, PPTX

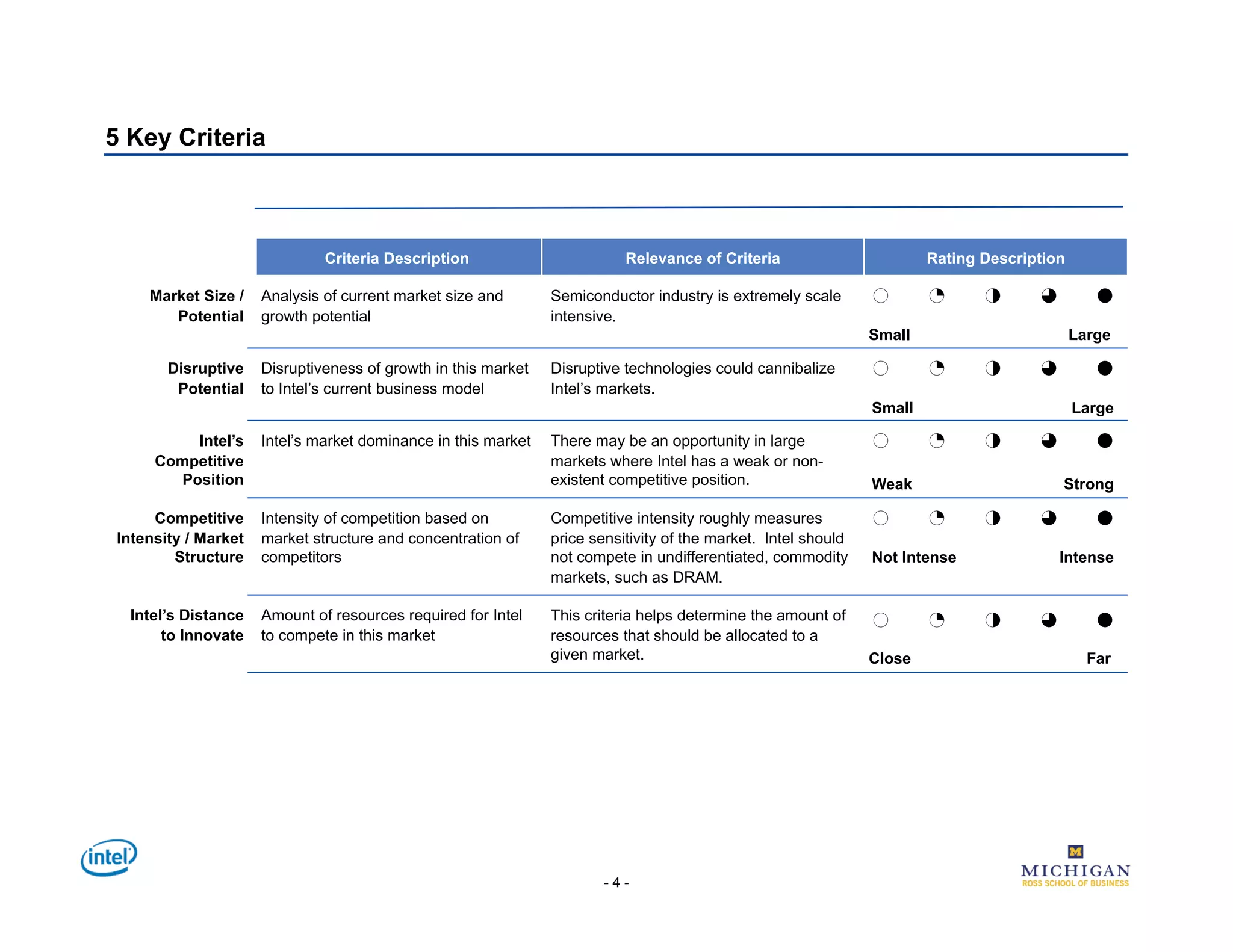

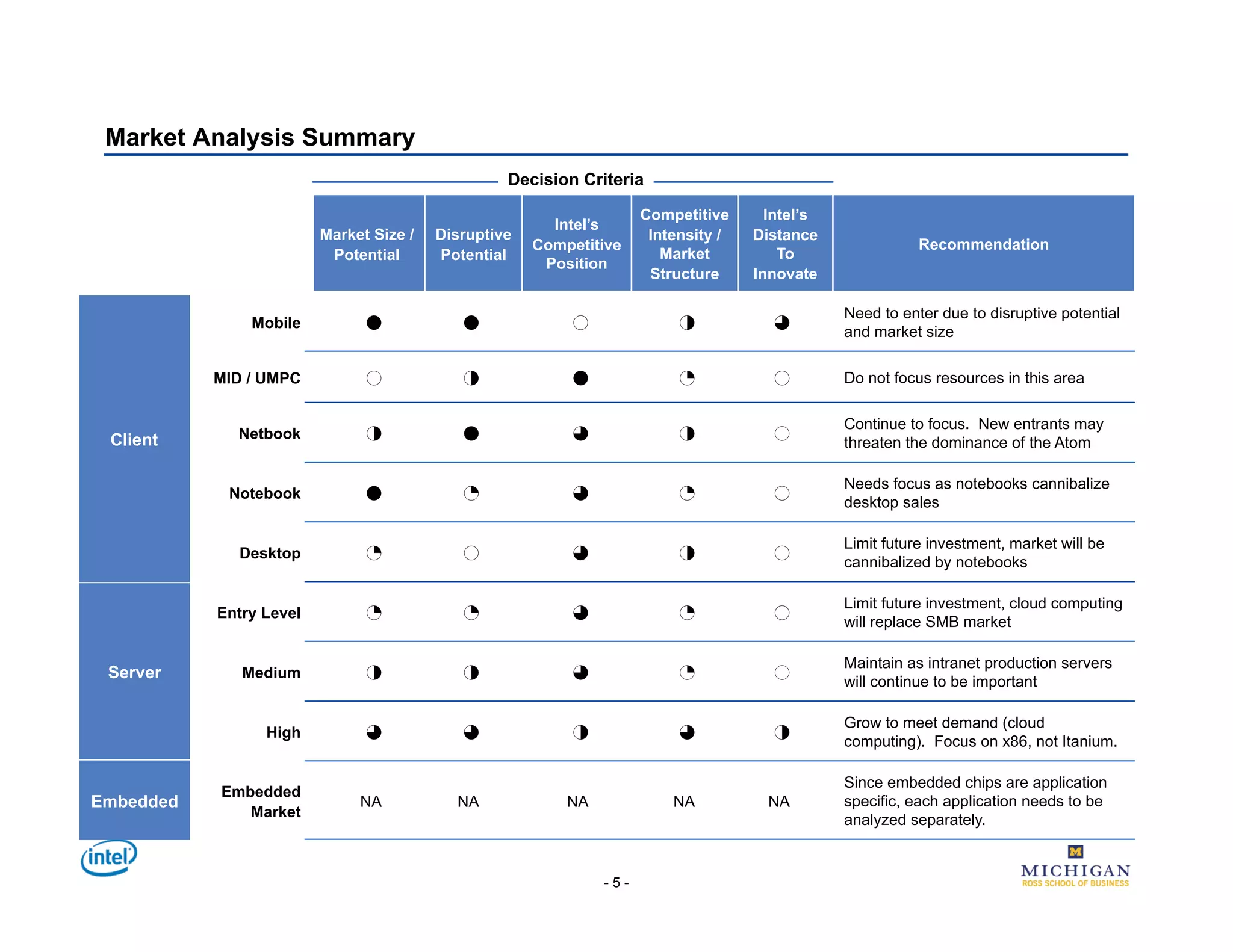

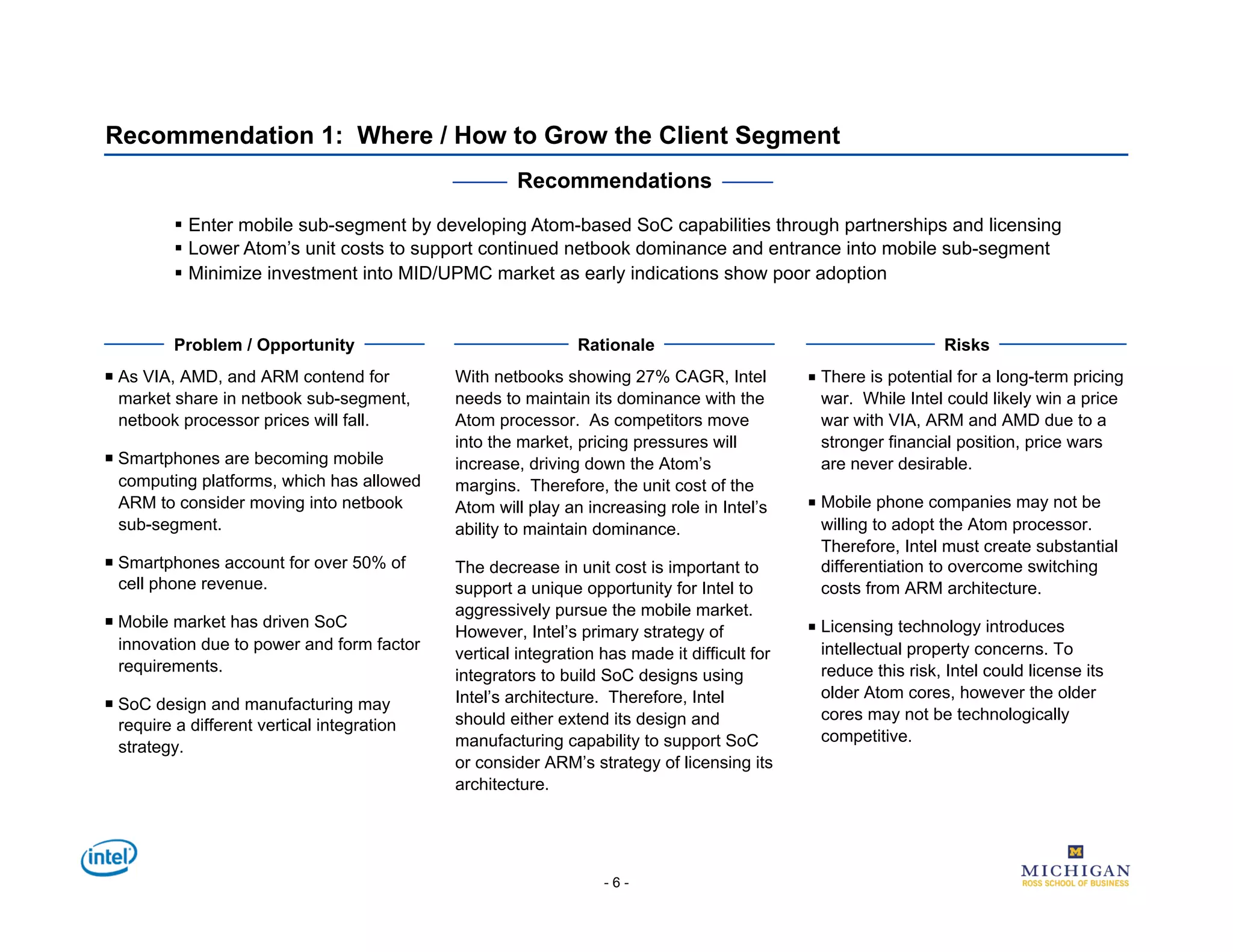

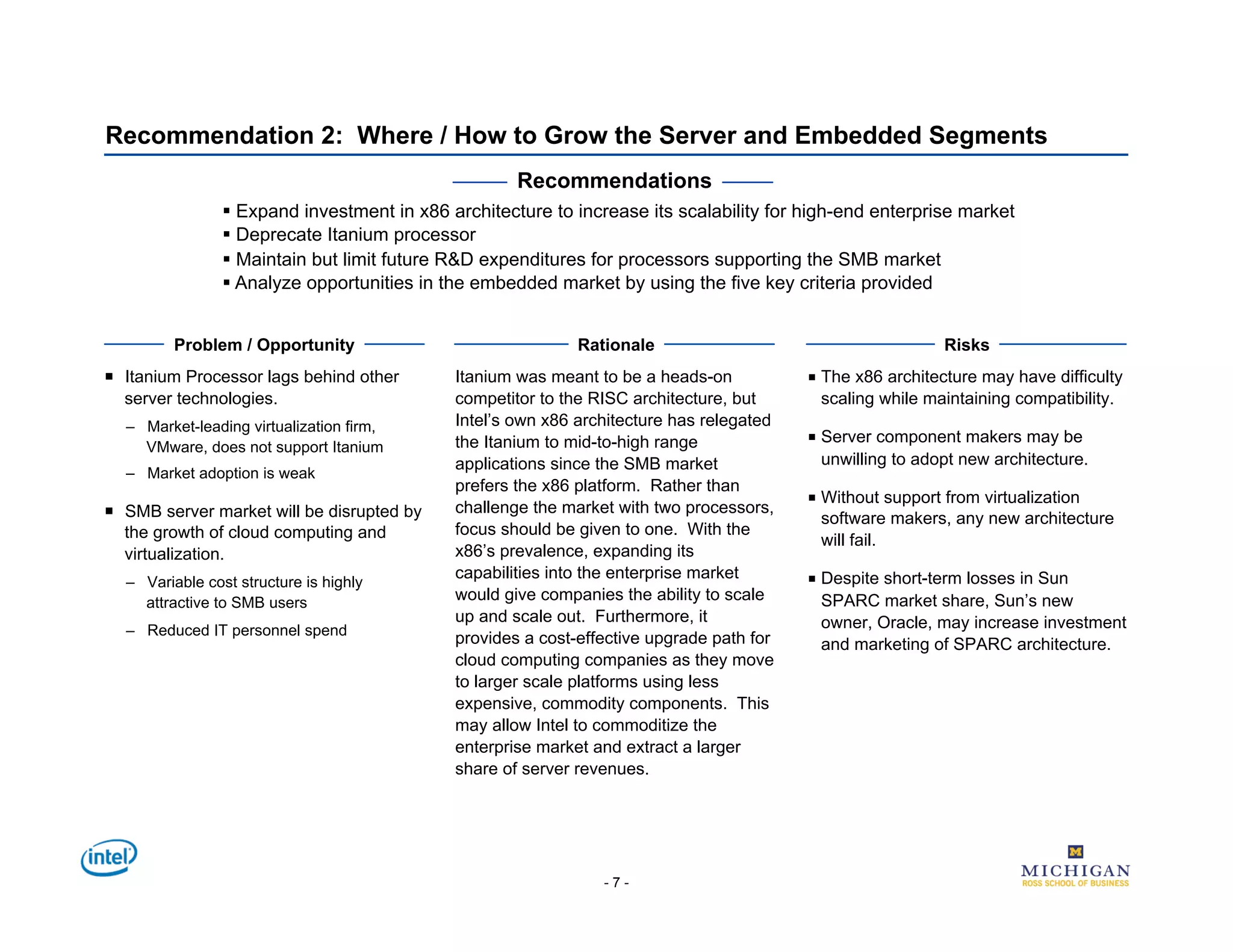

The document outlines Intel's strategy to expand its architecture into adjacent markets, specifically identifying opportunities in mobile, server, and embedded segments. Key recommendations include investing in scalable x86 architecture for cloud computing and mobile devices while minimizing focus on less lucrative markets. The analysis employs five criteria to evaluate potential growth areas and emphasizes the need for partnerships and competitive differentiation in the evolving tech landscape.