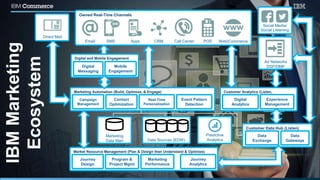

Jak IBM Marketing Platform wspiera koncepcję zorientowania firmy na klienta? Poprzez rozpoznanie i zrozumienie jego potrzeb oraz odpowiadanie na nie, co prowadzi do: - budowania długofalowych relacji, wzmacniania zaufania oraz kreowania adwokatów marki; - Omnichannel poprzez zapewnienie spójnych doświadczeń sprzedażowych i obsługowych w każdym z kanałów kontaktu; - rozwój zdolności biznesowych prowadzących do cross-funkcjonalnego zarządzania wiedzą o kliencie, kontaktami, priorytetyzacją i optymalizacją celów biznesowych; - spektrum możliwych działań podejmowanych w stosunku do klienta od oferty up/cross-sellowej, przez retencję, informację, rekomendację działania do braku działań włącznie. IBM Marketing Platform pozwala na optymalizację marketingu wielokanałowego, pomagając dotrzeć do tysięcy lub milionów osób z właściwym przekazem, we właściwym czasie i właściwym kanale. Rozwiązanie IBM pozwala na uwzględnianie preferencji poszczególnych klientów oraz na szybkie i ekonomiczne projektowanie i realizowanie strategii komunikacji z konsumentami za pośrednictwem wszystkich kanałów elektronicznych i tradycyjnych poprzez: - prowadzenie efektywnego, ciągłego dialogu z obecnym lub potencjalnym klientem z uwzględnieniem całej historii tej relacji, w tym zaprezentowanych ofert, kontekstu i szczegółów kampanii oraz odpowiedzi lub ich braku; - zarządzać kompleksowo logiką kampanii, w tym segmentacją grupy docelowej, wyłączeniami i przypisywaniem ofert i kanałów; - dotrzeć do każdego klienta z właściwym przekazem i we właściwym kanale, a w efekcie podnieść współczynnik konwersji z ofert up/cross-sellowych.