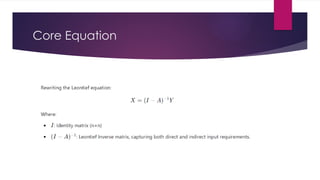

Input-output analysis is a quantitative technique for studying economic interdependencies among sectors, using structured matrices to represent the flow of goods and services. The Leontief production function models these relationships with a linear equation and assumes fixed input-output coefficients, no substitution, and a closed economy. This method provides a static analysis of economic interactions at a specific point in time.