Download as PDF, PPTX

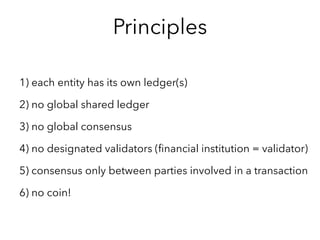

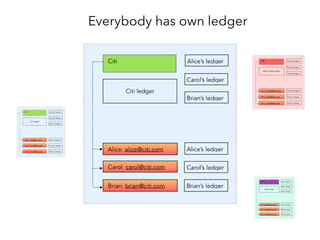

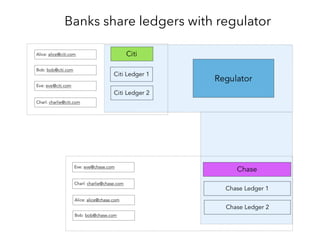

The document describes Infra, an open-source software protocol for financial institutions to facilitate fast and private digital transactions between users and banks in a decentralized manner. Key points include: each entity maintains its own ledger rather than a shared global one; consensus is only required between transacting parties rather than across the whole network; and identities are managed through a federated system of banks rather than a single centralized authority. The goal is to streamline financial processes while maintaining privacy, transparency, and compliance standards of the existing banking system.