The industrial real estate market in the Greater Montreal Area saw improvements in the second quarter of 2015. New industrial construction starts nearly doubled compared to the beginning of the year, signaling continued market recovery. While unemployment rose, full-time employment increased with gains in manufacturing and transportation jobs. Absorption of industrial space rose over 1 million square feet, indicating more space was leased during the quarter. The availability rate increased slightly due to new space added to the market.

Cushman toronto office leasing market report 2014Chris Fyvie

office space toronto, toronto office space, office search toronto, office space in toronto, office rentals toronto, commercial office space, commercial real estate toronto, office rent toronto, toronto offices for lease

Cushman toronto office leasing market report 2014Chris Fyvie

office space toronto, toronto office space, office search toronto, office space in toronto, office rentals toronto, commercial office space, commercial real estate toronto, office rent toronto, toronto offices for lease

office space toronto, toronto office space, office search toronto, office space in toronto, office rentals toronto, commercial office space, commercial real estate toronto, office rent toronto, toronto offices for lease

Lots of great information in our Q2 industrial report. Construction continues to ramp up and some large leases will provide a boost to absorption later this year

There was a slowing of Industrial leasing activity for the summer, but as Amazon proposes to expand their footprint, they have introduced a new type of warehouse to the region.

office space toronto, toronto office space, office search toronto, office space in toronto, office rentals toronto, commercial office space, commercial real estate toronto, office rent toronto, toronto offices for lease

Lots of great information in our Q2 industrial report. Construction continues to ramp up and some large leases will provide a boost to absorption later this year

There was a slowing of Industrial leasing activity for the summer, but as Amazon proposes to expand their footprint, they have introduced a new type of warehouse to the region.

Industrial developers and investors are in touch with the pulse of the industrial marketplace and are taking aggressive steps to meet the potential increase in demand for modern, Class A space.

JLL Detroit Industrial Insight & Statistics - Q2 2016Aaron Moore

The automotive industry is not going anywhere. Although it is in the midst of a disruption, the advancements are a win-win for all. The Big Three are generally experiencing steady growth trends in line with improving consumer sentiment and economic gains.

The report provides key market indicators, trends and forecasting for the #Kitchener, #Waterloo and #Cambridge industrial markets, including vacancy rates, absorption, lease rates, sale prices and recent market transactions. Colliers International #Office #CRE

JLL West Michigan Industrial Insight & Statistics - Q1 2020Harrison West

While West Michigan market has seen historically low vacancy figures and impressive rent growth the past few years, we should expect things to slow in Q2 as the effects of the COVID-19 pandemic begin to take hold. Market fundamentals remain stable; however, given the current uncertainty, we expect leasing and sales activity to slow considerably in the near term as occupiers evaluate their current and future space needs.

Outlook

While not as robust as 2018, the market is expected to

maintain its momentum over the course of 2019. Although

market conditions are increasingly becoming landlord

favourable, the market remains quite competitive. Large

occupiers seeking space in the Central area are now looking

to new developments to satisfy their needs as there are very

few large contiguous blocks of available space left in the

market. In the Financial Core, only six options for tenants

seeking 50,000+ sf of space remain. Despite the

disappearance of large available space options and the

significant downward pressure on vacancy rates, landlords

have only marginally increased rent expectations at

approximately 2% annually. A slight year-over-year increase in

average net asking rates is anticipated as a result of Class

AAA deliveries; however, the range of rates is not expected to

change

Colliers St. Louis 1Q20 Industrial Market SnapshotColliersSTL

Healthy Start but Impact of COVID-19 Remains to be Seen

The St. Louis industrial market started 2020 strong with positive absorption, a healthy construction pipeline and a historically low vacancy rate. However, it is unclear what impact COVID-19 shutdown will have on the industrial sector. Nevertheless, the supply chain, especially for consumer goods, is working hard to keep up with demand. Until the stay-at-home orders have ceased and governments and companies figure out how to best operate in this environment, commercial real estate experts are working with occupiers and building owners to ensure that they can continue to operate when possible and be able to bounce back when able.

The CBD had a strong quarter of activity. Absorption was positive driving vacancy down to 11.9 percent, the third consecutive quarter since 2008 to reach that low.

Similar to Industrial Insight Report - GMA (Q2 2015) (20)

1. Economy

Most noteworthy this quarter were the Greater Montréal Area’s

(GMA) new industrial construction starts which almost doubled from

the beginning of the year and represent the highest increase in

almost two years. This is encouraging for industrial investors and a

long awaited sign of market recovery.

Regardless of an increased unemployment rate of 8.7 percent across

the GMA, full-time employment has made considerable improvements

with some 22,500 new full-time jobs. Notable gains were seen in the

manufacturing sector (gain of 5,400 jobs) and the transportation-

warehousing industry (gain of 15,200 jobs). On the flip side,

employment losses occurred mostly on the administration and

services side.

A strengthening US economy along with a soft Canadian dollar

continued to enhance provincial foreign trade. Provincial exports will

remain a key driver of growth in 2015 with positive implications for

Québec manufacturers. The manufacturing and transportation

industries will continue to further benefit from decreased gasoline

prices.

Quarter in review (Leasing Market)

The leasing fundamentals of GMA’s industrial market has continued

to improve since January 2015. Close to 500,000 square feet of new

industrial space were completed in the second quarter and 2.1 million

square feet are currently under construction; an indication of

continued market recovery and developers’ market optimism.

Overall net absorption rose by over 1 million square feet to end the

quarter at 405,323 square feet; meaning that more industrial space

were leased in the second quarter. The availability rate has increased

by 175 basis points since January to 7.5 percent across the GMA; a

result of new space added to the market which provides more options

to tenants looking for space.

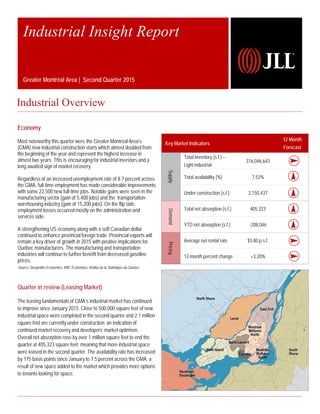

Industrial Insight Report

Greater Montréal Area | Second Quarter 2015

12-month

forecast

Key Market Indicators

12 Month

Forecast

Supply

Total inventory (s.f.) –

Light industrial

316,046,643

Total availability (%) 7.53%

Under construction (s.f.) 2,150,437

Demand

Total net absorption (s.f.) 405,323

YTD net absorption (s.f.) -208,046

Pricing

Average net rental rate $5.80 p.s.f.

12-month percent change +3.20%

Source: Desjardins Economics, RBC Economics, Institut de la Statistique du Québec

Industrial Overview

2. JLL | Greater Montréal Area | Local Industrial Insight Report | Q2 2015

Industrial Overview Cont’d

2

Quarter in review (Leasing Market)

Off-island markets outperformed this quarter. Laval, South-Shore and

North-Shore all recorded strong leasing demand in the second quarter.

A total of 166 buildings were fully or partially leased during the second

quarter. Spaces leased include 11281 Albert-Hudon in the East End

(170,087 square feet), 2100 52nd avenue in Lachine (53,245 square

feet) and 2190 Francis-Hughes in Laval (51,698 square feet). A few of

the largest industrial buildings that became available during the quarter

include 2450 Marie-Curie (166,730 square feet), 867 Hodge (229,355

square feet) and 2500 Marie-Curie (158,958 square feet); all three

properties are located in Saint-Laurent.

Sublet spaces on the market decreased during the quarter. Most

spaces available for sublease were located in Saint-Laurent and range

from 5,000 to 15,000 square feet. There were 107,194 square feet

(across eight buildings) of new sublease space added to the market in

Q2 2015.

There are currently 23,783,236 square feet available for lease in the

GMA of which 54.0 percent are multi-tenant buildings, 43.0 percent are

single-tenant and 3.0 percent are industrial condos. Rental rates rose

slightly across the GMA to an average of $5.80 per square foot net and

$9.10 per square foot gross. Due to their mostly newer inventory,

North-Shore and Laval are currently the most expensive submarkets.

Average asking rents for space above 50,000 square feet did not

increase over the last quarters; there continues to be a large supply of

larger spaces and landlords continue to be competitive to attract and

retain these size tenants. Smaller spaces continue to be abundant on

the market, typically with higher rental rates on a per square foot basis

than larger spaces; thus increasing the average rental rate for the

GMA.

Redevelopment of industrial buildings continued to spread in Q2; more

specifically, refurbishment from industrial to office use. The latest large

buildings to be redeveloped were 1236 Mill street in Sud-Ouest

(264,658 square feet) and 9292 Meilleur in Ahuntsic-Cartierville

(109,740 square feet) both converted into offices. Montréal’s Midtown

submarkets have been the primary target for this type of projects, which

can be very lucrative for landlords.

Approximately 18 percent of industrial buildings which were built prior

to 1960, the majority of which are on the island of Montréal, may not be

suitable for the current demand of higher ceilings and modern office

layouts which is creating a mini-exodus towards markets such as Laval,

South-Shore and North-Shore. Moreover, over 66 percent of Montréal’s

industrial inventory has a clear height below 18 feet and only 11

percent have a clear height of 24 feet or higher. On the Island, higher

ceiling buildings are primarily found in the West-Island and in Saint-

Laurent, leading to the higher asking rates in those submarkets.

Greater Montréal Area Property Clock

Peaking

market

Falling

market

Rising

market

Bottoming

market

Lachine

East End

Landlordleverage

Tenantleverage

Midtown South

Saint-Laurent

Midtown North & South Shore

West Island

Laval &

Vaudreuil

North Shore

Distribution of Availabilities for Lease by Submarket

12.22%

5.01%

17.91%

20.55%8.98%

17.60%

6.91%

2.94%

6.99%

West Island

4,737,361 s.f.

Lachine

2,069,869 s.f.

East End

4,128,747 s.f.

Midtown South

1,154,755 s.f.

St-Laurent

4,057,715 s.f.

Laval

1,592,042 s.f.

North Shore

1,355,527 s.f.

South Shore

1,610,373 s.f.

Midtown North

2,817,139 s.f.

3. JLL | Greater Montréal Area | Local Industrial Insight Report | Q2 2015

Industrial Overview Cont’d

3

Average Lease Rental Rates by Submarket

$7.52 $6.58

$5.69 $6.05 $5.31

$6.20

$5.51 $5.11 $5.04

$3.24

$3.64

$3.79 $3.21

$3.69 $2.63

$3.21

$3.16

$2.69

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

Net Asking Rent Additional Rent

$10.76 $10.22

$9.48 $9.26 $9.00 $8.83 $8.72

$8.27

$7.73

Market statistics

Submarket

Total

inventory

(s.f.)

Number of

buildings

Under

construction

(s.f.)

Total

availability

Quarterly

absorption

(s.f.)

Average net

asking rent

($ p.s.f.)

QoQ %

change in net

rent

YoY %

change in net

rent

Midtown North 50,869,927 1,139 0 5.54% -514,032 $7.52 +0.27% +16.41%

Midtown South 23,981,083 608 0 4.82% 215,862 $6.05 -5.32% +15.90%

East End 69,522,610 2,175 0 5.94% 160,518 $5.04 -0.79% -1.18%

West Island 44,709,317 656 512,000 10.60% -212,633 $5.69 +4.21% +7.77%

Lachine 22,012,450 294 0 9.40% 7,916 $5.11 +0.99% -0.99%

Saint-Laurent 63,139,927 1,019 287,637 6.43% -149,416 $5.31 -2.75% -1.67%

Laval 17,661,943 363 0 9.01% 135,729 $6.58 +2.81% +3.30%

Vaudreuil 810,890 13 294,000 30.03% - $6.75 +3.85% -1.75%

South-Shore 16,522,778 304 893,800 9.75% 371,329 $5.51 -1.08% -9.38%

North Shore 6,815,718 170 163,000 20.31% 401,749 $6.20 +0.55% +1.13%

Greater Montréal Area 316,046,643 6,741 2,150,437 7.53% 405,323 $5.80 +0.35% +3.20%

Source: certain numbers come from Altus Insite

Historical Greater Montréal Area Total Net Absorption and Total Availability

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

-2,500,000

-2,000,000

-1,500,000

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

s.f. GMA Net Absorption GMA Total Availability

New developments/Under construction

There are currently seven industrial buildings under

construction in the GMA for a total of 2,150,437 square feet.

The average delivery time of those new projects are

estimated to be by the end of the year. Montoni recently

announced a new 60,000 square feet development for Abipa

in Boisbriand, the project will be completed at the end of the

summer 2015. Triovest is continuing it’s work on a 150,000

square feet building on FX Tessier in Vaudreuil; the project

will be delivered in December 2015. Broccollini has 144,000

square feet under development on FX Tessier until the end of

2016. Divco will soon be starting a 65,000 square feet

development project at 2985 Douglas B. Floreani. Quintcap

also has 63,000 square feet under development of which half

is already rented out; another project next door should begin

this summer. Broccollini’s building on Aviation street in Dorval

is now fully leased to Cardinal Health and construction will

begin this spring. Almost 70 percent of all current

developments are off the island of Montréal due to the

scarcity of industrial land availability.

Outlook

Landlords will need to continue to reinvent themselves to stay

competitive with the current available market supply.

Moreover, the rise of data center requirements should be able

to breath new life into lower ceiling buildings, as data centers

do not require high ceilings. Finally, we will be slowly moving

from a tenant favorable market to a more balanced market on

the leasing side and should remain in a buyer’s market on the

sale side.

4. JLL | Greater Montréal Area | Local Industrial Insight Report | Q2 2015 4

Industrial Sales Overview

Industrial sales declined in the second quarter of 2015 with 2.4

million square feet sold, a decrease of 13.0 percent from the previous

quarter, across the GMA for a total of $189,692,151. The average

transaction price for non-investment deals was of $61.45 per square

foot.

The most notable transaction of the quarter was the sale of 11281

Albert-Hudon, Sobeys Québec headquarter, a 551,759 square foot

property located in the East End of Montréal. The transaction was a

sale/leaseback and closed at $29.15 million or $52.83 per square

foot.

Throughout the quarter, there were approximately 13.23 million

square feet of industrial space available for sale in the GMA , of

which 9 million square feet were on the island of Montréal. Saint-

Laurent and the East End accounted for almost 38 percent of the

market’s availability with 4.98 million square feet available for sale.

The amount of industrial space available for sale increased across

the GMA and consequently, average asking sale prices dropped

slightly to an average of $68.17 per square foot. Due to their newer

inventory, Vaudreuil and Laval once again had the highest average

asking sale prices. On the other hand, Lachine, Midtown South and

Montérégie recorded the lowest average asking sale prices at

$49.09, $50.35 and $43.81 per square foot, respectively. We

continue to be in a buyer-favorable market across the GMA;

however, smaller stand-alone properties in the 10,000-30,000 square

feet range that are available for sale are becoming harder to find and

thus, sell at a premium. We believe that such properties will continue

to increase in value, representing great opportunities for vendors of

those industrial buildings.

Average Asking Sale Prices by Clear Height (GMA)

<18 feet 19-22 feet 23-27 feet >28 feet

$61.69 p.s.f. $66.54 p.s.f. $71.68 p.s.f. $75.42 p.s.f.

Current Space Available for Sale in the Greater Montréal Area

Submarket Available space (s.f.)

Proportion of the

Market

Midtown North 1,141,355 8.63%

Midtown South 421,046 3.18%

East End 2,408,450 18.21%

West Island 1,879,315 14.21%

Lachine 622,903 4.71%

Saint-Laurent 2,572,077 19.45%

Laval 1,620,251 12.25%

North-Shore 1,511,704 11.43%

South Shore 905,604 6.85%

Vaudreuil-Dorion 143,560 1.09%

Greater Montréal Area 13,226,265 100%

Average Asking Sale Prices by Submarket

Submarket Average Asking Price ($/s.f.)

Vaudreuil-Dorion $87.00

Laval $85.95

Midtown North $79.43

Saint-Laurent $74.91

West-Island $71.68

South Shore $68.50

North Shore $67.91

East End $58.95

Midtown South $50.35

Lachine $49.09

Montérégie $43.81

Sales Transactions (Square feet traded and average $/s.f.)

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

0

1

2

3

4

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015

($/s.f.)

Millionsofsquarefeet

Square feet sold Average transaction value

5. JLL | Greater Montréal Area | Local Industrial Insight Report | Q2 2015

(400) (300) (200) (100) 0 100 200 300 400

Thousands of s.f.

5

Quarterly Market News

Greater Montréal Area

• Real estate developer Gimmelin intends to build a new three

million square feet industrial park for medium and heavy

industries in Eastern Laval at the junction of Highways 25 and

440. The project will have the capacity to accomodate a dozen

large firms with buildings of up to 530,000 square feet. No firm

dates have yet been released.

• Green Cross Biotherapeutics kicked off the construction of its

biopharmaceutical facility located in Saint-Laurent’s Technoparc

campus. The $315 million project is one of the largest

biopharmaceutical projects in Canada and will be built on a land

of 700,000 square feet with a building size of 225,000 square

feet. This project was the result of the Canada-Korea Free Trade

Agreement.

• Lisi Aerospace Canada unveiled plans to install a new production

line to manufacture titaniu assembly parts at its facility located at

2000 Place Transcanadienne in Dorval. The project involves an

investment of more than $12 million.

• Alta Group succesfully rezoned 8.5 million square feet of land to

an industrial use in Coteau-du-Lac adding to the existing supply

of industrial land in the region.

• Womensweat retailer Boutique Jacob is relaunching its

operations with five Quebec stores along with a focus on online

operations to adapt to the current retail environment.

• Ikea Canada announced the opening of a pick-up store in

Québec City. Stefan Sjostrand, managing director, said “The

pick-up format is part of a global Ikea test pilot for secondary

markets where it currently has no stores…”.

Quarterly Leasing Activity by Submarket (s.f.)

Submarket Conditions – Market History and Forecast

Submarket 2012 2013 2014 2015 2016

Midtown North

Midtown South

East End

Saint-Laurent

West island

Lachine

Vaudreuil

Laval

North-Shore

South-Shore

Balanced

conditions

Tenant-favorable

conditions

Landlord/Owner-

favorable conditions

Positive AbsorptionNegative Absorption

North Shore

Greater Montréal Area

South Shore

Midtown South

East End

Laval

Lachine

Saint-Laurent

West-Island

Midtown North

6. JLL | Greater Montréal Area | Local Industrial Insight Report | Q2 2015

Greater Montréal Area • Q2 2015 Highlights

1 4505 HIckmore, Saint-Laurent

Tenant: Mega Brands

Lease renewal: 817,000 s.f.

2 165 Hymus, Pointe-Claire

Tenant: Leviton

Lease renewal: 131,465 s.f.

3 4141 Highway Laval

Tenant: Staples Canada Inc.

Lease renewal: 130,219 s.f.

4 510-560 Orly, Dorval

Rosedale Transport Ltd.

Lease renewal: 83,014 s.f.

5 12225 Industriel, Rivière-des-Prairies

Tenant: Transport Viens

New lease: 48,000 s.f.

6 11281 Albert-Hudon, Montreal North

551,759 s.f.

Buyer: Quintcap & Divco

Seller: Sobeys Québec Inc.

Sale price: $27,100,000 ($52.83 p.s.f.)

7 8000 Henri-Bourassa, Saint-Laurent

297,170 s.f.

Buyer: Groupe Mach

Seller: LaSalle CIG

Sale price: $17,350,000 ($58.38 p.s.f.)

8 2177-2185 23nd avenue, Lachine

200,033 s.f.

Buyer: Cominar

Seller: Igri Industrial Fund

Sale price: $7,215,100 ($36.07 p.s.f.)

9 2125 23rd avenue, Lachine

204,610 s.f.

Buyer: Cominar

Seller: Igri Industrial Fund

Sale price: $7,969,500 ($38.95 p.s.f.)

10 3655 Losch, Saint-Hubert

99,646 s.f.

Buyer: Darmieux Inc.

Seller: Groupe Royal

Sale price: $3,350,000 ($33.62 p.s.f.)

11 3075 Thimens, Saint-Laurent

Direct: 1,642,615 s.f.

Asking rent: No official asking price

12 1144 Magenta, Farnham

(Also available for sale)

Direct: 618,928 s.f.

Asking rent: $4.50 p.s.f net

13 2200 Trans-Canada, Pointe-Claire

Direct: 413,335 s.f.

Asking rent: $5.00 p.s.f. net

14 2105 23rd avenue, Lachine

Direct: 318,960 s.f.

Asking rent: $4.25 p.s.f. net

15 6755 Grandes-Prairies, Montréal

Direct: 283,438 s.f.

Asking rent: $4.25 p.s.f. net

16 800 Industriel, St-Jean

(Also available for lease)

352,000 s.f.

Asking price: $11,500,000

($31.25 p.s.f.)

17 150 Collins, Farnham

272,000 s.f.

Asking price: $4,080,000

($15,00 p.s.f.)

18 117 Hymus, Pointe-Claire

(Also available for lease)

241,929 s.f.

Asking price: $18,500,000

($76.47 p.s.f.)

19 22000 Trans-Canada, Baie-d’Urfé

(Also available for lease)

225,196 s.f.

Asking price: To be determined

20 7800 Trans-Canada, Pointe-Claire

224,130 s.f.

Asking price: $11,500,000

($51.31 p.s.f.)

6

Lease Transactions Sale Transactions Large Blocks Available for Lease Large Blocks Available for Sale

4

2 7

8

138

13

14

17

18

16

10

6

9

13

15

40

40

40

40

13

20

25

15

25

20

117

20

20

15

10

440

25

20

20

10

19

125

134

122

138

520

335

20

15

40

25

138

40

4019

3

6

12

5

1

7

10

15

20

11

7. JLL | Greater Montréal Area | Local Industrial Insight Report | Q2 2015

Helping you

maximize the

value of your

assets