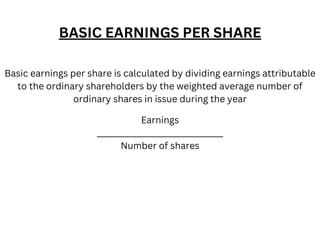

This document discusses Indian Accounting Standard (Ind AS) 33 on earnings per share (EPS). It defines EPS as a ratio used in financial analysis that measures a company's profit allocated to each outstanding share. There are two main types of EPS - basic EPS and diluted EPS. Basic EPS is calculated by dividing earnings attributable to ordinary shareholders by the weighted average number of ordinary shares outstanding. Diluted EPS shows the lowest possible EPS assuming potential ordinary shares are converted to actual shares, and it can never be higher than basic EPS.

![Fmch17[1]](https://cdn.slidesharecdn.com/ss_thumbnails/fmch171-211219052311-thumbnail.jpg?width=640&height=640&fit=bounds)