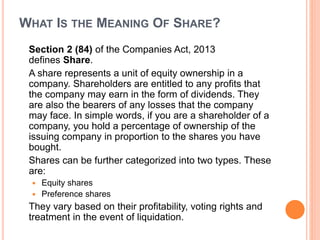

The document discusses various types of shares that can be issued by a company. It begins by defining what a share is, noting that it represents ownership in a company. Shares are categorized as either equity shares or preference shares. Preference shares provide preferential treatment to shareholders in terms of dividends and liquidation. There are various types of preference shares described, such as cumulative, non-cumulative, redeemable, non-redeemable, participating, and convertible shares. Equity shares are also discussed, including how they are classified based on share capital, definition, and returns. The document then covers topics like allotment of shares, irregular allotment, and the effects of irregular allotment.

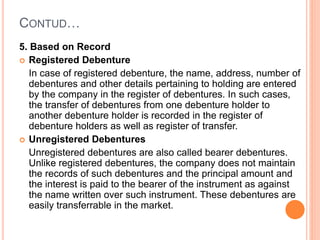

![SPECIAL PROVISIONS RELATING TO APPLICATION

AND ALLOTMENT SHARES & DEBENTURES

The Companies Act, 1956 prescribes certain restrictions regarding the

allotment of shares and debentures by public companies. These

restrictions may be discussed under the following two heads:

I. When no public offer is made; and

II. When public offer is made.

I. When no public offer is made.

Where a public company having a share capital does not offer shares or

debentures to the public, it need not issue a prospectus. In such a case it

shall not proceed to allot shares or debentures unless at least 3 days

before the first allotment it has filed with the Registrar for registration a

statement in lieu of prospectus. The statement shall be signed by every

person who is named therein as a director or proposed director of the

company or by his agent authorized in writing (Sec. 70 (1)]. If the

company acts in contravention of this rule, the allotment shall be irregular

and it will be voidable at the option of the allottee. Further the company,

and every director of the company who willfully authorizes or permits the

contravention, shall be punishable with fine which may extend to

Rs.10.000 [Sec. 70 (4)].](https://image.slidesharecdn.com/unit-iiicl-221105035618-25616614/85/UNIT-III-CL-pptx-18-320.jpg)

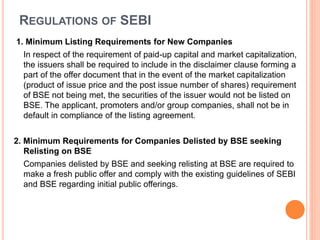

![RIGHTS OF THE MEMBERS

1. Statutory Rights: These are the rights conferred upon the members by

the Companies Act. These rights cannot be taken away by the Articles

of Association or Memorandum of Association. Some of the important

statutory rights are given below

Right to receive notice of meetings, attend, to take part in the

discussion and vote at the meetings.

Right to transfer the shares [in case of public companies].

Right to receive copies of the Annual Accounts of the company.

Right to inspect the documents of the company such as register of

members, annual returns, etc.

Right to participate in appointments of directors and auditors in the

Annual General Meetings.

Rights to apply to the Government for ordering an investigation into the

affairs of the company.

Right to apply to the Court for winding up of the company.

Right to apply to the National Company Law Tribunal for relief in case of

oppression and mismanagement under Secs. 397 and 398.](https://image.slidesharecdn.com/unit-iiicl-221105035618-25616614/85/UNIT-III-CL-pptx-53-320.jpg)