Download to read offline

![1 | P a g e

Report On

CAR FINANCING AND IT’S

WORKING

Submitted to: Sir Vijay Kumar

Group Members:

Fahad-Ur-Rehman Khan (1496) [Group Leader]

MuhammadYasir ()

TalhaShoaib

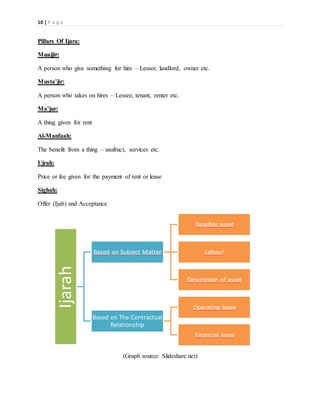

MuhammadImmad](https://image.slidesharecdn.com/carfinancingijara-190101062953/85/Ijarah-Car-Financing-Report-1-320.jpg)

![1 | P a g e

Report On

CAR FINANCING AND IT’S

WORKING

Submitted to: Sir Vijay Kumar

Group Members:

Fahad-Ur-Rehman Khan (1496) [Group Leader]

MuhammadYasir ()

TalhaShoaib

MuhammadImmad](https://image.slidesharecdn.com/carfinancingijara-190101062953/75/Ijarah-Car-Financing-Report-1-2048.jpg)

The document provides a comprehensive overview of car financing, outlining various types of loans such as personal, secured, unsecured, and ijara financing, which is particularly popular in Pakistan. It details eligibility requirements, interest rates, documentation needed, and the mechanics of repayments, emphasizing the importance of credibility and potential economic impacts. In contrast to conventional loans, ijara financing operates on fixed rental payments rather than interest, appealing to many borrowers seeking accessible financing options.

![Ijara Financing In Pakistan [PPT]](https://cdn.slidesharecdn.com/ss_thumbnails/pptibfreportfahadurrehmansgroup-141222054832-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)