Lecture 8 - Technology, Innovation and Great Power Competition - Cyber

IGI Technologies I-Corps@NIH 121014

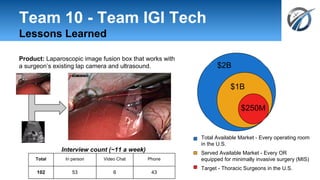

1. Team 10 - Team IGI Tech

Lessons Learned

Product: Laparoscopic image fusion box that works with

a surgeon’s existing lap camera and ultrasound.

Interview count (~11 a week)

Total In person Video Chat Phone

102 53 6 43

$2B

$1B

$250M

Total Available Market - Every operating room

in the U.S.

Served Available Market - Every OR

equipped for minimally invasive surgery (MIS)

Target - Thoracic Surgeons in the U.S.

2. IGI Technologies Team

Principal Investigator

Raj

Shekhar, PhD

Industry Expert

Mark

Chandler, MBA

Entrepreneur

William

Plishker, PhD

● Principal investigator within the

Sheikh Zayed Institute for

Pediatric Surgical Innovation

● Focuses on clinically driven

innovation

● 15 years of experience as a

serial innovator of medical and

surgical imaging technologies

● Two of his prior inventions have

led to commercial products.

● CEO of IGI Technologies

● Builder and leader of

startups, converting

academic research into

real-world products.

● 3 Different Silicon Valley

startups as an engineer

and marketer

● Mayfield Fellow

● Early stage medical

device investor

● Expert in commercializing

intellectual property (IP)

● Founder of Upstream

Partners

● CEO of TAO Lifesciences

5. So here’s what we did:

Experiment: Talk to a wide variety of lap

surgeons outside of home institution

Insight: Very first interview, many lap surgeons

do not have ultrasound, and do not want it.

6. We talked to surgeons - and learned we didn’t

know them as well as we thought

Surgeon Value Propositions Surgeon Pains/Gains

Products/

services

Overlay

ultrasound

on lap field

of view

Guidance

of ablative

tools

Gain creators

Get to target more reliably

than standalone ultrasound

Get to target faster than

standalone ultrasound

Find targets

Pain relievers

Single display

Lower technical difficulty

Reduce risk of complication

Customer Job(s)

Lap surgery --

ablation/resection

Pre-procedure --

diagnose

Post procedure patient

monitoring

Often no task for

ultrasound

Gains

Belief in better patient care

More confidence in complete

treatment

More lap target identification,

less open surgeon

Faster procedures

Pains

Mental correlation across

two screens

Unfamiliarity with

ultrasound

Steep learning curve

Complication risk

7. We refined surgeons into customer

segments… and value propositions

Field High

volume

procedure

core need currently

uses lap

ultrasound

Does NOT

use robot

Urology partial neph See target and vessels (fast, sans

radiologist, mobile)

⇒ do more laps (vs. open)

✔

Gynecology hysterec-tomies

See the ureter

⇒ fewer complications

no, but can

read it

✔

Oncology liver

resections/

ablations

See the target with ablation needle critical

sections

⇒ fewer readmissions

✔ ✔

Thoracic ? lesion location in collapsed lung

⇒ less invasive (more laps, no hand

port)

no ✔

9. So here’s what we did next:

Experiment: Talk to urologic surgeons (and

oncologic, gynecologic, thoracic)

Insight: Good feedback on MVP from

urologists, but thoracic presented as an even

more compelling opportunity.

10. We kept talking to surgeons - and found patterns in

thoracic surgery

Pains

- Disorienting

- Hour-long search

“Would do anything to

localize tumors minimally

invasively”

11. We kept talking to surgeons - and found patterns in

thoracic surgery

Pains

- Disorienting

- Hour-long search

“Would do anything to

localize tumors minimally

invasively”

50-100 cases a year at academic hospitals

⇒ $250M market opportunity

12. Customer segments - what we learned

(# of people overall supporting)

High volume

procedure

core need uses lap

ultrasound

Does NOT

use robot

Urology partial neph See target and vessels

⇒ do more laps (vs. open) ✔

Gyn hysterectomies

endometriosis?

endomet surgery is sensitive to depth

⇒ provide real-time depth (1mm

accuracy) to prevent uterus

punctures (2)

no, and most

(3) can’t

justify port

small but

growing

Oncology focus on

ablations

Losing cases to interv rads (9)

⇒ tool nav in lap ablation is hard, we

would track everything in one place

✔ ✔

Thoracic VATS for

primary lung

lesions

lesion location in collapsed lung

⇒ less invasive (more laps, no hand

port), easier workflow (no fiducials),

organ sparing, find smaller nodules,

⇒ no reliance on interv rad (12)

no, but willing

to learn (10) limited

14. There were many other learnings...

KP

KA

KR

Luminary

Surgeon

(KOL)

Ultrasound

Company

Lap camera

company

Training Curriculum

Enhancement

Lap Ultrasound

Visualization Studies

Integration

Refinement

Software

Devels APIs OR Access

CR - GET

Conference

Presentations

Youtube

Publications

CS

Society Courses

Centers of

Excellence

Surgeon

OR

Mngr

Value

asmt

App form & pres comm

support

Proforma Financials

Admin

council

Tech

assmnt

committee

Conference

Presentations

Youtube

Publications

VAC

Society Courses

Centers of

Excellence

App form & pres

support

Proforma

Financials

Interest

Consideration

Purchase

Awareness

Booth

Installation at

luminary

sites/KOLs

Keep

Support

Unbundle

Track other tools

Use other

camera/

ultrasound

Upsell

Advanced Viz:

Vessel seg

Advanced Viz:

3D recon

Cross Sell

Other surgeons

(thoracic,

urologic,

oncology, gyn)

Referrals

Academic

hospitals

Main-stream

hospitals

US

comps

Co-sales

IGI Tech

surgns

Tracking

company

OR

Mngers

equipme

nt supply

contract

hospital

profit,

etc.

disposab

lmarkers

profit,

etc.

disposable

markers

15. … and we are in a better position than

ever for commercialization

Pivot:

Away from urology to thoracic

Customer Segments:

Primary - Thoracic

Secondary - Urology, Gynecology, Oncology

U.S. Market Opportunity:

$250 Million

102 Interviews:

55 Surgeons

6 Radiologists

10 Surgical support

10 Hospital administrators

5 Ultrasound company officials

3 Robot company officials

2 Tracking company officials

4 Regulatory, reimbursement, IP specialists

7 Misc

Product: Thoracic surgeons find small-cell

carcinoma lung nodules twice as fast without

preoperative preparation.

info@igitechnologies.com

www.igitechnologies.com

19. With respect to submitting an SBIR/STTR Phase II application, we are making the

following decision (PICK ONE)

● Go with a nominal pivot: The feasibility data generated in the Phase I

grant provide the appropriate technical foundation for a Phase II

application, AND we are largely targeting the customer segments that

we had originally anticipated*

● Go with a significant pivot: The feasibility data generated in the Phase I grant

provide the appropriate technical foundation for a Phase II application, BUT

we are targeting very different customer segments than we had originally

anticipated

● No Go: We do not have a product/market fit that supports the continuation of

this project in its current form, and/or we have made substantial pivots to the

business model that require us to obtain additional technical feasibility data

that should more appropriately be pursued under a new Phase I grant (or

other R&D grant)

● No Go: We plan to continue pursuing this project, but we intend to finance this

project through other non-federal sources (e.g., venture, strategic partner, etc)

*we view our thoracic segment as a refinement of our existing plan, and pivot within the

course

Current

Start

IRL = 6 (soft)

(we have mostly validated 4-6)