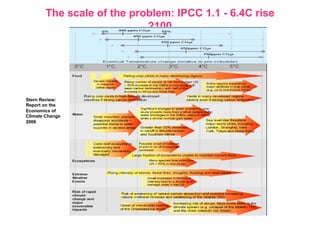

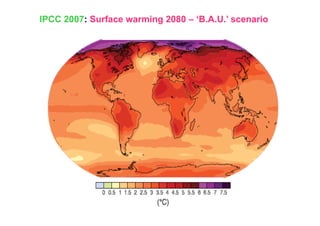

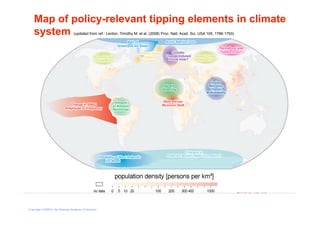

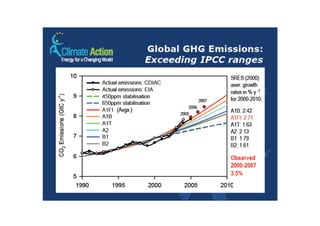

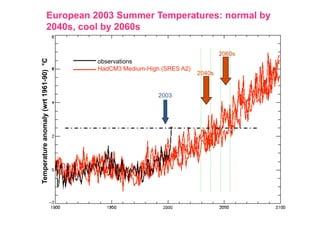

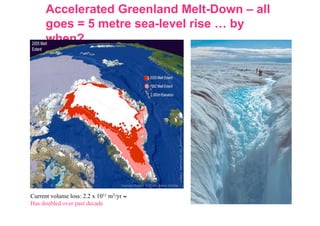

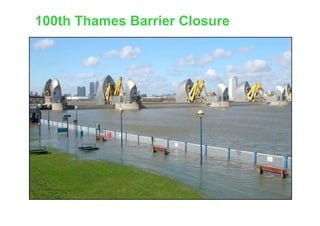

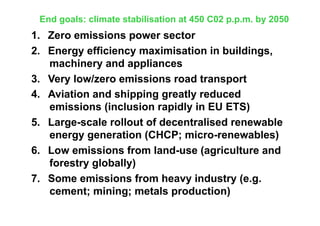

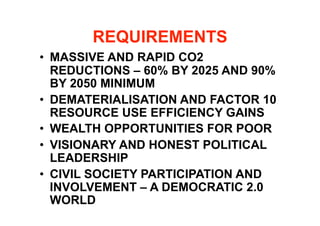

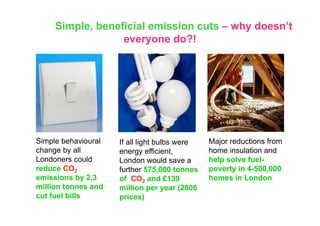

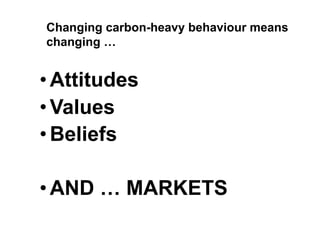

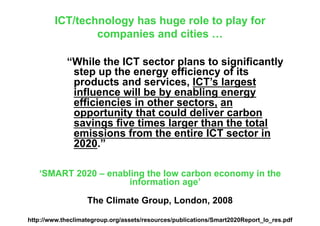

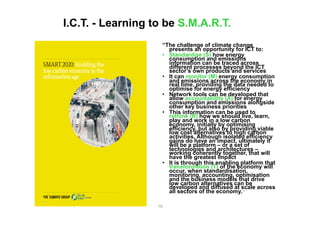

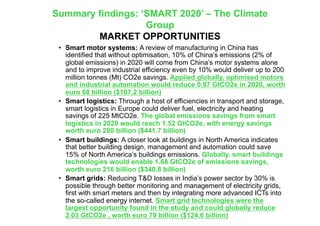

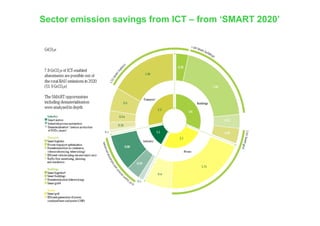

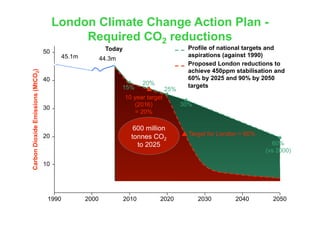

This document discusses the need for urgent action to address climate change through reducing carbon emissions. It highlights the potential for information and communication technologies (ICT) to enable major emissions reductions across different sectors of the economy by optimizing efficiency. ICT can standardize, monitor, and provide accountability for energy consumption data to rethink how society functions in a low-carbon way through smart systems, buildings, transportation, and more. Urgent transformation of society is needed to stabilize the climate through massive CO2 reductions by 2025 and 2050.

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)