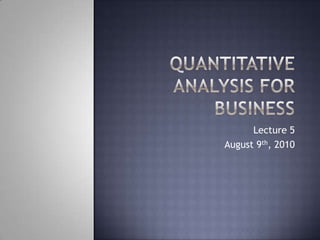

![Multiple Regression Analysis ,[object Object],Y = 0 + 1X1 + 2X2 + … + kXk + where Y = dependent variable (response variable) Xi = ith independent variable (predictor or explanatory variable) 0 = intercept (value of Y when all Xi= 0) I = coefficient of the ith independent variable k = number of independent variables = random error](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Viewers also liked

Similar to Multiple Regression Analysis for Business Lecture

Similar to Multiple Regression Analysis for Business Lecture (20)

More from saark

More from saark (16)

Recently uploaded

Recently uploaded (20)

Multiple Regression Analysis for Business Lecture

- 1. Quantitative Analysis for Business Lecture 5 August 9th, 2010

- 4. Interpreting example 10-year real earnings growth of S&P500 (EG10) Intercept term If dividend payout ratio (PR) is zero and the slope of the yield curve (YC) is zero, we would expect the subsequent 10-year real earnings growth rate to be -11.6% intercept Slope coefficient of PR If they payout ratio increases by 1%, we would expect the subsequent 10-year earnings growth rate to increase by 0.25%, holding YC constant Slope coefficient of YC If the yield curve slope increases by 1%, we would expect the subsequent 10-year earnings growth rate to increase by 0.14%, holding PR constant

- 5. Hypothesis testing of regression coefficients t-statistic – used to test the significance of the individual coefficient in a multiple regression t-statistic has n-k-1 degrees of freedom Estimated regression coefficient – hypothesized value Coefficient standard error of bj

- 6. Ex: testing the statistical significance of a regression coefficient Test the statistical significance of the independent variable PR in the real earnings growth example at the 10% significance level. Data based on 46 observations

- 7. Ex: testing the statistical significance of a regression coefficient We are testing the following hypothesis: The 10% two-tailed critical t-value with 43 degree of freedom (46-2-1) is approximately 1.68 We should reject the hypothesis if the t-statistic is greater than 1.68 or less than -1.68 Greater than 1.68, we can reject the null hypothesis and conclude that PR regression coefficient is statistically significant a the 10% significant level

- 12. The p-value for the F-test and r2 are interpreted the same

- 13. The hypothesis is different because there is more than one independent variable

- 14. The F-test is investigating whether all the coefficients are equal to 0

- 15. p-value – the smallest level of significance for which the null hypothesis can be rejected

- 16. p-value < significance level

- 18. p-value > significance level

- 21. F-statistic F-test assesses how well the set of independent variables, as a group, explains the variation of the dependent variable F-statistic is used to test whether at least one of the independent variables explains a significant portion of the variation of the dependent variable

- 22. F-statistic F-statistic is calculated as Where: SSR = Sum of Square of Regression SSE = Sum of Square of Errors MSR = Mean Regression Sum of Squares MSE = Mean Squared Error Reject H0 if F-statistic > Fc (critical value)

- 23. EX: calculating and interpreting f-statistic An analyst runs a regression of monthly value-stock returns on five independent variables over 60 months. The total sum of squares is 460, and the sum of squared errors is 170. Test the null hypothesis at the 5% significance level that all five of the independent variables are equal to zero The critical F-value for 5 and 54 degrees of freedom at 5% significance level is approximately 2.40

- 24. EX: calculating and interpreting f-statistic The null and alternative hypothesis are Calculations F-statistic > F-critical We reject null hypothesis! At least one independent variable is significantly different than zero

- 26. The p-value for the F-test is 0.002

- 27. r2 = 0.6719 so the model explains about 67% of the variation in selling price (Y)

- 28. But the F-test is for the entire model and we can’t tell if one or both of the independent variables are significant

- 29. By calculating the p-value of each variable, we can assess the significance of the individual variables

- 31. Adjusted R2 Unfortunately, R2 by itself may not be a reliable measure of the multiple regression model R2almost always increases as variables are added to the model We need to take new variables into account Where n = number of observations k = number of independent variables Ra2 = adjusted R2

- 32. Adjusted R2 Whenever there is more than 1 independent variable Ra2 is less than or equal to R2 So adding new variables to the model will increase R2 but may increase or decrease the Ra2 Ra2 maybe less than 0 if R2 is low enough

- 36. A dummy variable is assigned a value of 1 if a particular condition is met and a value of 0 otherwise

- 38. Mint

- 39. GoodTable 4.5

- 42. Model explains about 90% of the variation in selling price F-value indicates significance Low p-values indicate each variable is significant Jenny Wilson Realty Program 4.3

- 44. As more variables are added to the model, the r2-value usually increases

- 45. For this reason, the adjusted r2 value is often used to determine the usefulness of an additional variable

- 48. In some cases, variables contain duplicate information

- 49. When two independent variables are correlated, they are said to be collinear

- 50. When more than two independent variables are correlated, multicollinearity exists

- 53. They have been asked to study the impact of weight on miles per gallon (MPG) Table 4.6

- 54. 45 – 40 – 35 – 30 – 25 – 20 – 15 – 10 – 5 – 0 – MPG | | | | | 1.00 2.00 3.00 4.00 5.00 Weight (1,000 lb.) Colonel Motors Linear model Figure 4.6A

- 57. The easiest way to work with this model is to develop a new variable

- 58. This gives us a model that can be solved with linear regression softwareColonel Motors

- 60. Cautions and Pitfalls t-tests for the intercept (b0) may be ignored as this point is often outside the range of the model A linear relationship may not be the best relationship, even if the F-test returns an acceptable value A nonlinear relationship can exist even if a linear relationship does not Just because a relationship is statistically significant doesn't mean it has any practical value