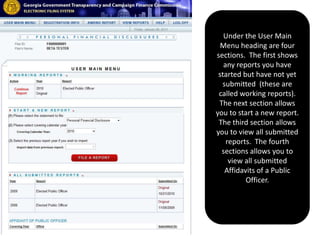

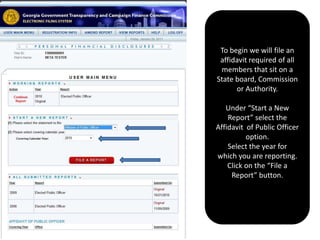

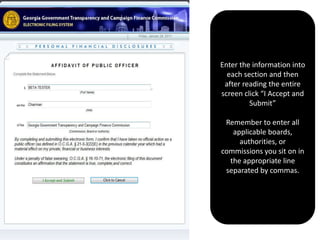

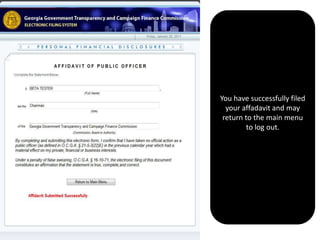

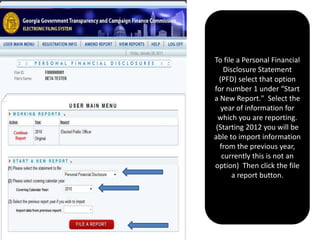

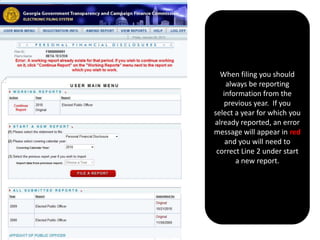

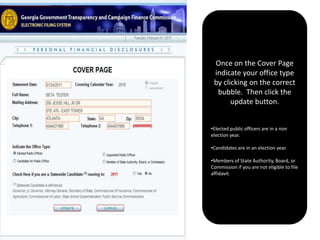

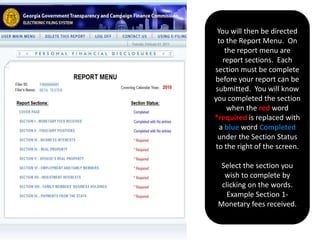

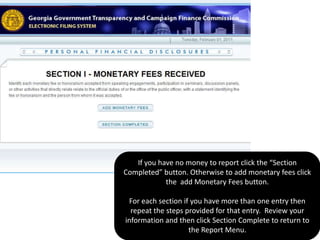

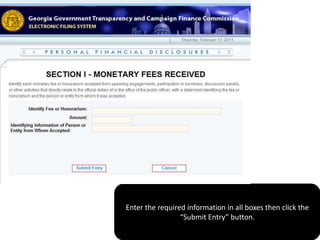

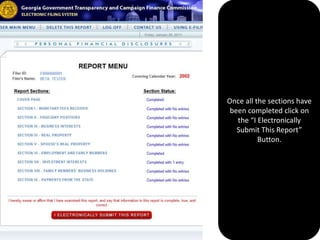

The document provides instructions on how executive directors and members of State Boards, Commissions or Authorities in Georgia are now required to electronically file an annual affidavit rather than a personal financial disclosure statement. It explains how to access the electronic filing system, obtain log-in credentials, and file the required affidavit. The affidavit confirms these individuals took no official action in the previous year that materially affected their private financial or business interests.