Hesa Data 2009 2010 Summary

•

1 like•361 views

The document summarizes data on international students in UK higher education from the 2009-2010 HESA report. It finds that the number of non-UK domiciled students increased 9.5% from the previous year to 454,980. China remains the top sending country, growing 20.2% to 60,660 students. The top 5 sending countries (China, India, US, Nigeria, Malaysia) account for over 50% of non-EU students. All countries in the top ten saw growth in student numbers.

Recommended

More Related Content

Similar to Hesa Data 2009 2010 Summary

Similar to Hesa Data 2009 2010 Summary (20)

More from ESEI International Business School

More from ESEI International Business School (13)

Hesa Data 2009 2010 Summary

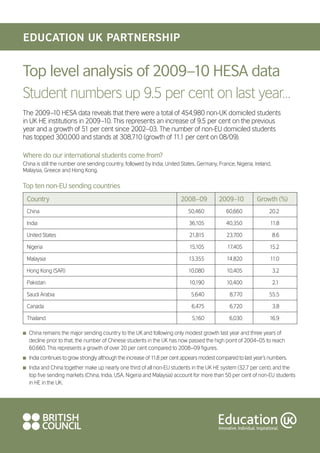

- 1. Top level analysis of 2009–10 HESA data Student numbers up 9.5 per cent on last year… The 2009–10 HESA data reveals that there were a total of 454,980 non-UK domiciled students in UK HE institutions in 2009–10. This represents an increase of 9.5 per cent on the previous year and a growth of 51 per cent since 2002–03. The number of non-EU domiciled students has topped 300,000 and stands at 308,710 (growth of 11.1 per cent on 08/09). Where do our international students come from? China is still the number one sending country, followed by India, United States, Germany, France, Nigeria, Ireland, Malaysia, Greece and Hong Kong. Top ten non-EU sending countries Country 2008–09 2009–10 Growth (%) China 50,460 60,660 20.2 India 36,105 40,350 11.8 United States 21,815 23,700 8.6 Nigeria 15,105 17,405 15.2 Malaysia 13,355 14,820 11.0 Hong Kong (SAR) 10,080 10,405 3.2 Pakistan 10,190 10,400 2.1 Saudi Arabia 5,640 8,770 55.5 Canada 6,475 6,720 3.8 Thailand 5,160 6,030 16.9 n China remains the major sending country to the UK and following only modest growth last year and three years of decline prior to that, the number of Chinese students in the UK has now passed the high point of 2004–05 to reach 60,660. This represents a growth of over 20 per cent compared to 2008–09 figures. n India continues to grow strongly although the increase of 11.8 per cent appears modest compared to last year’s numbers. n India and China together make up nearly one third of all non-EU students in the UK HE system (32.7 per cent), and the top five sending markets (China, India, USA, Nigeria and Malaysia) account for more than 50 per cent of non-EU students in HE in the UK.

- 2. n USA and Hong Kong have turned around the slight declines experienced last year and have grown by 8.7 per cent and 3.3 per cent respectively. n Saudi Arabia continues to grow at an astonishing rate with a growth of 55.6 per cent building on last year’s growth of 45 per cent. The number of students from Saudi Arabia has grown 126 per cent in two years and now stands at 8,775. n Taiwan has dropped out of the top ten non-EU sending countries to the UK, and is replaced by Thailand who experienced nearly 17 per cent growth. All countries in the top ten have experienced growth in the last year. There are now seven non-EU countries with over 10,000 students studying at HE in the UK and 11 countries in total which send over this number. Education UK Partnership countries The table below shows all 18 Education UK Partnership countries. There was a decline in the number of students from three of these countries (Japan, Mexico and Brazil), but a total of ten Partnership countries recorded a double-digit growth, with students from Vietnam and China growing more than 20%. Country 2008–09 2009–10 Growth Absolute growth 2008–09 to 2008–09 to 2009–10 (%) 2009–10 Brazil 1580 1540 -2.4% -40 China 50460 60660 20.2% 10200 Hong Kong (SAR) 10080 10405 3.2% 325 India 36105 40350 11.8% 4245 Indonesia 1120 1240 10.9% 120 Japan 4505 4170 -7.5% -335 Korea (South) 4840 4940 2.0% 100 Malaysia 13355 14820 11.0% 1485 Mexico 1755 1705 -2.7% -50 Nigeria 15105 17405 15.2% 2300 Pakistan 10190 10420 2.1% 210 Russia 3115 3385 8.6% 270 Singapore 3515 4110 16.9% 595 Thailand 5160 6030 16.9% 870 Turkey 3045 3520 15.5% 475 United Arab Emirates 2825 3105 9.9% 285 United States 21815 23700 8.6% 1885 Vietnam 2150 2640 22.8 % 490

- 3. Countries recording significant growth The graph below shows a selection of EU and non-EU sending countries which have recorded a significant growth over the last year (more than 15 per cent growth, and sending more than 1,000 students). In addition to the Partnership countries and Saudi Arabia noted above, an enormous growth has been recorded by the Philippines (66.4 per cent) building on the 61 per cent growth recorded last year. Libya, Kazakhstan and Bangladesh all appeared in this list last year and continue to experience large growth. Nepal with a growth of 61.6 per cent is a new entrant to this list and now has nearly 1,200 students in the UK. Compared to last year, many more countries from the South East Asia region appear to have experienced a large growth. Growth 1870 Phillippines 1125 66.4% 1190 Nepal 735 61.6% 8770 Saudi Arabia 5640 55.5% 3530 Bulgaria 2320 52.2% 3350 Romania 2310 45.0% 3150 Libya 2335 35.0% 2130 Kazakhstan 1585 34.4% 2640 Vietnam 22.8% 2150 60660 20.8% China 50460 1715 20.0% Latvia 1430 3020 19.8% Lithuania 2520 4325 19.3% Bangladesh 3625 4110 16.9% Singapore 3515 6030 16.9% Thailand 5160 17405 Nigeria 15.2% 15105 3520 Turkey 3045 15.5% 0 5000 10000 15000 20000 Number of students in the UK 2008/09 2009/10 Growth in first year student numbers 174,885 non-EU first year students enrolled in UK HE in 2009–10. This is an increase of 12.2 per cent on 2008–09. First year students from Nepal grew 105 per cent, Saudi Arabia saw a 63 per cent increase, Kazakhstan 57 per cent, and Libya 48 per cent. The number of new students from South Korea dropped 1 per cent compared to 2008–09. Pakistan decreased 3 per cent and Kenya dropped 5 per cent despite these markets growing overall. This could be an early indication that these markets are going to shrink.

- 4. What level are they studying at? The majority of non-UK domiciled students study postgraduate taught (PGT) programmes (predominantly one-year Masters courses) and first degree programmes. Roughly one in eight non-UK students study at postgraduate research level, and a similar proportion study at ‘other undergraduate’ level. The size of the population at both postgraduate taught and first degree level are three times as large. 180000 How does this compare to previous years? 171700 160000 All levels of study experienced a growth in the number 170045 of non-UK domiciled students enrolling in 2009 –10. 140000 However, the growth has been largely driven by 120000 students at postgraduate taught level. 109260 100000 The gap between first degree students and 100505 80000 postgraduate taught students is narrowing each year as the popularity of postgraduate taught programmes 60000 56910 50270 grows, and now stands at just 1,655 (compared to 56325 40000 nearly 8,000 two years previously). 40920 20000 0 Postgraduate 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 Research 12.4% Postgraduate Other Postgraduate Research Postgraduate Taught Undergraduate Taught 37.3% 12.6% First Degree Other Undergraduate First Degree 37.7% What subjects are they studying? The most popular subject area for non-EU students in 2009–10 continues to be Business and Administrative studies, and in particular the subjects of Business studies and Management studies. The subject area hosted 93,420 non-EU students in 2009–10 and experienced 15 per cent growth, Accounting and Finance in particular recorded very strong growth (of around 20 per cent). Electronic and electrical engineering remains the most popular subject outside of business disciplines. All subject areas recorded a positive growth apart from ‘Education’ (-1 per cent) and ‘Historical and Philosophical studies’ (-5 per cent). Focussing on new students (first year) by subject area, many subject areas recorded a double-digit growth in this category of student in 2009–10, including ‘Mass communications and documentation’, ‘Mathematical sciences’ and ‘Languages’.

- 5. A wealth of data at your fingertips Members can use our online interactive HESA data-mining tool to produce further statistical reports and charts in a user-friendly format. This allows you to analyse, cross-tabulate and drill-down to investigate where students are coming from and what they are studying. To use the tool, please visit: http://www.britishcouncil.org/eumd/statistics/ Our holistic EMI portfolio also includes the following innovations: Student Decision Making (SDM) A global on-line survey capturing aspirational data from over 124,000 prospective applicants looking to study overseas, thereby empowering a UK institution to tailor their marketing approaches accordingly. Members can access primary data collected by our SDM survey in a real-time, online, interactive, data-mining tool and via tailor-made automated reports. Early reporting of international student data This is an initiative to improve the immediacy of international student data. It allows for an instant insight into enrolment trends of other institutions by country, by subject and by year of course. To find out more about how you can use these tools and more, please visit: http://www.britishcouncil.org/eumd-emi-dataproducts.htm Contact us We hope that you have found this summary useful. If you have any questions or comments, please get in touch. Education UK Partnership British Council Bridgewater House 58 Whitworth Street Manchester M1 6BB United Kingdom T: +44 (0) 161 957 7069 E: education.market.intelligence@britishcouncil.org www.britishcouncil.org/eumd-partnership.htm