Hedge Fund Review EXANTE 2013 Report

•

2 likes•2,864 views

Hedge Fund Review’s special report gives particular emphasis on EXANTE’s potential to support the next generation of financial companies by connecting different types of clients such as asset managers and high-net-worth individuals with its unique integrated electronic trading and fund platform providing access to all markets, all instruments and a variety of exchanges, as well as direct market access and high-speed infrastructure.

Recommended

Recommended

More Related Content

What's hot

What's hot (15)

Similar to Hedge Fund Review EXANTE 2013 Report

Similar to Hedge Fund Review EXANTE 2013 Report (20)

More from EXANTE

More from EXANTE (14)

Recently uploaded

Recently uploaded (20)

Hedge Fund Review EXANTE 2013 Report

- 2. CONTENTS 2 Editor MargieLindsay+44(0)2073169440 margie.lindsay@incisivemedia.com US editor KrisDevasabai+16464903975 kris.devasabai@incisivemedia.com News editor ClareDickinson+44(0)2073169434 clare.dickinson@incisivemedia.com Commercial editorial manager StuartWilles+44(0)20731691982 stuart.willes@incisivemedia.com Publisher AntonyChambers+44(0)2073169784 antony.chambers@incisivemedia.com Sales executive LynseyPorter+44 (0)2073169786 lynsey.porter@incisivemedia.com Advertising fax +44(0)2073169935 Advertising production BenCornish+44(0)2073169477 ben.cornish@incisivemedia.com Marketing executive DhirenPatel +44(0)2073169501 Events marketing manager JenniferNewsum+44(0)2070047469 Subscription and circulation enquiries +44(0)1858438421(UK) +16467361888(US) Fax+44(0)1858434958 incisivehv@subscription.co.uk Subscription renewals ManpreetChanna+44(0)2070047441 manpreet.channa@incisivemedia.com Subscription sales TomDodson+44(0)2070047536 tom.dodson@incisivemedia.com AmyLeather +44(0)2074847423 amy.leather@incisivemedia.com Group publishing director NatKnight+44(0)2073169705 Managing director MatthewCrabbe+44(0)2073169010 Head office 32-34BroadwickStreetLondonW1A2HG Problems? Contactcustomerserviceson+44(0)1858 438421(UK)or+16467361888oremail incisivehv@subscription.co.uk. PeriodicalsPostagePaidatRahwayNJ. Postmastersendaddresscorrectionsto: HedgeFundsReview,C/OMercuryAirfreight InternationalLtd,365BlairRoad,Avenel, NJ07001. Disclaimer:Noinformationinthis magazineshouldbetakenasasolicitation forinvestmentinanyoftheinvestments reportedon. PublishedbyIncisiveFinancialPublishing Limited.©2012IncisiveMediaInvestments Limited.ISSN1471-8855. FUND PROFILES 5 MTG China Arbitrage Fund Capturing the essence of market growth Liza Aizupiete reveals how the MTG China fund is entirely unique despite its trading system boasting an impressive heritage 6 FTM Playing it safe An innovative way to gain value from discounted medical accounts receivables is proving popular with investors 7 Chicago Capital Management Beautifully boring Chicago Capital Management’s strategy will not get any pulses racing, but its returns will 8 Niagara Discovery Fund A winning formula David Rothberg sticks to what he knows and hires managers he knows for the Niagara Discovery Fund 9 The Jordan Company Hedge fund manager makes virtual track record a reality A focus on small and mid-cap companies in undervalued sectors is proving a winning formula for The Jordan Company 10 Apis Offshore Capital A global approach to opportunities Extensive experience, coupled with a flair for finding overlooked investment stories, is a profitable strategy for Apis Offshore Capital 11 Quantum Brains Capital From algos, with love Quantum Brains Capital has used local expertise in mathematics and information technology to create what it believes is a unique set of trading algorithms OVERVIEW 3 EXANTE Access all areas EXANTE managing partner Alexey Kirienko discusses how technology is at the centre of creating systems and product offerings that are attractive for both asset managers and investors EXANTE 2013exante.eu

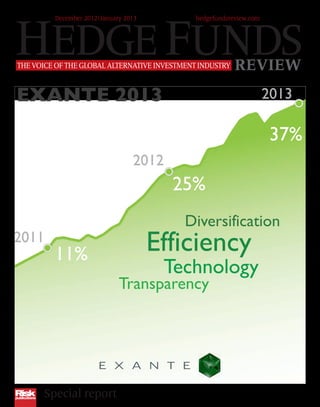

- 3. OVERVIEW Access all areas 3 EXANTE, a Malta-based brokerage company, has harnessed cutting-edge technology to develop an integrated trading and fund platform to support the next generation of financial companies, says managing partner Alexey Kirienko. The company was established in March 2011 to exploit a gap in the market for an execution broker that could provide an electronic platform with access to all markets, all instruments and a variety of exchanges, as well as direct market access and high-speed infrastructure. “All the managing partners of EXANTE used to work with different brokers or hedge funds around the globe,” explains Kirienko, “so the niche was obvious to us and we simply set up the platform to address those needs.” Clients include professional investors, brokerage firms, hedge funds, financial institutions and asset management companies. EXANTE’s automated trading platform (ATP) also offers access to EXANTE Hedge Fund Marketplace, an online platform that currently lists funds from more than 40 management companies. Professional investors and financial institutions can use the platform to view information on a variety of products and then invest with one click. Management companies that list on the platform can gain exposure to users such as high-net-worth investors, financial institutions and funds of funds. The idea for the listings tool came about when brokers at the company found themselves repeatedly connecting different types of clients such as asset managers and high-net-worth individuals. “That wasn’t our core business, so instead of introducing them via phone or in person, we thought it would be much more convenient to set up an online system whereby our customers could click on a particular hedge fund’s name, see details of its performance and maybe read some additional information before being able to simply add it to their portfolio with one click,” states Kirienko. EXANTE’s infrastructure was designed to aid accessibility and to promote transparency. Kirienko argues that EXANTE’s hedge fund marketplace can offer investors more transparency and control than they would normally be able to achieve when investing money with a bank or in the stock market. “An investor can use the platform to create a portfolio of managers that specialise in various fields and even flavour the portfolio with bonds, stocks, and so on, receiving a fair risk/reward,” explains Kirienko. “But, even with a simple deposit in a bank, you do not know what the risks are and are simply paid an interest rate, which is currently very low,” he says. “Stock markets have proven themselves to be highly correlated on a global scale and too reliant on liquidity rather than the intrinsic value of the business.” Hedge funds, on the other hand, are “the ultimate structure for the next generation of finance”, says Kirienko. Investors can check on performance because administrators calculate net asset value (NAV) on a monthly basis and auditors then check the work of administrators. In addition, in the event that an investor does lose faith in one or more of the managers they have invested with, they can simply drop the relevant funds from their portfolio. While the alternative investment market is often perceived to be opaque, Kirienko believes that proper due diligence by an external party can boost investor confidence in the sector. EXANTE itself implements strict criteria for listing funds and has developed an in-depth due-diligence process that involves plenty of direct contact with the fund managers before they are accepted onto the marketplace. “We conduct a lot of interviews and find out where the fund is domiciled, ensure it has appropriate accountants, administrators and auditors,” Kirienko explains. Past performance is also important. For example, EXANTE looks at how long the management company has been in operation and how the fund fared during difficult periods in the market such as the 2008 financial crisis. “If the fund satisfies those parameters, we go in depth with the manager about their strategies. If we think the strategies make sense and there is edge, then we are happy to list the fund on the system.” Kirienko adds that this is crucial to maintaining EXANTE’s reputation as a company that properly researches all of its listed funds. “We look at it like we are going to invest in them,” he says. Technology is at the centre of creating systems and product offerings that are attractive for both asset managers and investors www.hedgefundsreview.com Hedge Funds Review Special report December 2012/January 2013 Alexey Kirienko

- 4. 4 OVERVIEW Future growth The next step for the platform in 2013 will be to augment further its hedge fund listings with the development of the EXANTE Hedge Fund Index,which was launched in February 2012.This is an equally weighted portfolio currently composed of the 22 best-performing managers listed on EXANTE’s ATP. EXANTE aims to increase this pool over time to reach a minimum of 100 management companies. Kirienko believes the index forms a strong basis for an industry benchmark, as well as providing ease of access for EXANTE’s users. The user experience targets a gap identified by EXANTE’s management through its own experience of the market. “We wanted to create a tradeable index that can be accessed with one click,” he says. “That’s very important because I haven’t seen such a system elsewhere.” The key challenge in 2013 for EXANTE will be expanding the index by attracting liquidity and interest in the secondary market, according to Kirienko. As for the Hedge Fund Marketplace, the aim is to increase that to include as many as 200 management companies. EXANTE also plans to expand regionally, opening offices in London and Zurich, as well as turning its attention to emerging markets such as India, South Africa and Brazil, among others. “We have a presence, but we would like to strengthen it,” Kirienko says, adding that EXANTE has a lot to offer emerging markets, particularly those that may not be as technologically advanced as Europe and the US. As well as adding regional managers in these areas, the company believes it can grow by selling white-label versions of its offering. “We think the white-label option is going to be our key focus,” he says.” EXANTE has not offered any white-label packages to date but hopes to sell between five and 10 in 2013, according to Kirienko. “There is a lot of interest in this, especially if the platform comes with all of the instruments we have developed,” he adds. Regulatory outlook One potential break on expansion and development could be the stricter regulations on trading that have been developed in the wake of the 2008 financial crisis. These will affect the hedge fund structure that Kirienko believes will be the definitive model for the next generation of financial company. He is confident about the suitability of EXANTE’s business model to the new regulatory regime.“We think we are operating in the correct way and that the rest of the market should operate like this,” he says. “Managers with assets of $1 million or $10 million should have systems such as ours to showcase their talents. Technology is key to everything.” Over the past year EXANTE has already improved its infrastructure by adding new server units in New York, Chicago, London and Moscow, among other cities with exchanges. As for the regulations that are currently taking shape, Kirienko worries they may be too stringent. “At EXANTE we are all liberals,” he says, arguing that the market structure should be regulated, rather than the market itself. “Any regulations should be like a framework of honesty to allow liberal markets to function. If you start regulating exactly how markets should behave then you will just create more road signs that don’t solve any problems, they just cause more traffic around the junctions.” He argues that a good place for regulators to focus is on service providers to the industry such as administrators and accountants. For example, by requiring that they be paid by those who wish to view the resulting data and reports rather than by the fund being audited. “If the customer pays for an audit, he receives an honest audit,” Kirienko reasons. Current legislation is also too detailed, he adds, pointing to the mosaic of rules that have been in development in the US since 2010 under the Dodd-Frank Act with both the US Commodity Futures Trading Commission and the Securities and Exchange Commission as regulators. “The US is already over-regulated,” he declares, adding that “each line in the [new] regulations creates 100 more interpretations”. EXANTE’s state-of-the-art co-location infrastructure and ATP have been designed to attract investors of all shapes and speeds, from conservative money managers to high- frequency traders. Attempts to limit the latter under the new regulations “will not end well”, according to Kirienko. He believes such initiatives tend to be suggested by those who do not understand and have no experience of the market.“High- frequency traders – our customers – take large orders [such as those placed by pension funds] and take them apart,shifting them to other markets like Asia or Europe and London,and transforming them into different shapes to trade in option markets,physical spot markets,futures markets and so on.” Kirienko calls these larger trades “unwise” and argues that, if pension funds invested more in technology, their systems would recognise the best and most effective way of executing these orders. Overall,just as EXANTE was designed to help players of all shapes and sizes access a range of products and markets,Kirienko believes equal access to markets should be key to any attempt to regulate financial markets.“There should be some light regulation to ensure everyone has equal access,” he says.“Each market member has to have equal rights.” EXANTE 2013exante.eu

- 5. 5 www.hedgefundsreview.com Hedge Funds Review Special report December 2012/January 2013 MTG CHINA ARBITRAGE FUND Capturing the essence of market growth MTG CHINA ARBITRAGE FUND prides itself on having entered a new and exciting market place. It is the second hedge fund created under the MTG Fund SPC umbrella. But what sets this fund apart is, as its name suggests, mainland China. The Chinese markets are notoriously difficult to access for any foreign entity wishing to participate. But, as MTG’s manager Liza Aizupiete explains, the fund has successfully established its presence in China, with staff working at its Shanghai office. The MTG China fund was launched in May 2011. It has netted investors a solid 16.87% (which translates into more than 11% per annum) after tax and expenses since its inception. “Considering various investment restrictions and the relatively small size of the fund, it has done exceptionally well in building up the infrastructure and setting up core operations, thus realising the investment strategy,” says Aizupiete. “The fund draws on extensive experience in arbitrage from the MTG Multi-Arbitrage Fund’s success. We are continuing the investment pattern originally developed by the MTG Multi-Arbitrage team on a new platform that the Chinese markets offer. It is not, however, a pure replica of the trading system, as the new China environment noticeably differs from other developed markets.” Technically, algorithmic trading is less developed in China. Therefore, a completely new algo-trading approach had to be developed to accommodate a number of restrictions and regulations in trading via application programming interface systems. Trading in China is a commonplace activity. The Chinese authorities welcome more institutional participation, in part to stabilise often volatile trading volume swings. The market remains largely closed to outside investors, yet some progressive investment programmes are being set up to gradually liberalise the second largest market in the world. It is only a question of time and political willpower to continue the market reform process, explains Aizupiete, and the MTG China fund is part of this unique opportunity to grow alongside the global China market developments. “We view this as our core selling point: to be able to offer individual and institutional investors participation in the Chinese markets, investing in strategies with low or no correlation to the overall equity or bond markets,” continues Aizupiete. “The fund strives to achieve long-term capital appreciation using a proprietary arbitrage trading system designed and tested to take advantage of market inefficiencies.” The fund’s investment scope includes financial instruments and commodities traded on all major Chinese exchanges. The nexus of its trading, however, is the futures instruments listed on the three largest regulated commodities exchanges in China and the largest commodity exchanges in the UK and the US. Besides this, the fund is also increasing its trading activities in the physical and over-the- counter markets. “Effectively, arbitrage is made possible because of the Chinese market offering – similar products with other well-developed markets that may differ in quality, location and other specifications,” says Aizupiete. “Our fund strategy captures the price discrepancies that occur due to different market participants with diverse sets of needs for hedging or speculating. Our research team is constantly scouting for the best market opportunities, and management enforces the most optimal funds allocation across the trading strategies. The fund’s current broad asset allocation stands at more than 80% in commodities (including physical material), less than 10% in currencies, and the rest is kept in cash.” With the long-awaited advent of new listed derivatives such as options, interest rates and bond futures, the MTG China fund is set to grow exponentially, capturing the very essence of the Chinese market growth. Liza Aizupiete Liza Aizupiete reveals how the MTG China fund is entirely unique despite its trading system boasting an impressive heritage Photo: Normunds Braslins

- 6. 6 Playing it safe FORGET THE MARKET (FTM) fund manager Endre Dobozy believes he can offer investors a safe haven by capitalising on the inefficiencies of the US health insurance market. Dobozy describes himself as “extremely risk averse, the kind of guy that won’t even cross the street unless there are traffic lights”. That attitude inspired him to develop a strategy to generate returns outside of the equity market with minimal risk to investors. The resulting fund, FTM, was launched by Dobozy in 2010 to feed the post-financial crisis appetite for products with an emphasis on capital preservation. He aims to generate returns commensurate with market averages without the rollercoaster ride generally associated with investing in recent years. The main component of the fund is an investment in discounted medical accounts receivables secured at an average rate of $3 for every $1 invested. This investment is routed through a US-based medical accounts receivables company, which covers the medical expenses of insured accident victims involved in personal injury cases. A lien taken against a portion of the payout from the insurance policy is paid once a claim is settled, creating FTM’s returns. “Because the US system is so inefficient, it can take two years or more for insurance payments to come through. So we speed the process up and generate a return that has no correlation to the market,” Dobozy says. In order to minimise risk, the receivables are spread across a number of insurers with no more than 10% of the portfolio attributed to any one company. To further minimise risk, the fund does not blindly purchase a pool of receivables. Rather, each case is carefully reviewed and chosen based on criteria such as who was at fault and whether the injured party is insured. Dobozy adds that FTM is also heavily involved in the research and due diligence conducted by the accounts receivables company when choosing its cases. “We assist with the research of the cases and ensure the accounts receivables company is audited annually. We see the hospitals being paid, the patients being helped and healed, and the money coming back from insurance policies,” he says. The “incredibly strict” criteria used to choose cases means that typically only one out of every five cases reviewed is eventually chosen for funding by the accounts receivables company. Dobozy ensures diversification by keeping between 5% and 10% of the fund in cash and investing the remaining assets – up to a maximum of 5% – in the currency markets via a proprietary trading Endre Dobozy An innovative way to gain value from discounted medical accounts receivables is proving popular with investors system. This strategy typically consists of five open trades in sterling and US dollars. As a result, Dobozy says, the fund can generate returns that are separate to the medical accounts receivables strategy, while also providing liquidity, something accounts receivables cannot deliver. Overall, Dobozy argues that FTM offers investors a safe bet with a 95% capital secured portfolio and an annual return of 12%. “If the market falls 10%, 20% or even 30%, it doesn’t matter to us,” he says. “Even with the foreign exchange component – which is set at a 35% stop/loss – the worst that could happen is a 1.75% loss to the overall portfolio and we make sure that doesn’t happen.” So far, Dobozy’s risk-averse bet has paid off. As of December 1, 2012, the fund is now in its 33rd positive month in a row, with no negative months. With a major shake-up on the horizon for the US healthcare system under the 2010 Patient Protection and Affordable Care Act (also known as ‘Obamacare’), some may question whether returns are sustainable. Until the legislation is fully rolled out, it remains to be seen how it might affect FTM’s future, says Dobozy. FTM EXANTE 2013exante.eu

- 7. 7 www.hedgefundsreview.com Hedge Funds Review Special report December 2012/January 2013 CHICAGO CAPITAL MANAGEMENT Beautifully boring CHICAGO CAPITAL MANAGEMENT (CCM) offers a refreshing antidote to the hallucinogenic complexity of many modern hedge funds. Founded in 1998 by Steven Gerbel, CCM employs a ‘classic’ merger arbitrage strategy, concentrating exclusively in publically announced mergers and acquisitions (MA) in developed markets. CCM does not speculate on rumoured transactions and steers clear of high-octane deals where hostile bids and antitrust concerns may cause spreads to widen. Put another way, the fund is reassuringly boring. “Merger arbitrage is not the most exciting strategy,” Gerbel concedes, “but it does produce very consistent returns.” Merger arbitrage spreads – the difference between the offer price and the target company’s current trading price – have historically tracked at around three times the risk-free rate. This means the arbitrageurs can earn an attractive return by investing in relatively safe deals with a modest amount of leverage. “You need to have a very methodical, repeatable approach. We do the same thing over and over again, making a small profit every time. It adds up to a nice return at the end of the year and compounds handsomely over time,” states Gerbel. “What you shouldn’t do is chase deals with wide spreads, thinking you’ll make money more quickly. That doesn’t work. When you’re wrong on those deals, you lose a tremendous amount of money. The rewards rarely justify the risks.” CCM’s philosophy is to “hedge as much as possible”. Gerbel aims to collect the spreads on offer with the least amount of risk and volatility. The fund typically has exposure to around 35 deals. The risk of individual positions is capped at 5% of the fund’s value. The risk profile of transactions in the portfolio is estimated on a daily basis and the fund’s position sizes, hedges and leverage are adjusted accordingly. Although Gerbel tends to favour “boring deals” with limited downside risk, CCM’s returns are far from mundane. The fund has delivered compound annual returns of 17.32% since its inception in 1998, with a standard deviation of 11.23%. CCM’s returns have held up despite falling deal volume and spread compression since late 2011. While many merger funds have struggled in this environment, CCM returned 6.51% in 2011 and was up 4.38% in 2012 through the end of October. Gerbel ascribes the low deal volume in 2012 to heightened political and economic uncertainties, which made chief executive officers reluctant to take on the risk of an acquisition. “Management teams were understandably cautious. They didn’t Steven Gerbel Chicago Capital Management’s strategy will not get any pulses racing, but its returns will know what the tax rates would be or if they would continue to receive government subsidies. It’s impossible to make an intelligent decision about a deal in that situation,” he says. However, Gerbel is convinced deal activity will pick up in 2013. “The outlook is very good for MA,” he says. “There is $2 trillion of cash on the balance sheets of corporate America. Asset prices are at historical lows. Companies can borrow at the lowest rates in a generation. A lot of deals will be cut once the fiscal cliff is behind us and the questions over tax rates and government spending are resolved.” Gerbel expects to see plenty of deals in the financial, pharmaceutical and technology sectors. He predicts a large number of smaller US regional and community banks will be forced to merge in 2013 as a result of Dodd-Frank and the Basel III capital rules, while pharma and tech companies need to make acquisitions to fill product gaps after cutting back on research and development in the recession. While the MA market may heat up in 2013, Gerbel has no intention of ramping up the fund’s risk taking. “We’re going to do what we’ve always done,” he says, “which means doing the little things right, staying disciplined and avoiding style drift. It’s classic, boring, blocking and tackling, but it works.”

- 8. 8 NIAGARA DISCOVERY FUND A winning formula THE NIAGARA DISCOVERY FUND provides exposure to five distinct macro-oriented investment styles in a fund of managed accounts structure. The fund is the brainchild of Albert Friedberg and David Rothberg. Friedberg is the founder and chief investment officer of Friedberg Mercantile Group (FMG), one of Canada’s best-known futures trading houses. FMG manages close to $1 billion in the Friedberg Global Macro Hedge Fund, which has achieved compound annual returns of more than 17.5% since its inception in December 2001. Rothberg, the fund’s strategy adviser, has been affiliated with FMG since 1976 and sits on the macro fund’s risk committee. Friedberg’s investment approach, which he has employed successfully for nearly four decades, is built around five main trading concepts: momentum, sentiment, fundamental and technical analysis of commodities, discretionary macro and value investing. While Friedberg’s macro fund utilises these approaches in a single portfolio, the Discovery Fund assigns each strategy to an external manager. The fund managers were hand-picked by Friedberg and Rothberg, and most of them have strong connections to FMG. “The idea behind the fund was to do what we know with people we know,” says Rothberg. “We hire managers we have known for years to run strategies that, in aggregate, deliver uncorrelated returns with no beta.” The momentum strategy captures long-term price trends in futures markets. The systematic programme relies on an algorithm to identify trends that are likely to persist beyond rational levels. Volatility filters are used to size positions and identify exit points. The sentiment strategy serves as a counterpoint to momentum. In this case, the manager – an FMG alum – focuses on scenarios where consensus runs contrary to current price trends. Trading opportunities are identified by analysing divergences and convergences in the relationship between open interest and price. Rothberg characterises the momentum and sentiment managers as “professional games players” who, like all commodity trading advisers (CTAs), compete with other speculators to profit from inefficiencies in the futures markets. In contrast, the Discovery Fund’s discretionary macro manager uses futures to express a top-down view of global economic trends. This manager’s trades are based on the interplay between price, time lags, supply and demand fundamentals as well as economic imbalances. The commodity portfolio is managed by a team of four traders David Rothberg David Rothberg sticks to what he knows and hires managers he knows for the Niagara Discovery Fund within FMG. The group performs fundamental analysis of supply and demand for commodities and combines this with technical analysis to confirm their views and establish entry points and stops for trades. The fifth and final leg of the fund is a value equity strategy. This manager invests in US mid-cap stocks that are priced at a discount to value and have plenty of free cash flow. Rothberg hedges out the beta of the long portfolio with futures contracts. Rothberg assigns the risk budgets and leverage limits for the five strategies. In making allocations to the strategies, he considers their relative volatilities, risk/reward profiles and correlations. Asset allocation is dynamic, although the weightings rarely shift dramatically as the strategies tend to be uncorrelated in most market environments. The trades of underlying managers are continuously monitored and any excess aggregate risks are hedged out at the portfolio level. Stress tests are also performed to ensure the fund’s losses are contained in a market crisis. The result is a portfolio that provides exposure to a diverse mix of uncorrelated macro-investment strategies with none of the additional costs of a traditional fund of hedge funds. EXANTE 2013exante.eu

- 9. THE JORDAN COMPANY 9 Hedge fund manager makes virtual track record a reality A BACKGROUND in corporate mergers and acquisitions (MA) has allowed Vad Yazvinski, chief investment officer of The Jordan Company and portfolio manager for Jordan Capital Asset Management, to hone a strategy of targeting undervalued small and mid-cap companies that are ripe for acquisition. Intent on learning the MA business after graduating from Western Carolina University, Yazvinski went to work for the corporate strategy group of SP 500 company Total System Services. “My long-term goal was always to start a fund. I wanted to learn how the MA process works from the inside and then go out there and put together an investment vehicle,” says Yazvinski. In June 2008 he did just that, launching Atlanta, Georgia-based Jordan Capital Asset Management. Yazvinski’s previous investment experience consisted of six years spent developing a virtual track record, during which time he entered and won portfolio simulation competitions such as MSN Money’s 2006 Strategy Lab Open. When it came to setting up the fund, The Jordan Company accepted this virtual track record as proof of his ability and of the strength of his investment rationale. “There are very few people that can successfully transfer an investment strategy from the virtual to the real world due to the very emotional aspect of playing with funny money versus real money,” he says. It is a long/short fund with below-average volatility invested in publicly traded securities. The fund is typically 55% net long and unleveraged. Yazvinski aims for a return that is slightly better than the market with a third of the risk. While the $2 million held at launch in 2008 has since grown to $31 million, Yazvinski’s aim is to build a track record rather than aggressively market the fund. “For me investing is not just my work, it’s something I want to do for the rest of my life. So I want to focus on slowly and steadily executing the strategy I’ve developed over the last decade, I’m not really worried about the pace of assets under management growth.” His strategy involves identifying small and mid-cap companies in undervalued sectors that are ripe for change in the next 18 to 24 months. “I fully subscribe to the Warren Buffet-style value methodology of looking for businesses that are trading at a discount to intrinsic value,” he says. “However, the big difference between myself and typical value managers is that identifying a catalyst that will provide value realisation is also an important part of my strategy. I look for Vad Yazvinski A focus on small and mid-cap companies in undervalued sectors is proving a winning formula for The Jordan Company indications that a company is likely to be looking for strategic alternatives, such as a tender offer, a restructuring or a dividend payment.” For example, the fund is currently invested in the US regional banking sector, where Yazvinski believes the larger regionals – the US top 30 banks – currently have no avenue for growth other than taking over smaller players. “They are looking for names that either represent a new geography or an attractive entry point from a financial standpoint, which means names that are selling for below tangible asset value in many cases,” he explains. “The fund has positions in some small regional banks that we believe are great acquisition targets.” Regional banks in states such as Texas and Wisconsin are particularly attractive because many large banks have a smaller footprint in these states, according to Yazvinski. This sector also provides the fund with exposure to what he believes is the most undervalued asset class in the world – US real estate. “This is currently one of our largest areas of exposure, but we invest mostly on the preferred side because the common equity of US homebuilders and real estate is overpriced,” he says. “Also we effectively have an indirect bet on this sector by way of regional banks since the majority of their loans are related to real estate.” www.hedgefundsreview.com Hedge Funds Review Special report December 2012/January 2013

- 10. 10 EXANTE 2013exante.eu APIS OFFSHORE CAPITAL A global approach to opportunities NEW YORK-BASED boutique hedge fund Apis Offshore Capital aims to identify undervalued and underreported investment stories as they play out across the globe. According to Apis Offshore Capital fund manager Dan Barker, his team’s level of experience sets the fund apart from its competitors. Along with his current colleagues, Barker left investment management company JW Seligman to launch Apis Offshore Capital in 2004. “As a team, we have worked together for 10 years and that’s what gives me the most confidence about Apis and our performance going forward. We have had that continuity. We’ve grown together,” says Barker. The fund is mainly focused on small to mid-cap companies, although it does invest in larger companies under the right circumstances. “It’s really about whether we can add value to the research process,” Barker says. “Inefficiencies are often greater in small to mid-cap securities, so we naturally gravitate there, but it doesn’t mean we won’t look at a large-cap situation if we think we can bring edge to that idea.” Geographical concerns are viewed with a similarly open attitude. Barker believes the fund’s borderless approach to investing allows for maximum leverage of each idea. The team’s combined experience in global equities gives the fund a head start on emerging trends as they spread to new regions or sectors. For example, Apis Offshore Capital recently added a long position in Japan-focused alternative energy player West Holdings to its portfolio. The company has access to the lucrative government subsidies currently being offered in Japan to stimulate energy production after its nuclear sector was shut down following the devastating earthquake in March 2011. “This is typical of what we can do at Apis in that we’ve watched similar subsidy programmes roll out in Germany, Italy and Spain,” Barker says. “It creates a bonanza of activity in the sector. But what is interesting about Japan’s programme is that the subsidies [in the region] are more than double the best offered in Europe. We think we are early to this play in Japan because of the experience we have in Europe.” Apis also looks for ways to short the market via long-term cyclical themes.Recently,the fund has been short the global tanker market via stocks such as energy transportation company Overseas Shipholding Group.The thinking behind this strategy,Barker explains,is a global oversupply of very large crude carriers,long-haul tankers that can transport two million barrels or more of crude oil. Dan Barker Extensive experience, coupled with a flair for finding overlooked investment stories, is a profitable strategy for Apis Offshore Capital “When these ships are ordered, delivery can be made as much as three years later. At the moment, a lot of new ships are about to hit the water and it will take many years for them to be absorbed,” Barker explains. Demand for the ships has fallen as the US has become less dependent on foreign oil, he adds, a trend that has been driven by the weak economic picture as well as increasing US domestic energy production. While Barker predicts that tanker demand will eventually recover, he says the current state of affairs in the market is likely to last for some time. The weak economic outlook has also affected the long side of the fund. “We remain cautious about global growth and currently favour areas in which the economic backdrop is not as important, although it tends to play some part in every company’s equation,” Barker says. “We are invested in areas with a growth dynamic that is insulated from what we feel might be a disappointing economic environment next year.” At the beginning of December 2012, the fund was up 11% for the year. “This is somewhat in line with the benchmark MSCI index but, with about two-thirds of the market’s volatility,” Barker says. Since inception, the fund has returned 118% versus 53% from the MSCI.

- 11. QUANTUM BRAINS CAPITAL 11 From algos,with love BEING ABLE to tap the knowledge of professionals in a range of fields including mathematics, quantum physics and computer theory is handy when trying to formulate an algorithm that can make money in today’s complex markets. That is what Russia-based Quantum Brains Capital (QBC) believes sets it apart. With the combined brain power of teams of mathematicians, physicists and IT specialists to hand, it has spent eight years and more than $10 million developing trading algorithms before putting them to work in the Bermuda-domiciled Quantum Brains Capital Fund, launched in 2012. The management company was co-founded by Arsen Yakovlev and Gregory Fishman. Yakovlev has a background in developing mathematical methods for trading and algorithmic models. He started his investment career in 2004 as a portfolio manager of a Russian private investment fund. Fishman’s experience spans both IT and finance, having worked in the financial technology and communications businesses. He is founder and president of Automated Intelligence Systems, a Russian scientific institute established in 2006 to carry out research and development on artificial intelligence systems. From its base in Russia, QBC has access to some of the top mathematics and IT graduates in the world. The University of St Petersburg is known for its IT training and Russia has long had a focus on maths education. In addition, QBC sources science expertise from the UK and Russia. Quantum Brains Capital Fund combines several different trading strategies: trend following, mean reversion, arbitrage, fixed income, high-frequency trading and heuristics, which in its most basic form means finding solutions through trial and error. Long-term arbitrage trades provide a contrast to the high-frequency trading strategies. The fund trades a range of instruments and markets with a focus on Russian equities, which have maintained a positive performance through 2012. Russia’s blue chip RTS Index was up 5.07% in 2012 to mid-December. Close attention is paid to the correlation between assets. QBC believes that by maintaining a diverse portfolio, systematic risk is reduced. Arsen Yakovlev Quantum Brains Capital has used local expertise in mathematics and information technology to create what it believes is a unique set of trading algorithms Daily turnover for the fund is around $1 billion, which is about 10% of the daily turnover of the Russian market, according to QBC. During the development of the fund, combinations of algorithms were created and then tested using an approach based on Monte Carlo methods. The best-performing trading programs were selected for the fund, which creates an optimal portfolio maximising risk/return ratios, according to QBC. The testing also determined the weight of each strategy in the portfolio and how the strategies interact with one another. QBC continues to tweak its systems, to make them better and more powerful, with the hope that they will become faster and more effective. Risk management is impossible if you cannot predict future events, believes QBC. With that in mind it has built a model based on hidden semi-Markov processes to predict changes in the market environment. The process, named for the Russian mathematician Andrey Markov, is a stochastic process satisfying a certain property, called the Markov property. As with many hedge fund strategies, market volatility is used to generate returns. For this reason, intervention in markets by governments and central bankers has impacted performance in 2012. Announcements from the European Central Bank, for example, tend to send markets into frenzy, pushing volatility higher. During such months, the fund generated positive returns. Overall, it has retained positive performance for the year, according to QBC. The fund is on the Emerging Manager Platform, a Bermuda- based platform for start-up managers established by managing directors of Apex Fund Services Peter Hughes and John Bohan. Apex provides administration services for funds on the platform. Legal and accounting support for new managers is also given. Currently only internal money and some private asset managers are invested in the fund, but QBC intends to open the fund to external investors. QBC has big ambitions for asset growth for the fund as well as its performance in 2013, believing it can achieve returns of at least 40%. www.hedgefundsreview.com Hedge Funds Review Special report December 2012/January 2013