Download to read offline

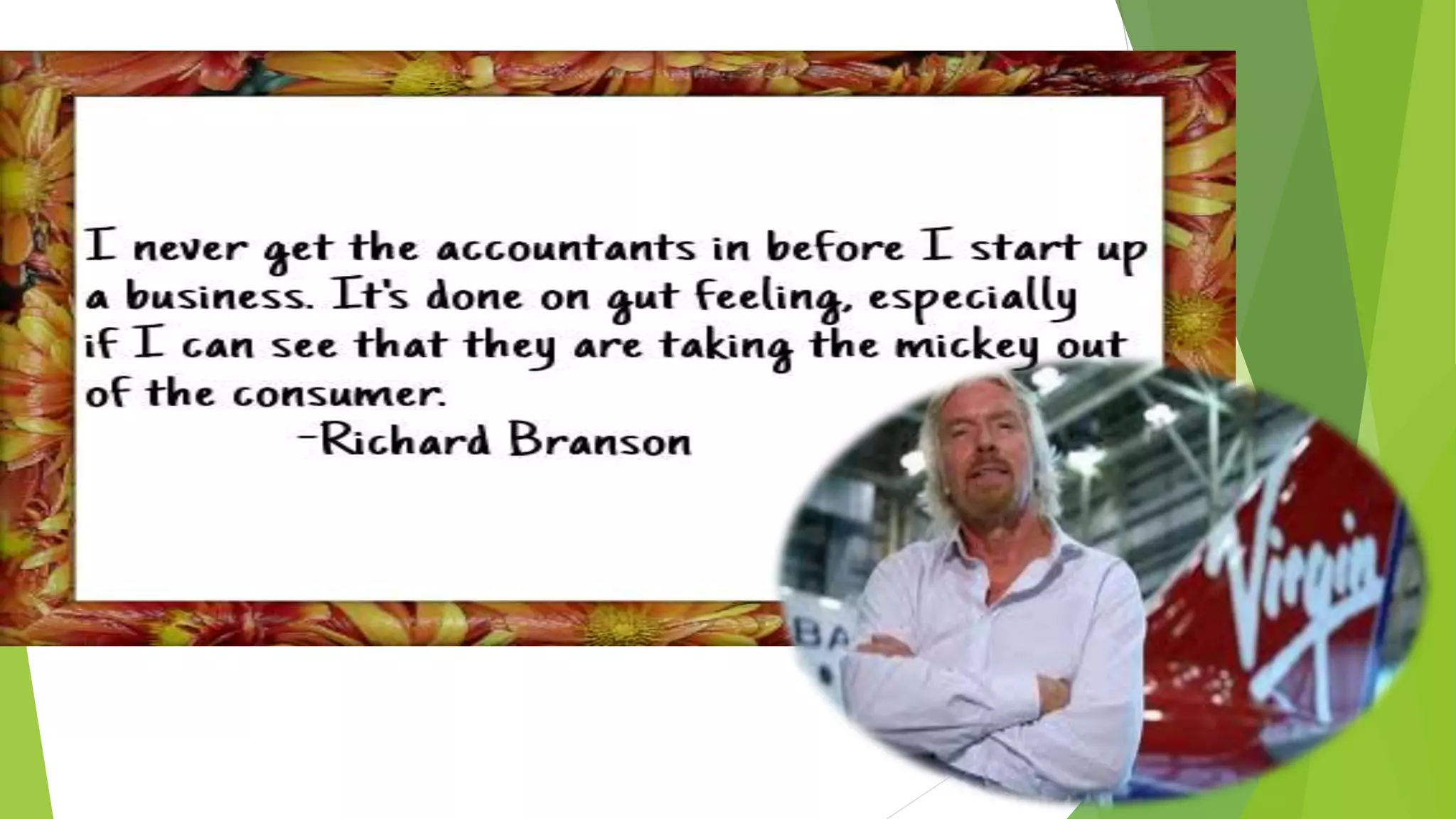

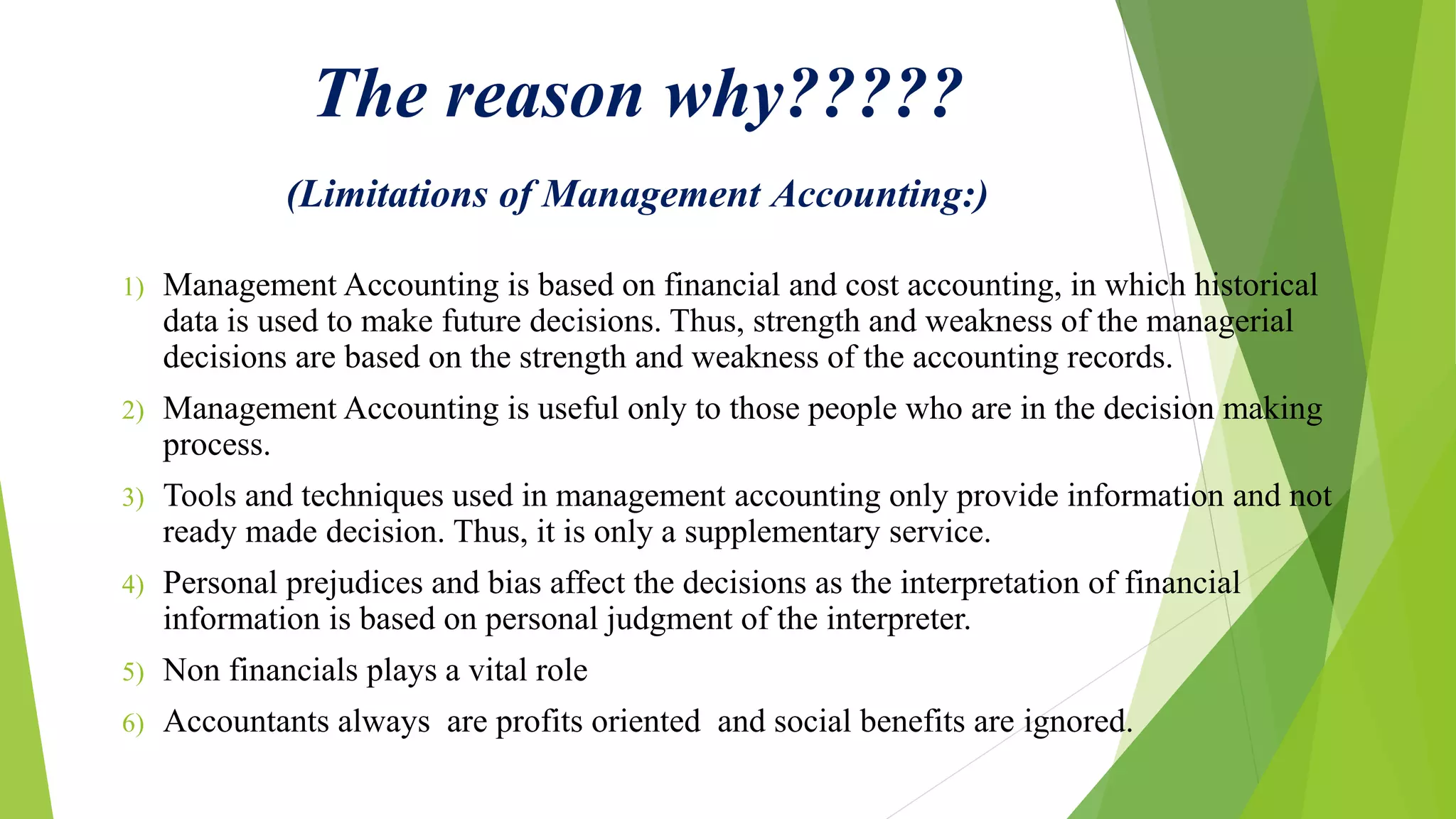

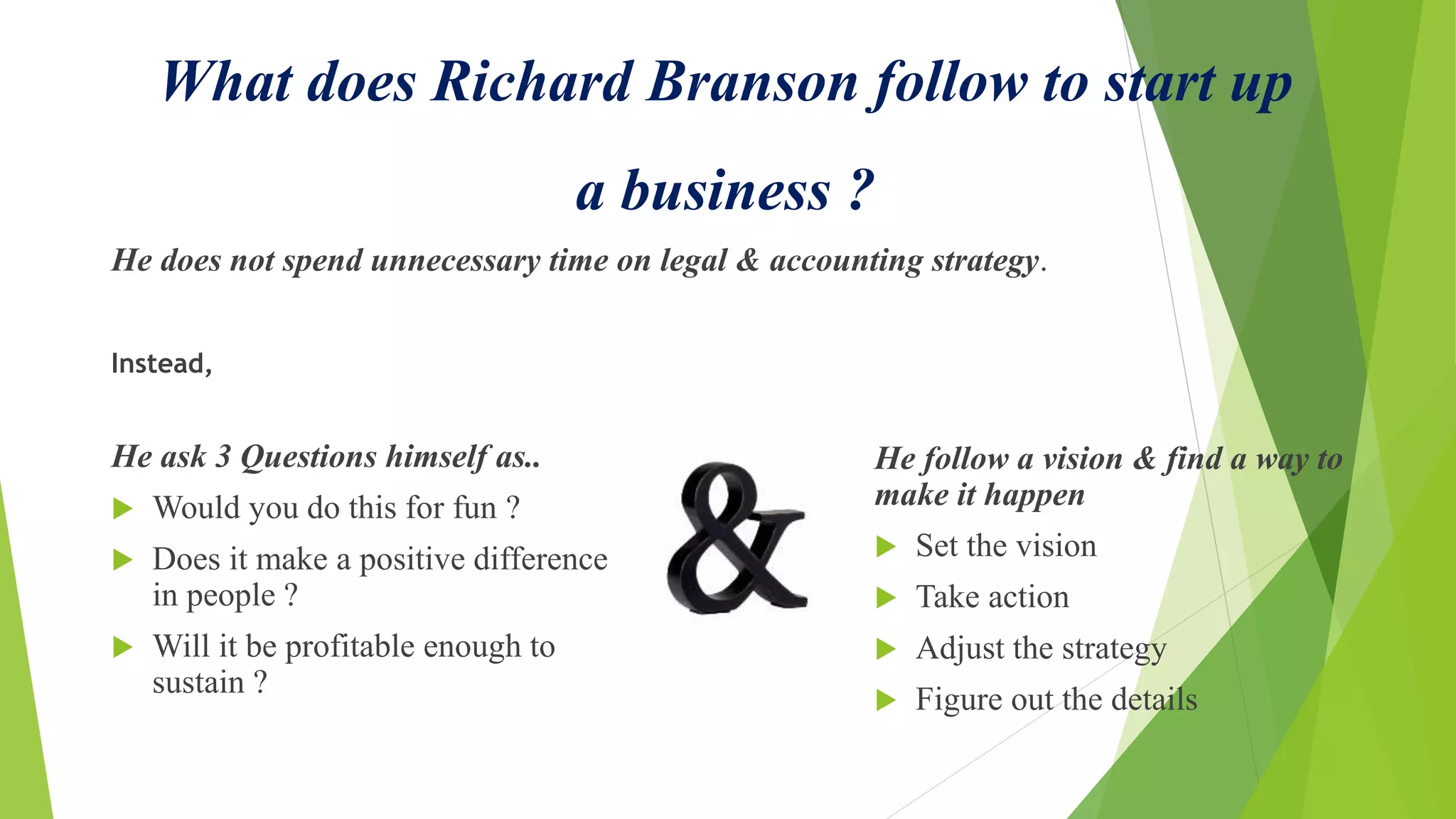

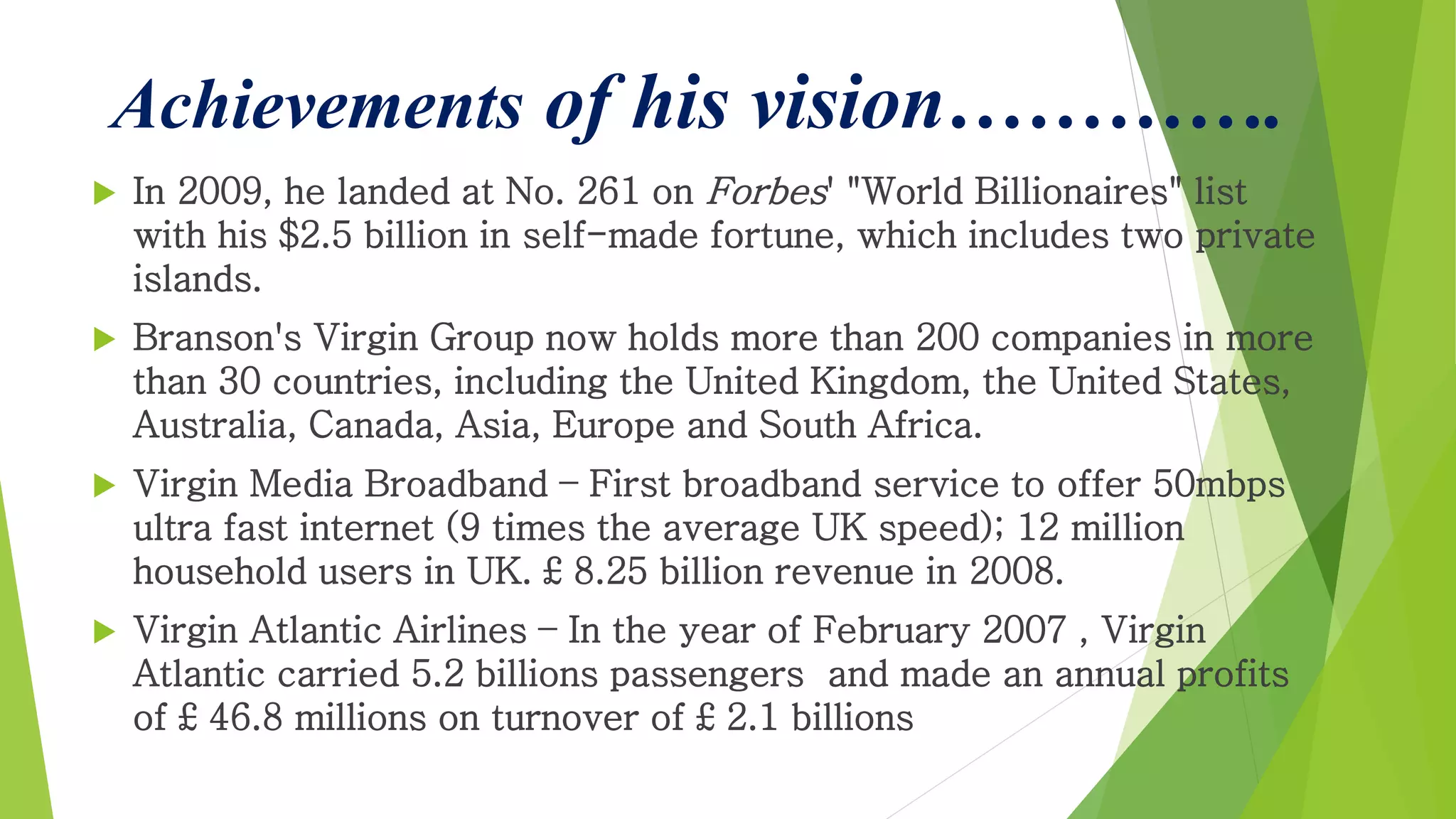

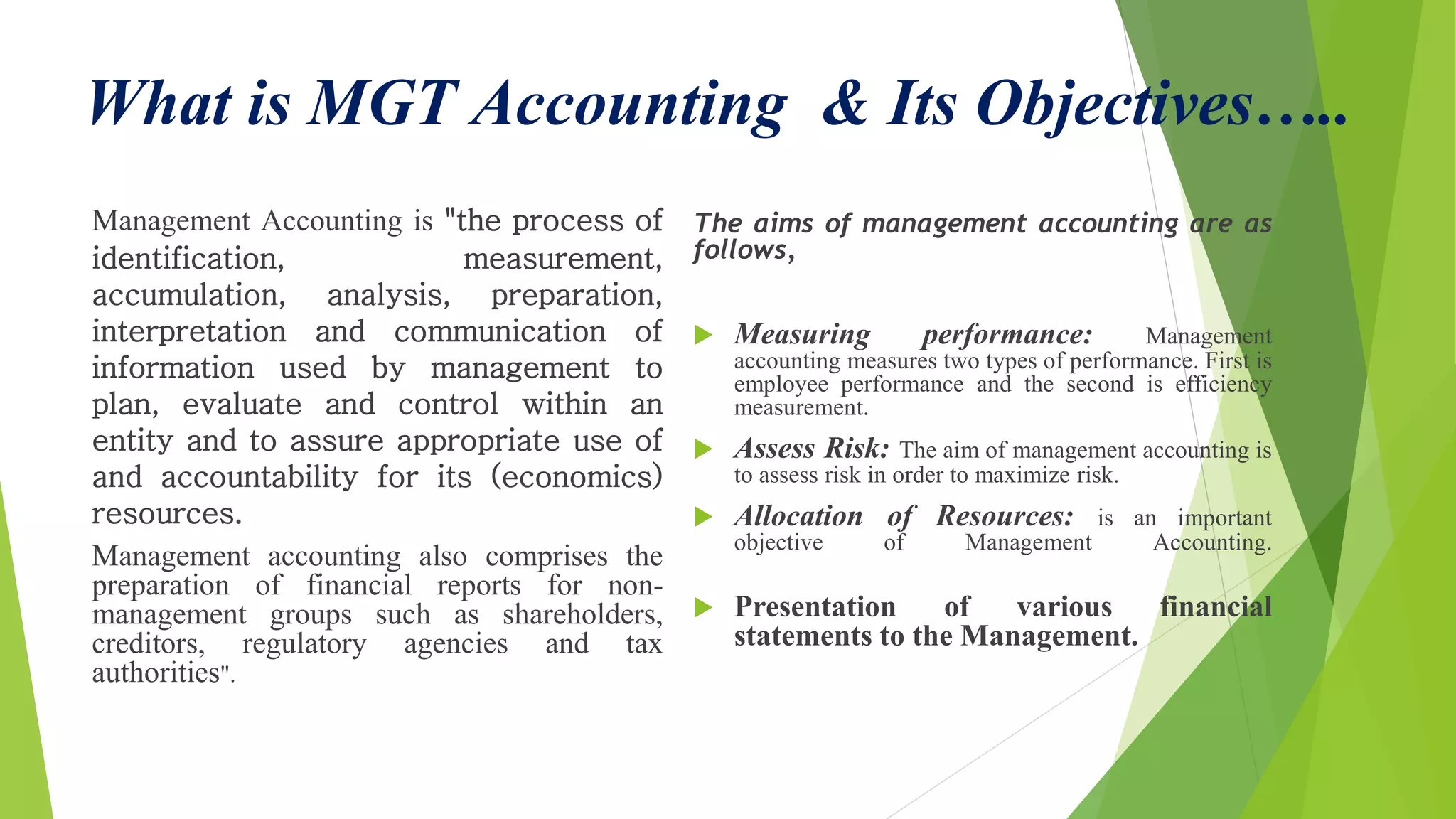

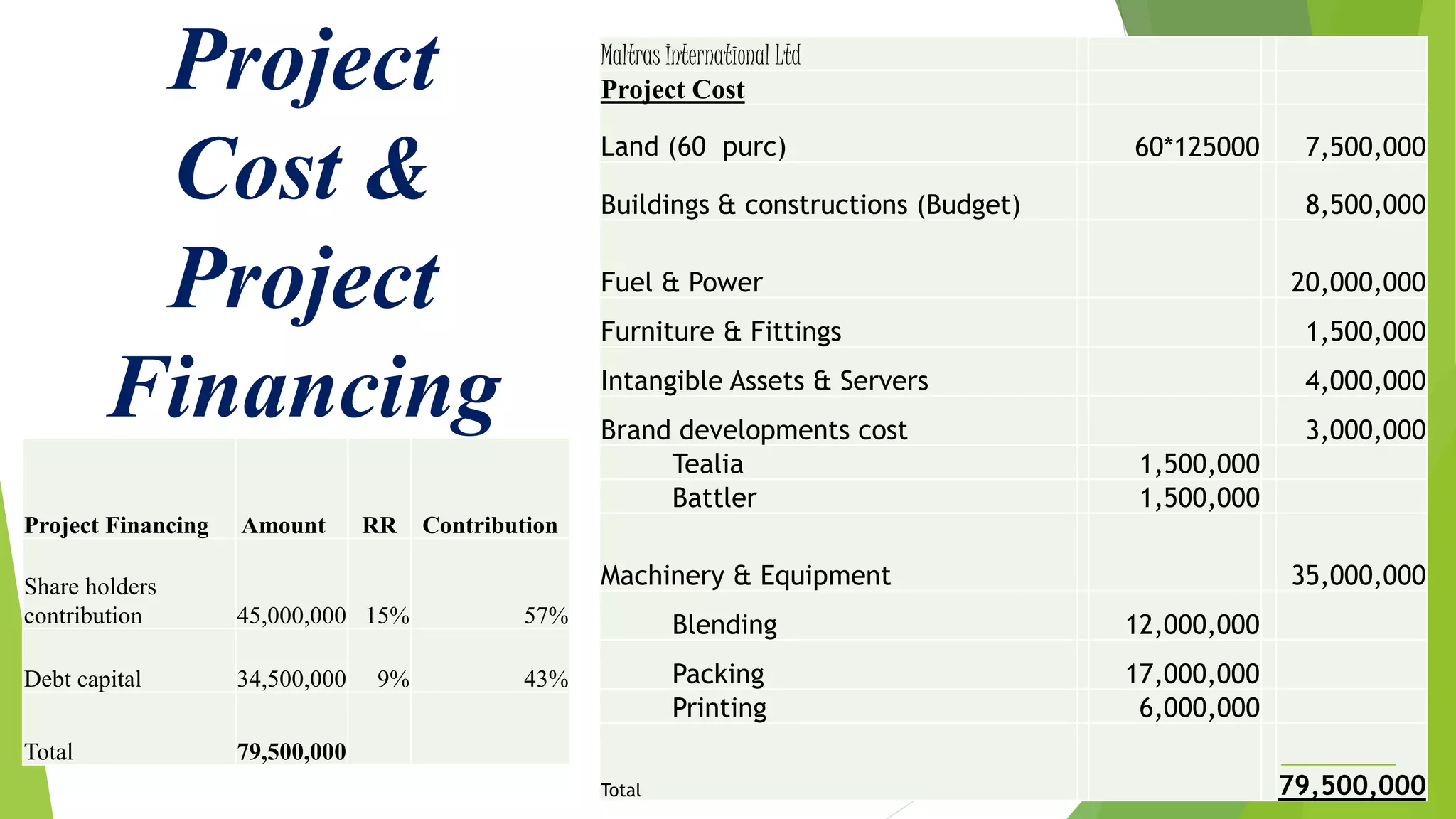

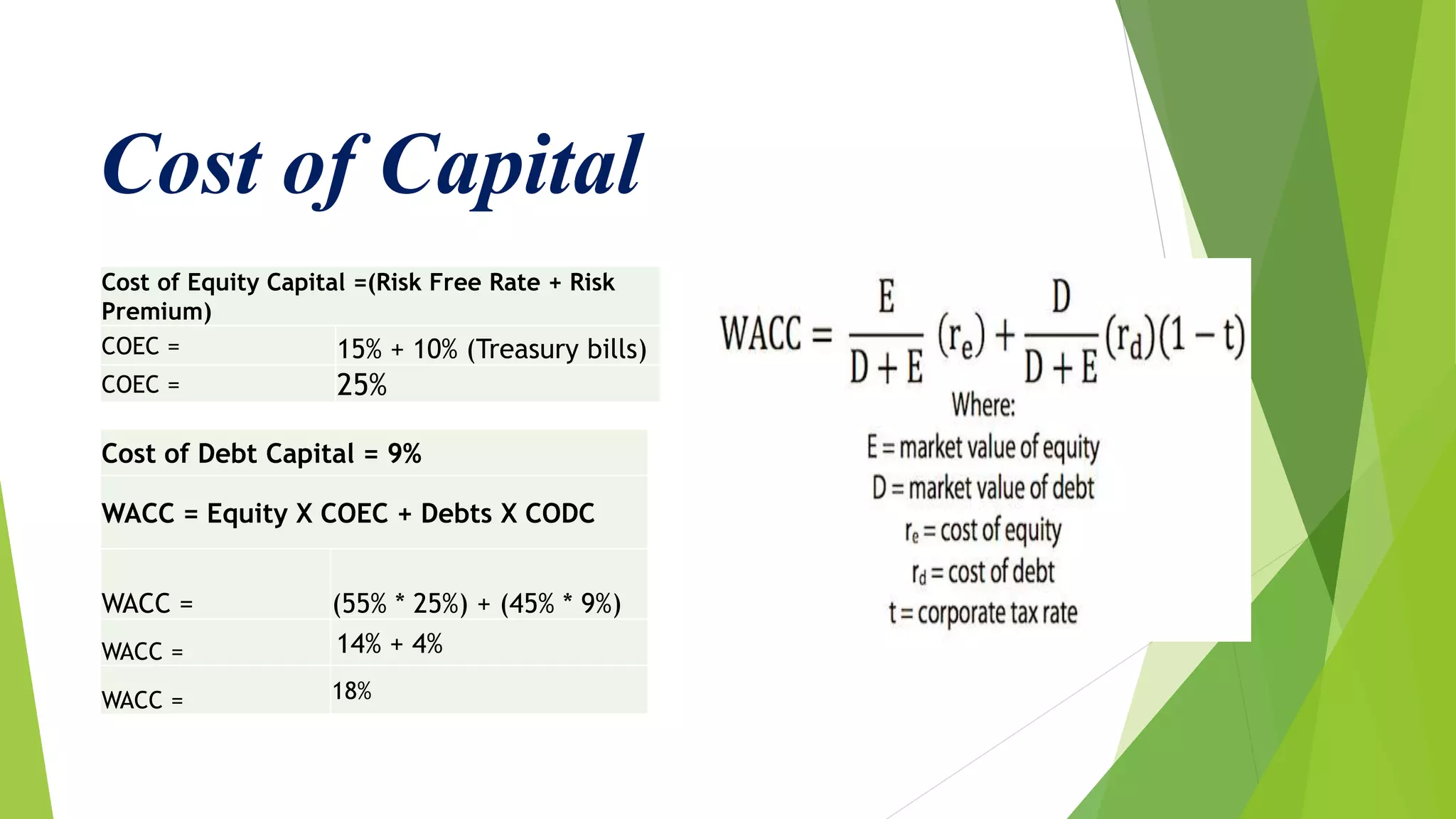

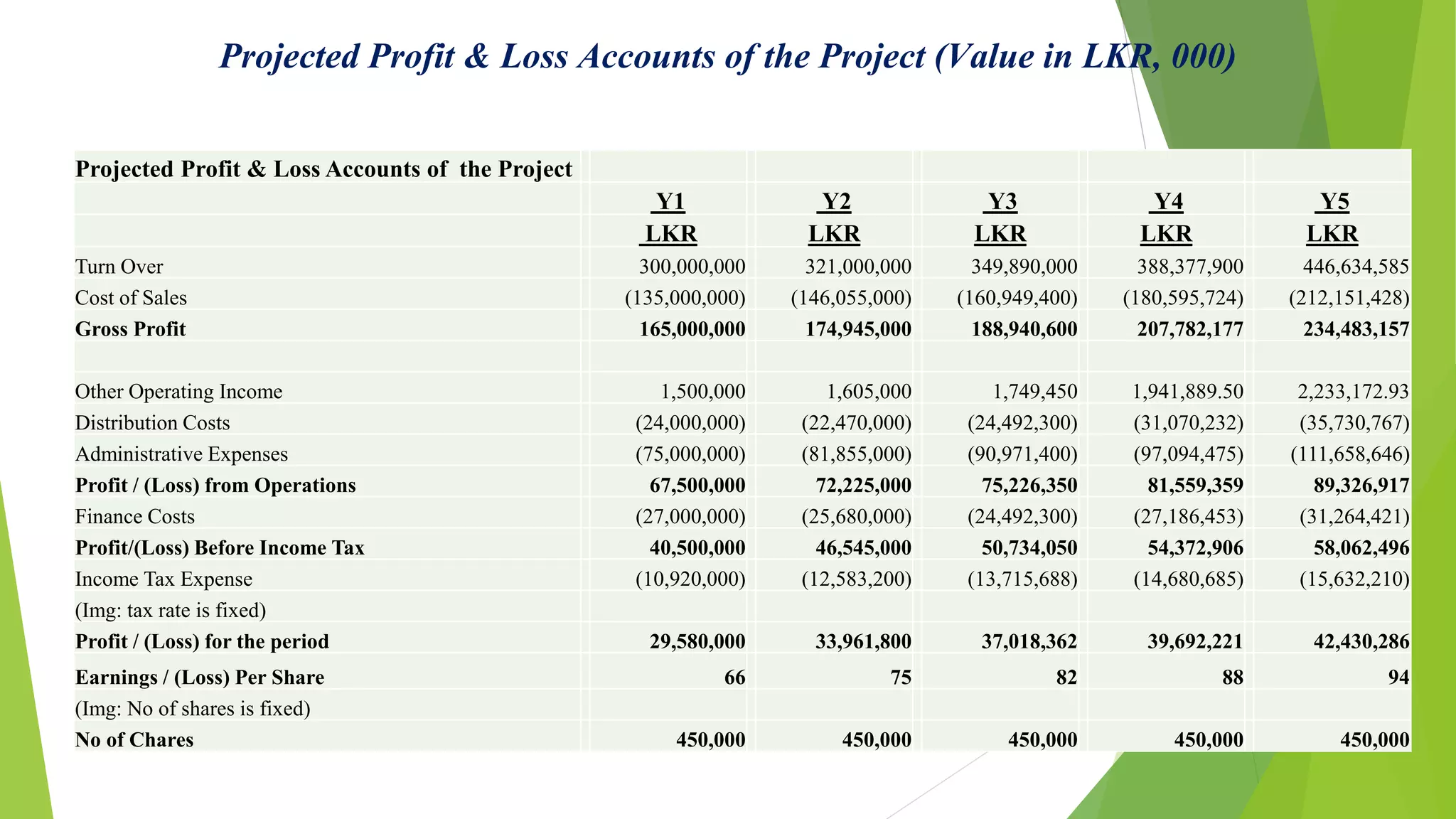

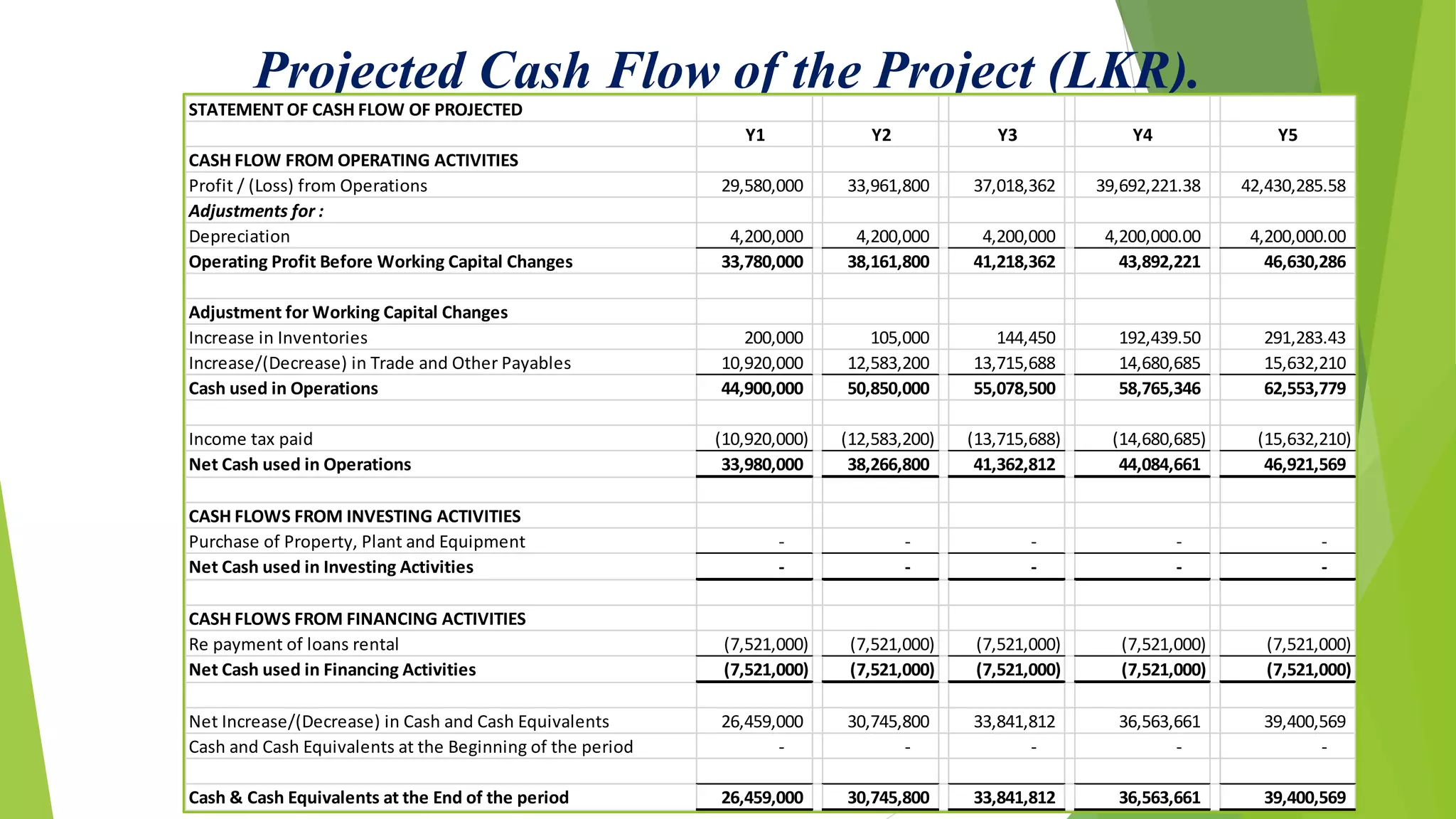

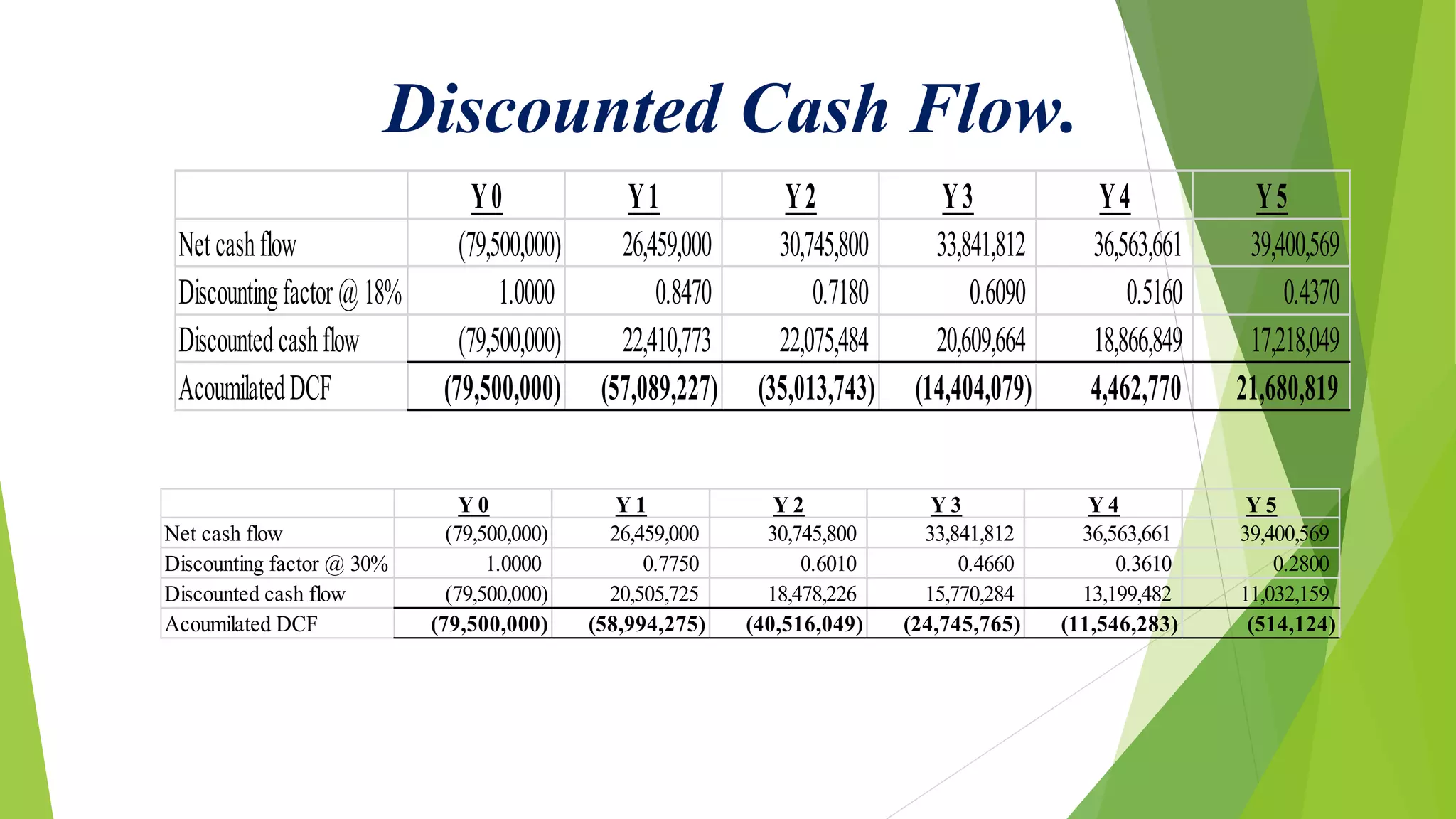

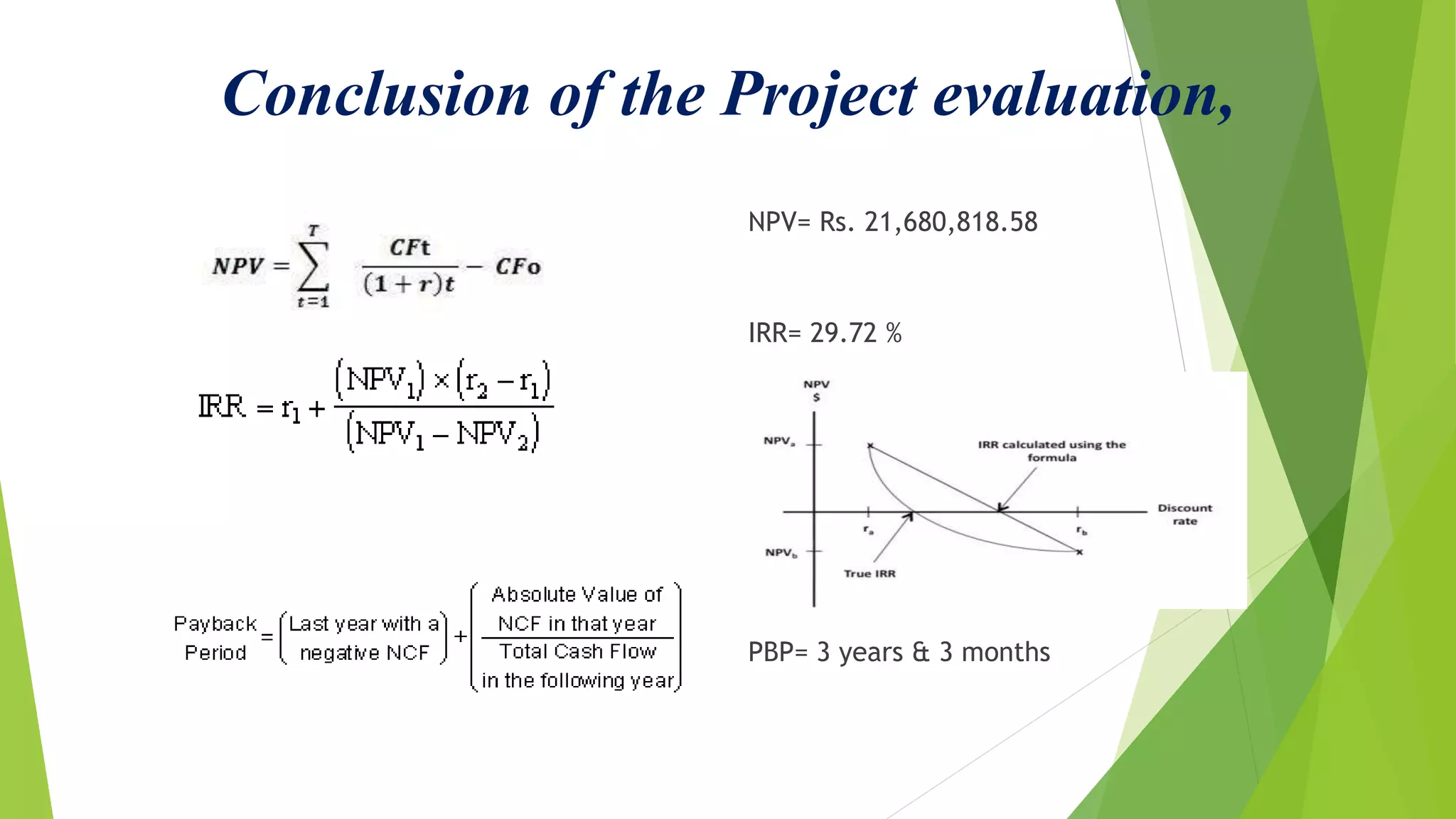

The document provides a summary of a presentation on investment appraisal and capital budgeting. It discusses Richard Branson's approach to starting businesses without extensive accounting involvement. It then summarizes the objectives and limitations of management accounting. The document outlines a proposed tea production and export project for Maltras International Ltd, including project costs, financing, financial projections, cash flow statements, and investment appraisal calculations. Based on the discounted cash flow analysis, the project has a positive net present value of Rs. 21,680,818, indicating it should be accepted.