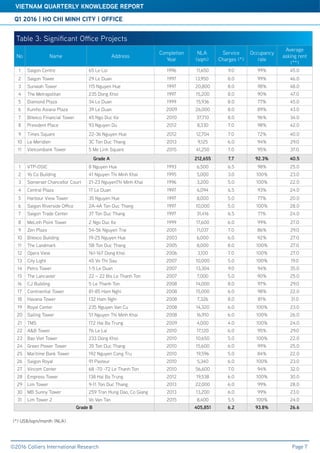

Downloaded 10 times

The Q1 2016 report highlights Vietnam's GDP growth at 5.46%, a decrease from the previous year, with notable growth in services and industrial sectors, while the agriculture sector saw a decline. Foreign direct investment saw a significant increase of 119.1% y-o-y, and retail sales grew by 9.1% y-o-y, indicating a robust consumer market. However, Ho Chi Minh City experienced a decrease in new FDI capital, and both the city and Hanoi faced challenges in agricultural growth amidst rising consumer prices.