Objectives

At the endof this lesson, the students

should be able to:

• Identify the components and

formats of the income statement and

cash flow statement

• Differentiate revenue recognition

and expense recognition

• Determine the nonrecurring items

and non-operating items

• Analyze income and cash flow

statements

3.

Income Statement

Components

are thedirect costs of producing

the goods being offered by the

entity. This would include the

materials, labor, and other

resources required for

production.

Cost of Goods Sold

is the money an entity receives from

the sale of goods or services. Other

terms frequently used for revenue

are sales, net sales, or sale revenue.

It is also referred to as the “top line”

because revenues are reported at

the top of the income statement.

Revenue

4.

Income Statement

Components

are theamount an entity

expends to maintain and

operate the general business.

Operating expenses include

research and development,

marketing, general and

administrative, amortization of

intangible assets (i.e. patents,

good will, etc.), etc.

Operating Expenses

is the difference between the

revenue received for the product

less the cost of goods sold.

Gross Profit

5.

Income Statement

Components

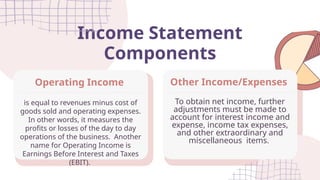

To obtainnet income, further

adjustments must be made to

account for interest income and

expense, income tax expenses,

and other extraordinary and

miscellaneous items.

Other Income/Expenses

is equal to revenues minus cost of

goods sold and operating expenses.

In other words, it measures the

profits or losses of the day to day

operations of the business. Another

name for Operating Income is

Earnings Before Interest and Taxes

(EBIT).

Operating Income

6.

Income Statement

Components

Revenues minusall expenses equals

net income (profits or losses). Profits

are also referred to as net income or

the “bottom line” because profits are

reported at the bottom of the

income statement.

Profits

7.

Income

Statement

Formats

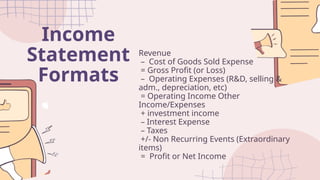

Revenue

– Cost ofGoods Sold Expense

= Gross Profit (or Loss)

– Operating Expenses (R&D, selling &

adm., depreciation, etc)

= Operating Income Other

Income/Expenses

+ investment income

– Interest Expense

– Taxes

+/- Non Recurring Events (Extraordinary

items)

= Profit or Net Income

9.

The purpose ofthe income

statement is to provide the financial

earnings performance of the entity

over a specific period of time. It is

also referred to as a profit and loss

statement or earnings statement.

Purpose of the

Income Statement

10.

WHAT IS REVENUE

RECOGNITIONPRINCIPLE?

Revenue recognition is a generally accepted

accounting principle (GAAP) that identifies the

specific conditions in which revenue is

recognized and determines how to account for

it. Typically, revenue is recognized when a

critical event has occurred, and the dollar

amount is easily measurable to the company.

11.

WHAT IS REVENUE

RECOGNITIONPRINCIPLE?

On May 28, 2014, the Financial Accounting

Standards Board (FASB) and International

Accounting Standards Board (IASB) jointly

issued Accounting Standards Codification (ASC)

606, regarding revenue from contracts with

customers. ASC 606 provides a uniform

framework for recognizing revenue from

contracts with customers.

12.

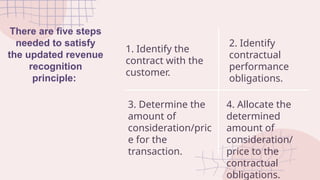

There are fivesteps

needed to satisfy

the updated revenue

recognition

principle:

1. Identify the

contract with the

customer.

2. Identify

contractual

performance

obligations.

3. Determine the

amount of

consideration/pric

e for the

transaction.

4. Allocate the

determined

amount of

consideration/

price to the

contractual

obligations.

13.

There are fivesteps

needed to satisfy

the updated revenue

recognition

principle:

5. Recognize

revenue when the

performing party

satisfies the

performance

obligation

14.

What is Expense

RecognitionPrinciple?

The expense recognition principle states

that expenses should be recognized in the

same period as the revenues to which they

relate. If this were not the case, expenses

would likely be recognized as incurred, which

might predate or follow the period in which the

related amount of revenue is recognized.

15.

What is Expense

RecognitionPrinciple?

This principle also has an impact on the

timing of income taxes. In the example, income

taxes will be underpaid in the current month,

since expenses are too high, and overpaid in

the following month, when expenses are too

low.

16.

When to Usethe Expense

Recognition Principle?

The expense recognition principle is a core

element of the accrual basis of accounting,

which holds that revenues are recognized when

earned and expenses when consumed. If a

business were to instead recognize expenses

when it pays suppliers, this is known as the

cash basis of accounting.

17.

When to Usethe Expense

Recognition Principle?

If a company wants to have its financial

statements audited, it must use the expense

recognition principle when recording business

transactions. Otherwise, the auditors will refuse

to render an opinion on the financial

statements.

18.

Nonrecurring Items and

Non-OperatingItems

There are four types of non-recurring items

in an income statement.

1. Discontinued operations

Discontinued operations are not

a component of persistent or

recurring net income from

continuing operations. To qualify,

the assets, results of operations, and

investing and financing activities of a

business segment must be

separable from those of the

company.

19.

Nonrecurring Items and

Non-OperatingItems

There are four types of non-recurring items

in an income statement.

2. Extraordinary items

Extraordinary items are both

unusual in nature and infrequent in

occurrence, and material in amount.

They must be reported separately

(below the line) net of income tax.

20.

Nonrecurring Items and

Non-OperatingItems

There are four types of non-recurring items

in an income statement.

3. Unusual or infrequent items

These are either unusual in nature or

infrequent in occurrence but not both.

They may be disclosed separately (as a

single-line item) as a component of

income from continuing operations. They

are reported pre-tax in the income

statement and appear "above the line,"

while the other three categories are

reported on an after-tax basis and "below

the line" and excluded from net income

from continuing operations.

21.

Nonrecurring Items and

Non-OperatingItems

There are four types of non-recurring items

in an income statement.

4. Changes in accounting

principles

Changes in accounting principles,

such as from LIFO to another inventory

method or from the percentage-of-

completion method to the completed-

contract method, can be either voluntary

changes or changes mandated by new

accounting standards.

22.

Nonrecurring Items and

Non-OperatingItems

There are four types of non-recurring items

in an income statement.

4. Changes in accounting

principles

Changes in accounting estimates,

such as changes in asset lives or salvage

value when recording depreciation

expenses, are not considered changes in

accounting principles. The impact of such

a change is only prospective, and no

retroactive or cumulative effects are

recognized. A change from an incorrect to

an acceptable accounting method is

treated as an error and its impact is

reported as a prior period adjustment.

23.

Nonrecurring Items and

Non-OperatingItems

Non-operating Items: Investing and

Financing Activities

Non-operating items are reported

separately from operating items.

For example, if a non-financial service

company invests in equity or debt

securities issued by another company,

any interest, dividends, or profits from

sales of these securities will be shown as

non-operating income.

24.

Analysis of Income

Statement

Investorscan use income statement

analysis to calculate financial ratios that can be

used to compare the same company year over

year, or to compare one company to another.

25.

Analysis of Income

Statement

Forinstance, you can compare one

company's profits to those of its competitors by

looking at a number of figures that express

margins, such as gross profit margin, operating

profit margin, and net profit margin. Or you

could compare one company's earnings per

share (EPS) to any other's, to show you what a

shareholder would receive per share in the

event that assets were made liquid, or if each

company were to distribute its net income.

26.

Analysis of Income

Statement

Whenyou compare each line up and down

the statement to the top line (which is revenue),

this is called "vertical analysis." Each line item

becomes a percentage of a base figure. This

method can be used to compare one line item

to another very simply, such as to check how

each may affect cash flow, or it can be used to

show how the cost of one line item stands up

against the cost of any other.

• Vertical Analysis

27.

Analysis of Income

Statement

Thismethod is most often used for spotting

trends. A single line item can be looked at over

a long span of time, to view changes from year

to year. For instance, you might wish to hone in

on what factors may be driving a certain

company's success (or failure) over the last few

years. Some investors use this method to

predict how well a company will perform in the

months or years to come.

• Horizontal Analysis

28.

Analysis of Income

Statement

Becauseincome statements have a few

limits, they may not always be the best source

to consult. It depends on what you're looking

for. Capital structure and cash flow, just to

name two, can make or break a firm, and you'll

want to have correct figures.

Limits of Income Statements

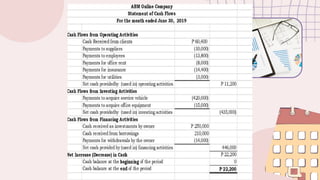

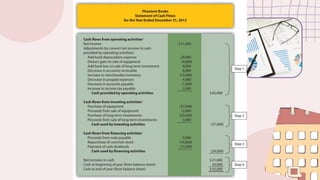

A cash flowstatement is a financial statement that

summarizes the amount of cash and cash equivalents

entering and leaving a company.

The cash flow statement measures how well a

company manages its cash position, meaning how

well the company generates cash to pay its debt

obligations and fund its operating expenses.

The cash flow statement complements the balance

sheet and income statement and is a mandatory part

of a company's financial reports since 1987

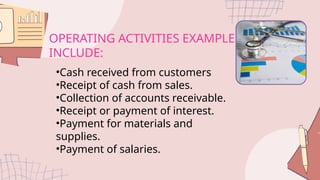

OPERATING ACTIVITIES EXAMPLES

INCLUDE:

•Cashreceived from customers

•Receipt of cash from sales.

•Collection of accounts receivable.

•Receipt or payment of interest.

•Payment for materials and

supplies.

•Payment of salaries.

34.

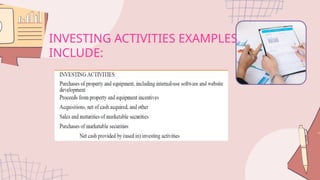

INVESTING

ACTIVITIES

Any cash flowsfrom the acquisition

and disposal of longterm assets and

other investments not included in

cash equivalents

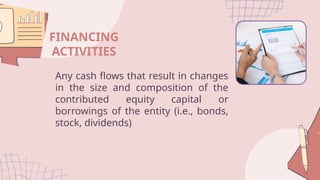

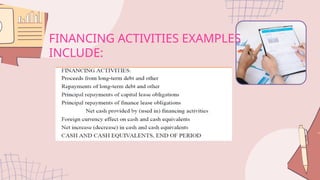

FINANCING

ACTIVITIES

Any cash flowsthat result in changes

in the size and composition of the

contributed equity capital or

borrowings of the entity (i.e., bonds,

stock, dividends)

Two Methods of

CalculatingCash Flow

The direct method adds up all the various types of cash

payments and receipts, including cash paid to

suppliers, cash receipts from customers, and cash paid

out in salaries. These figures are calculated by using

the beginning and ending balances of a variety of

business accounts and examining the net decrease or

increase in the accounts.

Direct Method

40.

Two Methods of

CalculatingCash Flow

With the indirect method, cash flow from operating

activities is calculated by first taking the net income off

of a company's income statement. Because a

company’s income statement is prepared on an accrual

basis, revenue is only recognized when it is earned and

not when it is received.

Indirect Method

42.

Cash Flow Statement

Analysis

Acash flow analysis determines a company’s

working capital—the amount of money

available to run business operations and

complete transactions. That is calculated as

current assets (cash or near-cash assets, like

notes receivable) minus current liabilities

(liabilities due during the upcoming accounting

period). Analysis of working capital provides a

snapshot of the liquidity of the business.

43.

Five Steps toCash

Flow Analysis

There are a few major items to look out for trends and outliers

that can tell you a lot about the health of the business.

When operating income exceeds net income,

it’s a strong indicator of a company’s ability to

remain solvent and sustainably grow its

operations

1. Aim for positive cash flow

44.

Five Steps toCash

Flow Analysis

There are a few major items to look out for trends and outliers

that can tell you a lot about the health of the business.

On the other hand, positive investing cash flow

and negative operating cash flow could signal

problems. For example, it could indicate a

company is selling off assets to pay its

operating expenses, which is not always

sustainable.

2. Be circumspect about positive cash flow

45.

Five Steps toCash

Flow Analysis

There are a few major items to look out for trends and outliers

that can tell you a lot about the health of the business.

When it comes to investing cash flow analysis, negative

cash flow isn’t necessarily a bad thing. It could mean the

business is making investments in property and

equipment to make more products. A positive operating

cash flow and a negative investing cash flow could mean

the company is making money and spending it to grow.

3. Analyze your negative cash flow

46.

Five Steps toCash

Flow Analysis

There are a few major items to look out for trends and outliers

that can tell you a lot about the health of the business.

What you have left after you pay for operating

expenditures and capital expenditures is free cash flow.

This can be used to pay down principal, interest, buy back

stock or acquire another company.

4. Calculate your free cash flow

47.

Five Steps toCash

Flow Analysis

There are a few major items to look out for trends and outliers

that can tell you a lot about the health of the business.

The operating cash flow margin ratio measures cash from

operating activities as a percentage of sales revenue in a

given period. A positive margin demonstrates profitability,

efficiency and earnings quality.

5. Operating cash flow margin builds trust

48.

Conclusion

Cash flow analysishelps your

finance team better manage

cash inflow and cash outflow,

ensuring that there will be

enough money to run—and

grow—the business.