Downloaded 237 times

![Let us see the formula of the Current Account Balance (CAB)

CAB = X - M + NI + NCT

X = Exports of goods and services

M = Imports of goods and services

NI = Net income abroad [Salaries paid or received,

credit / debit of income from

FII & FDI etc. ]

NCT = Net current transfers [Workers' Remittances

(unilateral),

Donations, Aids & Grants,

Official, Assistance and

Pensions etc]

CURRENT ACCOUNT DEFICIT

What are its objectives?

GOLD MONETIZATION SCHEME](https://image.slidesharecdn.com/gold-monetization-scheme-150703111313-lva1-app6891/75/Gold-monetization-scheme-8-2048.jpg)

![Let us see the formula of the Current Account Balance (CAB)

CAB = X - M + NI + NCT

X = Exports of goods and services

M = Imports of goods and services

NI = Net income abroad [Salaries paid or received,

credit / debit of income from

FII & FDI etc. ]

NCT = Net current transfers [Workers' Remittances

(unilateral),

Donations, Aids & Grants,

Official, Assistance and

Pensions etc]

CURRENT ACCOUNT DEFICIT

Hope you have understood the

concept of ‘Gold Monetization

Scheme’.

GOLD MONETIZATION SCHEME](https://image.slidesharecdn.com/gold-monetization-scheme-150703111313-lva1-app6891/75/Gold-monetization-scheme-23-2048.jpg)

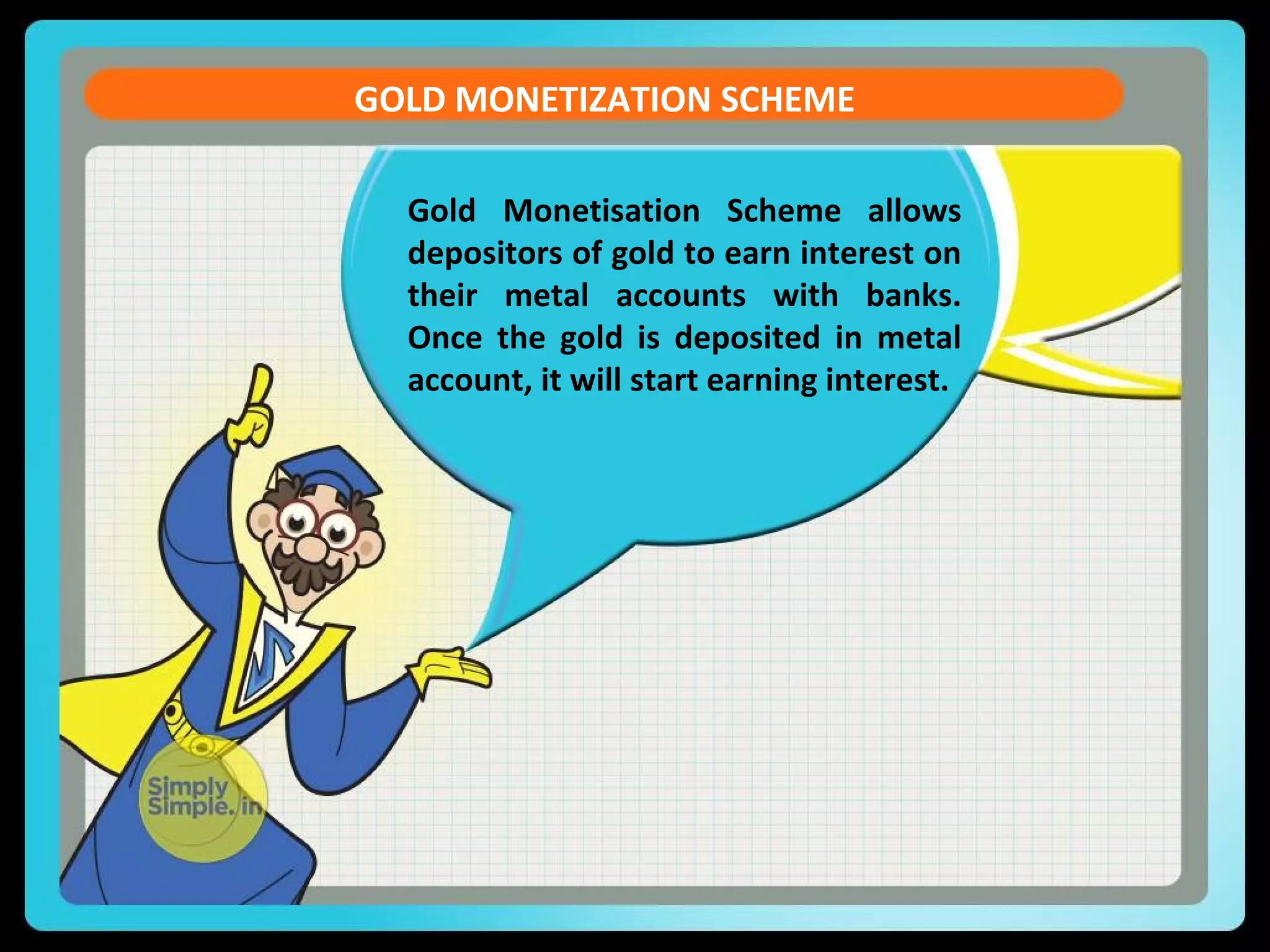

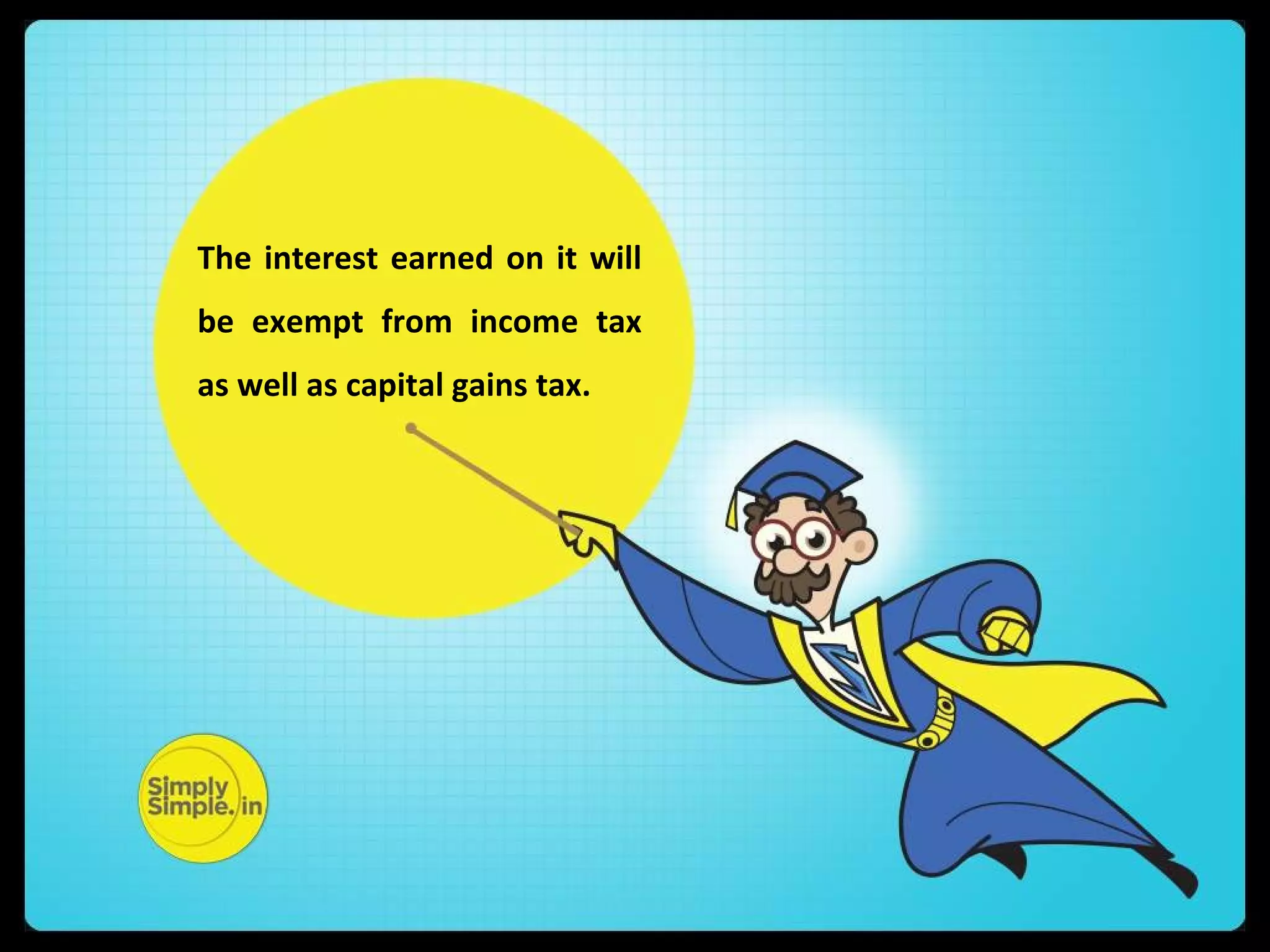

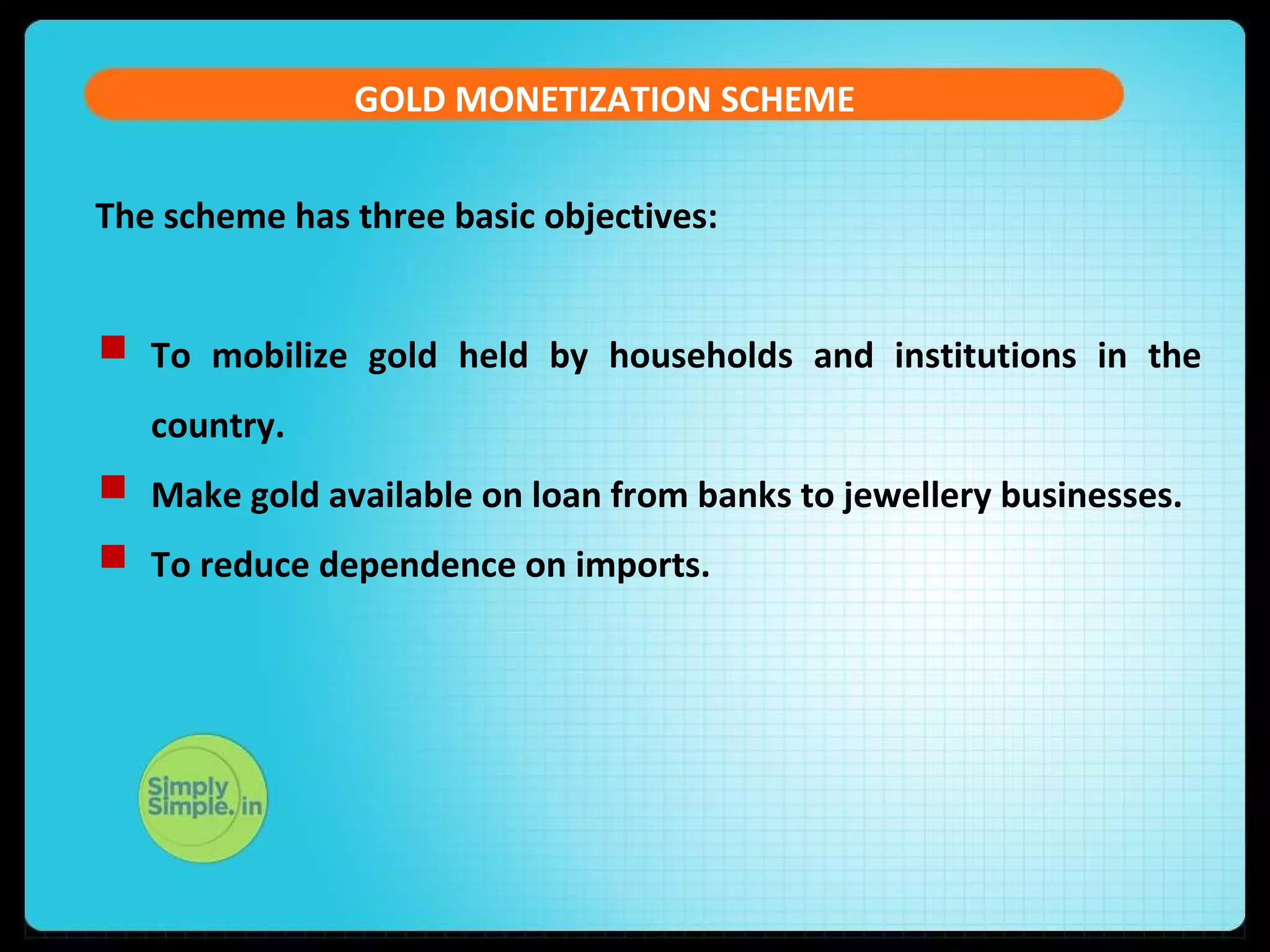

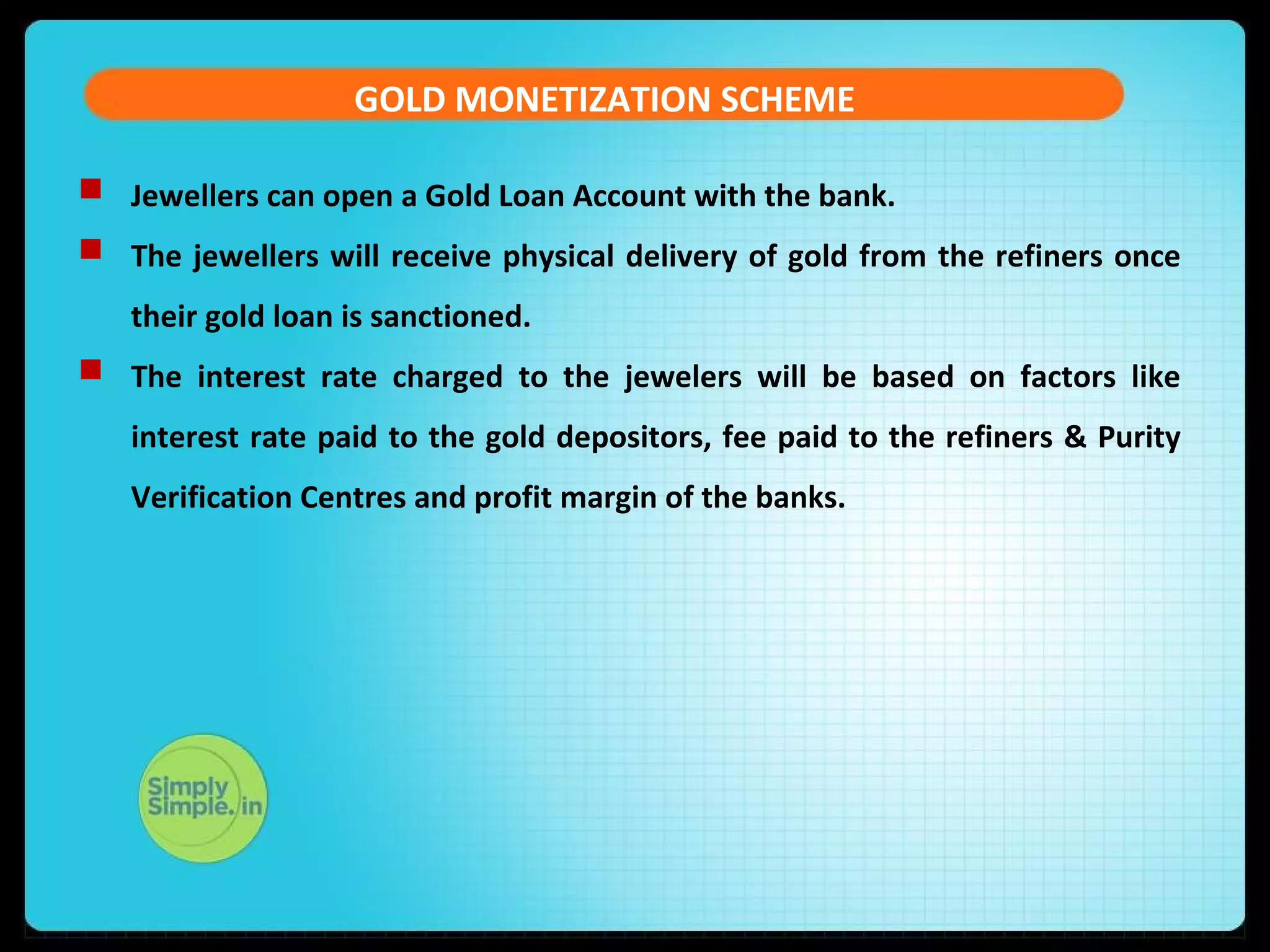

The document discusses India's Gold Monetization Scheme. It aims to reduce India's reliance on gold imports by mobilizing the estimated 20,000 tonnes of gold held by Indian households and institutions. Under the scheme, depositors can earn interest on gold deposited in bank metal accounts. The deposited gold can then be lent to jewelers. This would help reduce imports, increase recycling of domestic gold, and earn interest for depositors while providing jewelers access to gold to meet demand. The scheme's objectives are to mobilize household and institutional gold stocks, make gold available on loan to jewelers, and reduce dependence on imports.