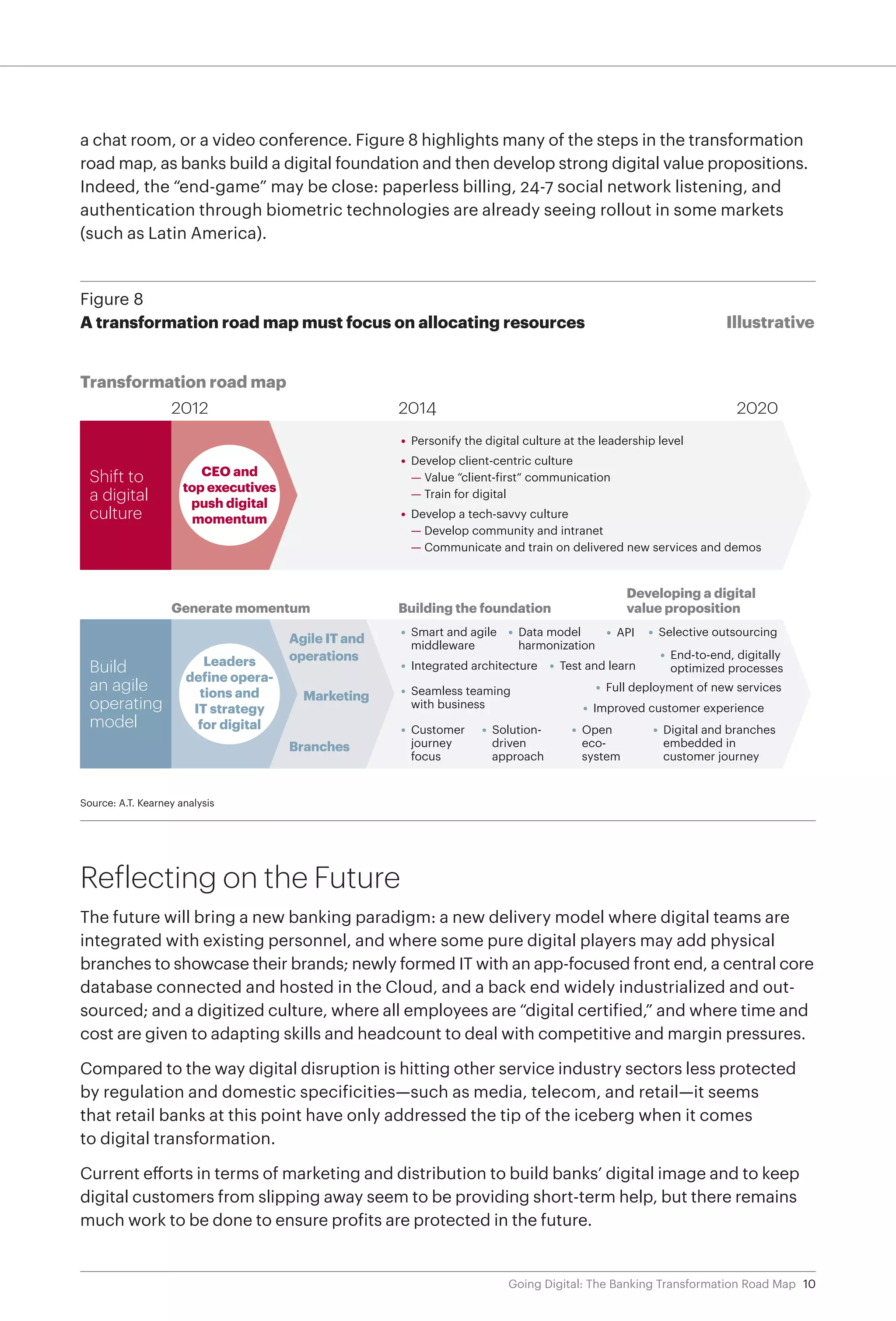

The document discusses the digital transformation occurring in the banking industry. It finds that digital banking leaders understand the importance of mobile, are developing more agile operating models, and have undertaken internal cultural shifts to be more customer-centric. These leaders are fundamentally changing their organizations to deliver the best customer experiences and results. The greatest challenge for banks will be changing internal mindsets and cultures to adapt to the digital age.