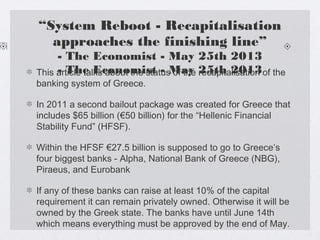

The document discusses the Greek debt crisis and banking system reboot. It describes how Greece was found to have understated its public debt for years, which grew to €290 billion, quadruple the allowable ratio. This led Greece to receive two bailout packages from Eurozone countries and the IMF totaling €240 billion. The document then focuses on Greece's four largest banks - Alpha, NBG, Piraeus, and Eurobank - and the efforts to recapitalize them with €27.5 billion from the HFSF. It provides an update on each bank's progress in raising the required capital through June 14th deadline.

![Greece economy]](https://cdn.slidesharecdn.com/ss_thumbnails/greeceeconomy-100612023558-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)