Recommended

Recommended

More Related Content

Similar to FS-3FORD MOTOR COMPANY AND SUBSIDIARIESCONSOLIDATED INCO.docx

Similar to FS-3FORD MOTOR COMPANY AND SUBSIDIARIESCONSOLIDATED INCO.docx (20)

More from ericbrooks84875

More from ericbrooks84875 (20)

Recently uploaded

Recently uploaded (20)

FS-3FORD MOTOR COMPANY AND SUBSIDIARIESCONSOLIDATED INCO.docx

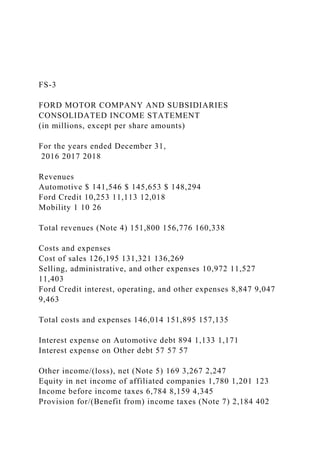

- 1. FS-3 FORD MOTOR COMPANY AND SUBSIDIARIES CONSOLIDATED INCOME STATEMENT (in millions, except per share amounts) For the years ended December 31, 2016 2017 2018 Revenues Automotive $ 141,546 $ 145,653 $ 148,294 Ford Credit 10,253 11,113 12,018 Mobility 1 10 26 Total revenues (Note 4) 151,800 156,776 160,338 Costs and expenses Cost of sales 126,195 131,321 136,269 Selling, administrative, and other expenses 10,972 11,527 11,403 Ford Credit interest, operating, and other expenses 8,847 9,047 9,463 Total costs and expenses 146,014 151,895 157,135 Interest expense on Automotive debt 894 1,133 1,171 Interest expense on Other debt 57 57 57 Other income/(loss), net (Note 5) 169 3,267 2,247 Equity in net income of affiliated companies 1,780 1,201 123 Income before income taxes 6,784 8,159 4,345 Provision for/(Benefit from) income taxes (Note 7) 2,184 402

- 2. 650 Net income 4,600 7,757 3,695 Less: Income/(Loss) attributable to noncontrolling interests 11 26 18 Net income attributable to Ford Motor Company $ 4,589 $ 7,731 $ 3,677 EARNINGS PER SHARE ATTRIBUTABLE TO FORD MOTOR COMPANY COMMON AND CLASS B STOCK (Note 8) Basic income $ 1.16 $ 1.94 $ 0.93 Diluted income 1.15 1.93 0.92 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (in millions) For the years ended December 31, 2016 2017 2018 Net income $ 4,600 $ 7,757 $ 3,695 Other comprehensive income/(loss), net of tax (Note 21) Foreign currency translation (1,024) 314 (523) Marketable securities (8) (34) (11) Derivative instruments 219 (265) 183 Pension and other postretirement benefits 56 37 (56) Total other comprehensive income/(loss), net of tax (757) 52 (407) Comprehensive income 3,843 7,809 3,288 Less: Comprehensive income/(loss) attributable to noncontrolling interests 10 24 18 Comprehensive income attributable to Ford Motor Company $ 3,833 $ 7,785 $ 3,270 The accompanying notes are part of the consolidated financial statements.

- 3. FS-4 FORD MOTOR COMPANY AND SUBSIDIARIES CONSOLIDATED BALANCE SHEET (in millions) December 31, 2017 December 31, 2018 ASSETS Cash and cash equivalents (Note 9) $ 18,492 $ 16,718 Marketable securities (Note 9) 20,435 17,233 Ford Credit finance receivables, net (Note 10) 52,210 54,353 Trade and other receivables, less allowances of $412 and $94 10,599 11,195 Inventories (Note 12) 11,176 11,220 Other assets 3,889 3,930 Total current assets 116,801 114,649 Ford Credit finance receivables, net (Note 10) 56,182 55,544 Net investment in operating leases (Note 13) 28,235 29,119 Net property (Note 14) 35,327 36,178 Equity in net assets of affiliated companies (Note 15) 3,085 2,709 Deferred income taxes (Note 7) 10,762 10,412 Other assets 8,104 7,929

- 4. Total assets $ 258,496 $ 256,540 LIABILITIES Payables $ 23,282 $ 21,520 Other liabilities and deferred revenue (Note 16) 19,697 20,556 Automotive debt payable within one year (Note 18) 3,356 2,314 Ford Credit debt payable within one year (Note 18) 48,265 51,179 Total current liabilities 94,600 95,569 Other liabilities and deferred revenue (Note 16) 24,711 23,588 Automotive long-term debt (Note 18) 12,575 11,233 Ford Credit long-term debt (Note 18) 89,492 88,887 Other long-term debt (Note 18) 599 600 Deferred income taxes (Note 7) 815 597 Total liabilities 222,792 220,474 Redeemable noncontrolling interest (Note 20) 98 100 EQUITY Common Stock, par value $.01 per share (4,000 million shares issued of 6 billion authorized) 40 40 Class B Stock, par value $.01 per share (71 million shares issued of 530 million authorized) 1 1 Capital in excess of par value of stock 21,843 22,006 Retained earnings 21,906 22,668 Accumulated other comprehensive income/(loss) (Note 21) (6,959) (7,366) Treasury stock (1,253) (1,417) Total equity attributable to Ford Motor Company 35,578 35,932 Equity attributable to noncontrolling interests 28 34 Total equity 35,606 35,966

- 5. Total liabilities and equity $ 258,496 $ 256,540 The following table includes assets to be used to settle liabilities of the consolidated variable interest entities (“VIEs”). These assets and liabilities are included in the consolidated balance sheet above. See Note 22 for additional information on our VIEs. December 31, 2017 December 31, 2018 ASSETS Cash and cash equivalents $ 3,479 $ 2,728 Ford Credit finance receivables, net 56,250 58,662 Net investment in operating leases 11,503 16,332 Other assets 64 27 LIABILITIES Other liabilities and deferred revenue $ 2 $ 24 Debt 46,437 53,269 The accompanying notes are part of the consolidated financial statements. FS-5 FORD MOTOR COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENT OF CASH FLOWS (in millions) For the years ended December 31,

- 6. 2016 2017 2018 Cash flows from operating activities Net income $ 4,600 $ 7,757 $ 3,695 Depreciation and tooling amortization 9,023 9,122 9,280 Other amortization (306) (669) (972) Provision for credit and insurance losses 672 717 609 Pension and other postretirement employee benefits (“OPEB”) expense/(income) 2,667 (608) 400 Equity investment (earnings)/losses in excess of dividends received (178) 240 206 Foreign currency adjustments 283 (403) 529 Net (gain)/loss on changes in investments in affiliates (139) (7) (42) Stock compensation 210 246 191 Net change in wholesale and other receivables (1,449) (836) (2,408) Provision for deferred income taxes 1,473 (350) (197) Decrease/(Increase) in accounts receivable and other assets (2,855) (2,297) (2,239) Decrease/(Increase) in inventory (803) (970) (828) Increase/(Decrease) in accounts payable and accrued and other liabilities 6,595 6,089 6,781 Other 57 65 17 Net cash provided by/(used in) operating activities 19,850 18,096 15,022 Cash flows from investing activities Capital spending (6,992) (7,049) (7,785) Acquisitions of finance receivables and operating leases (56,007) (59,354) (62,924) Collections of finance receivables and operating leases 38,834 44,641 50,880 Purchases of marketable and other securities (31,428) (27,567) (17,140) Sales and maturities of marketable and other securities 29,354

- 7. 29,898 20,527 Settlements of derivatives 825 100 358 Other 112 (29) (177) Net cash provided by/(used in) investing activities (25,302) (19,360) (16,261) Cash flows from financing activities Cash dividends (3,376) (2,584) (2,905) Purchases of common stock (145) (131) (164) Net changes in short-term debt 3,864 1,229 (2,819) Proceeds from issuance of long-term debt 45,961 45,801 50,130 Principal payments on long-term debt (38,797) (40,770) (44,172) Other (107) (151) (192) Net cash provided by/(used in) financing activities 7,400 3,394 (122) Effect of exchange rate changes on cash, cash equivalents, and restricted cash (265) 489 (370) Net increase/(decrease) in cash, cash equivalents, and restricted cash $ 1,683 $ 2,619 $ (1,731) Cash, cash equivalents, and restricted cash at January 1 (Note 9) $ 14,336 $ 16,019 $ 18,638 Net increase/(decrease) in cash, cash equivalents, and restricted cash 1,683 2,619 (1,731) Cash, cash equivalents, and restricted cash at December 31 (Note 9) $ 16,019 $ 18,638 $ 16,907 The accompanying notes are part of the consolidated financial statements. FS-6

- 8. FORD MOTOR COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENT OF EQUITY (in millions) Equity Attributable to Ford Motor Company Capital Stock Cap. in Excess of Par Value of Stock Retained Earnings/ (Accumulated Deficit) Accumulated Other Comprehensive Income/(Loss) (Note 21)

- 9. Treasury Stock Total Equity Attributable to Non- controlling Interests Total Equity Balance at December 31, 2015 $ 41 $ 21,421 $ 14,980 $ (6,257) $ (977) $ 29,208 $ 15 $ 29,223 Net income — — 4,589 — — 4,589 11 4,600 Other comprehensive income/(loss), net of tax — — — (756) — (756) (1) (757) Common stock issued (including share- based compensation impacts) — 209 — — — 209 — 209 Treasury stock/other — — — — (145) (145) (3) (148) Cash dividends declared (a) — — (3,376) — — (3,376) (5) (3,381) Balance at December 31, 2016 $ 41 $ 21,630 $ 16,193 $ (7,013) $ (1,122) $ 29,729 $ 17 $ 29,746 Balance at December 31, 2016 $ 41 $ 21,630 $ 16,193 $ (7,013) $ (1,122) $ 29,729 $ 17 $ 29,746 Adoption of accounting standards — 6 566 — — 572 — 572 Net income — — 7,731 — — 7,731 26 7,757 Other comprehensive income/(loss), net of tax — — — 54 — 54 (2) 52

- 10. Common stock issued (including share- based compensation impacts) — 207 — — — 207 — 207 Treasury stock/other — — — — (131) (131) (2) (133) Cash dividends declared (a) — — (2,584) — — (2,584) (11) (2,595) Balance at December 31, 2017 $ 41 $ 21,843 $ 21,906 $ (6,959) $ (1,253) $ 35,578 $ 28 $ 35,606 Balance at December 31, 2017 $ 41 $ 21,843 $ 21,906 $ (6,959) $ (1,253) $ 35,578 $ 28 $ 35,606 Net income — — 3,677 — — 3,677 18 3,695 Other comprehensive income/(loss), net of tax — — — (407) — (407) — (407) Common stock issued (including share- based compensation impacts) — 163 — — — 163 — 163 Treasury stock/other — — — — (164) (164) — (164) Dividend and dividend equivalents declared (a) — — (2,915) — — (2,915) (12) (2,927) Balance at December 31, 2018 $ 41 $ 22,006 $ 22,668 $ (7,366) $ (1,417) $ 35,932 $ 34 $ 35,966 (a) We declared dividends per share of Common and Class B Stock of $0.85, $0.65, and $0.73 per share in 2016, 2017, and 2018, respectively. The accompanying notes are part of the consolidated financial statements. 1. The Research paper will come in five parts. The instructions are:

- 11. RESEARCH PAPER TOPIC Impact of Women in Missions History . Part 1: Proposed topic, abstract, and three sources - Topic must be approved by the instructor. A list of possible topics will be made available. Include at least three sources to make sure there will be enough resources to draw on. Submit Part 1 by 11:59 p.m. (ET) on Sunday of Module/Week 2. YOU ALREADY COMPLETED . Part 2: Refined topic, edited abstract, outline, and ten sources - Students will incorporate any changes to topic, outline the paper, write questions to be answered by the research, and submit ten sources. Submit Part 2 by 11:59 p.m. (ET) on Sunday of Module/Week 3. Note: Some will need to limit their topic. Others will need to expand their topic. This process should begin this week and continue until the final project is submitted. DUE SUNDAY, MAY 31ST . Part 3: Introduction and first five pages - Students will submit the introduction and first five pages of the research paper. Submit Part 3 by 11:59 p.m. (ET) on Sunday of Module/Week 4. DUE FRIDAY, JUNE 5TH . Part 4: Introduction and first ten pages - Students will submit introduction and first ten pages, incorporating changes made to

- 12. initial submission. Submit Part 4 by 11:59 p.m. (ET) on Sunday of Module/Week 5. DUE FRIDAY, JUNE 12TH . Part 5: Complete research paper - Students will submit the complete research paper. The paper will be 5000-6000 words in the body of the paper, with a minimum of ten academic resources cited. Submit Part 5 by 11:59 p.m. (ET) on Sunday of Module/Week 7 DUE FRIDAY, JUNE 19TH As previously stated, focus on a good introduction (the end goal should be no less than five well-written paragraphs of introduction), not on a complete abstract. The thesis statement should be one sentence in the introduction of the paper that defines what you seek to show by your research. When you write your abstract for the final draft, it will look slightly different. It should be included as a separate page. An academic abstract typically outlines four elements relevant to the completed work: . The research focus (i.e. statement of the problem(s)/research issue(s) addressed) . Your approach to the problem (biblical worldview, implications of issue) . The results/findings of the research . The main conclusions and recommendations As you can see from my description, you will not be able to write a good abstract until most of your research and writing are completed. After this week, leave a placeholder for the abstract and work on a good introduction to your topic. Remember Turabian format in every assignment that you submit. While I try to be lenient, I want you to get into the habit of documenting your sources properly. It is a good habit in research. If you run into difficulties, please ask for

- 13. clarification. We are here to learn from one another’s experiences and to interact with the scholars in our textbooks. We can do that in a positive and stimulating manner. At any point during the term, if you think that there is another source that can provide insight into the discussion, please include it with proper documentation. 3 LIBERTY UNIVERSITY SCHOOL OF DIVINITY RESEARCH PAPER TOPIC Impact of Women in Missions History Submitted to Dr. Philip Coppola in partial fulfillment of the requirements for the completion of GLST 650-B01 History and Theory of Global Engagement By Viktoria Taylor-Richardson May 27, 2020

- 14. ABSTRACT Traditionally, doing theology or mission work has always been the domain of men. However, since the times of Jesus, women have been involved in the spread of the gospel. For centuries, women have led in many crusades and missions, crossing the enemy lines and risking their lives to spread the word of God in many parts of the world. When the Samaritan woman met Jesus at the well, she ran back to her town and told her neighbors about Jesus as the Lord. According to the scriptures, women were the first at the tomb to learn of Jesus' resurrection. In the book of Acts, Priscilla gives theological directives to Apollos, a convert who later turned to be a key evangelist. During the first centuries of the church of Christ, dedicated widows, women martyrs, as well as virgins, were crucial supporters and witnesses of the gospel of Christ. In the early 1800s, women missionaries formed CENT societies were every woman contributed 52 cents every year. The money contributed helped start hospitals, training, and medical institutions. By 1812, some women were accompanying their husbands in missions to spread the gospel. In the 19th and 20th centuries, few names of women in missions, such as Stella Cox, Malla Moe, Alberta Skinner, and Gertrude Dyck stood out in the male- dominated field. Throughout history of the universal church, women have been key players in the spread of the gospel and the fulfillment of the Great Commission. Bibliography Butler, Anthea D. Women in the Church of God in Christ: Making a sanctified world. Univ of North Carolina Press, 2007. Reeves-Ellington, Barbara. "Women, Protestant Missions, and American Cultural Expansion, 1800 to 1938: A Historiographical Sketch." Social Sciences and Missions 24, no. 2-3 (2011): 190-206.

- 15. Rutherdale, Myra. Women and the white man's God: Gender and race in the Canadian mission field. UBC Press, 2014. ACCT 621: Total Marks: 100 Instructions: 1.) The exam will be a take-home exam and is considered open book. 2.) You may not share any ideas or answers with other students under ANY circumstances. 3.) The exam is 2 hours long and must be returned by email to your instructor no later than 2 hours after it is received. Question 1: Please refer to the financial statements provided in Appendix 1: a.) For each of the following, please provide a calculation of the appropriate ratio amount for 2017 and 2018 years. Show your calculations (22 Marks). See Notes to specific financial statement items in calculations. b.) Please provide commentary to your observations, and your assessment of how the change in year-over-year ratios is reflective of the financial performance and health of the company (22 Marks). c.) For Current Ratio, Inventory Turnover and Accounts Receivable Turnover, please provide two examples each of things the company can do to improve these ratios (6 Marks). Answers: 1 a. and 1.b Ratio Calculation Commentary

- 16. Gross Profit Rate (Note 2) Profit Margin (Note 1,2) Return on Assets (Note 1) Asset Turnover (Note 2) Debt to Asset Ratio Times Interest Earned (Note 3) Free Cash Flow Current Ratio Inventory Turnover Working Capital Accounts Receivable Turnover

- 17. (Note 4) Note 1: Ignore Income/Loss attributable to non-controlling interests. Note 2: Consider all revenue items to be sales. Note 3: Include all interest expense items to be part of the cost of financing. Note 4: Consider all receivable items to be trade receivables. Answers: 1c.: Ratio Steps to Improve Ratio Current Ratio Inventory Turnover Accounts Receivable Turnover Question 2: You have recently taken over the role of the Chief Financial Officer of GT Gold Chasers Ltd. (“GT Gold”). GT Gold is junior mining company, that is hoping to hit it big with their next mining venture. You work out of the head office that is based out of Vancouver. GT has got a reputation in the industry for being quick to act, and the management team are known for pushing the envelope to get results. There has been a high turnover of people in the last two years, and the current team are mainly new to the job. During your first few weeks on the job, you have noticed a few “oddities” around how things in the office run. A couple of examples of these are as follows: · Your assistant staff accountant, Stella Monibag helps you with

- 18. the preparation of the accounting financial statements for the company. Stella spends her days reconciling the bank accounts of the company on a daily basis, which is great, because you need to know how much cash you have in the company at all times. Once she has reconciled the accounting general ledger to the bank statement, she prepares all the cheques for the new bills that needs to be paid. You have the authority to sign the cheques, but when you are out of the office, Stella is also able to sign these cheques or approve payments on your behalf. Stella keeps the cheque book on her desk so that she doesn’t lose it easily. Once you have approved a payment, Stella will access the company accounting system to enter the transactions in the general ledger. · Recently the company started to pay some larger invoices to vendors that you have never really heard of. One the vendors, SM Consultants Inc. provided printing services, a piece of furniture and six hours of printing consulting. These were not expected costs, but you are new to the office, and you figure that it will probably sort itself out later. 2.a) Please advise provides commentary on any internal control weaknesses that may exist in GT Gold, based on the above information (12 marks). 2.b) Please provide three possible solutions to the internal control weaknesses you have identified above, and how these will help solve the control weakness (6 marks). 2.c) Provide some commentary and two examples regarding things you would try to change in the organization to address internal control risk (hint: refer back to the Fraud Triangle model discussed during class), and how these changes would impact the company (4 marks). Question 3: The following transactions appeared in the accounting records of GT Gold during the year. Stella comes to your office, and wants to understand how we should be entering these into the accounting system for the December 31 year-end. Please summarize these transactions using the metric below (i.e. show

- 19. how the change in Assets, Liabilities or Shareholder Equity should be shown). Show your calculations. 1.) On January 1, GT purchased a mining machine from Japan. The machine cost CAN$1,350,000 and had to be shipped to Vancouver. Once it arrived in Vancouver, there were customs duties of CAN$50,000. The machine and its unassembled components were placed on a train and assembled on site. The cost of the freight was CAN$10,000, and a friendly mechanic named Mitch assembled the machine components once it arrived at its destination in Northern BC. GT paid Mitch $2,000. (3 marks) 2.) One week into the machine operating, a cable snapped, and Mitch had to replace it. Mitch recommended that we get a better cable that can lift more weight. It would make the machine way better Mitch said. The new cable cost $12,000. (3 Marks) 3.) GT employs a double declining method depreciation, assuming a salvage value of 15,000, and 6 year life. Stella wants to know what to book for depreciation for the year. (8 marks) 4.) On March 31 the next year, a competitor firm to GT offered to buy the mining machine for $2,000,000. GT took the offer and sold the machine on the same day. Assume for the purpose of this point only that accumulated depreciation on this asset at the time of sale was $200,000. Stella wants to know how to account for the sale. (8 marks). 5.) GT currently has $2,000,000 in its receivables on its books. Last year Stella booked $100,000 on the AFDA account. This year, you estimate that 3.5% of receivables are uncollectible. Stella wants to know what to book this year (4 marks). 6.) After making the adjustment in point 5, Stella finds out that

- 20. one of the accounts is uncollectible. They owe GT $65,000. Please help Stella with the adjustment (2 marks). Assets Liabilities Shareholder Equity