Download to read offline

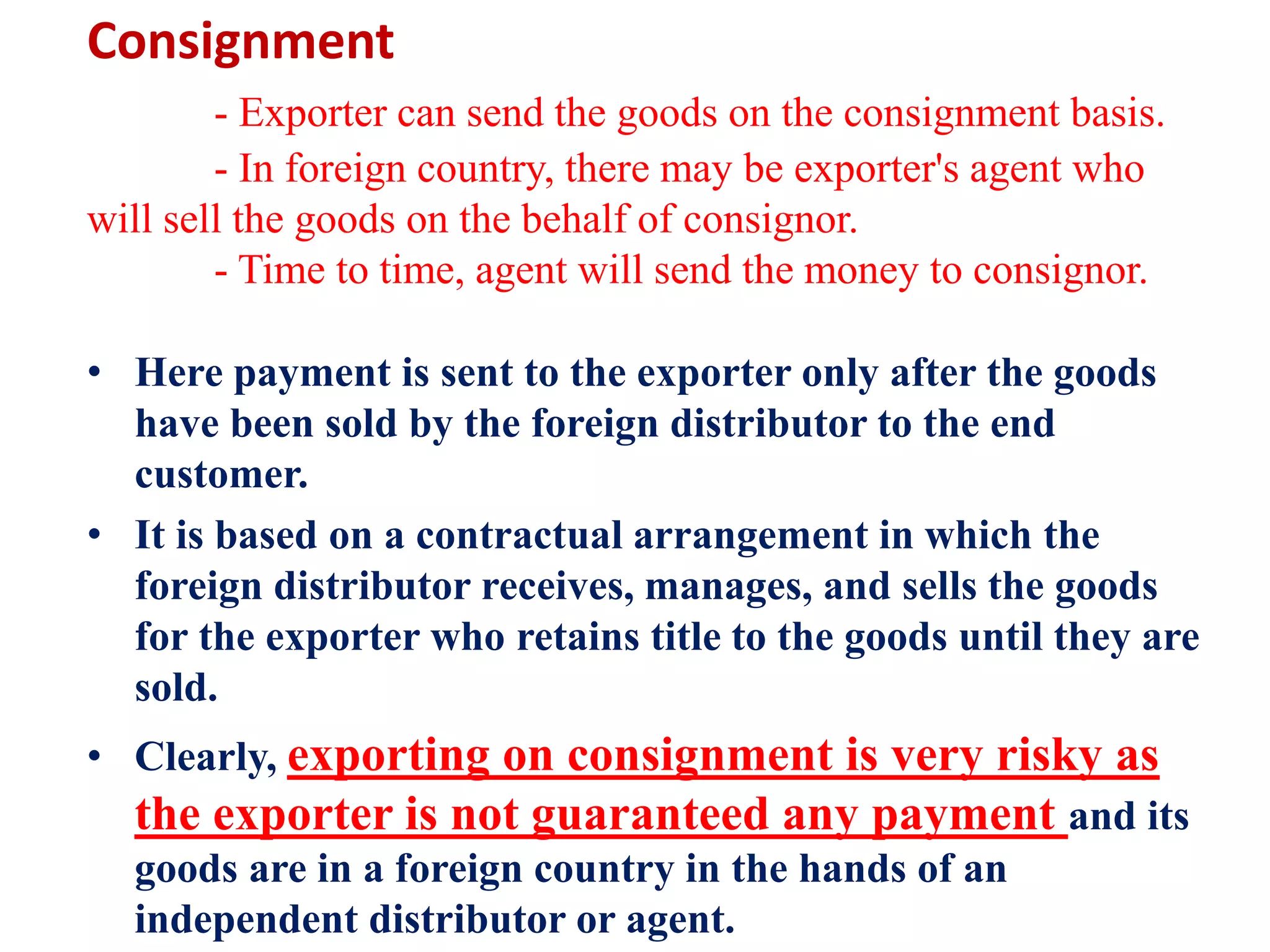

This document discusses various payment methods for foreign market transactions: - Cash in advance requires upfront payment before goods are transferred and is the least attractive option for buyers due to cash flow issues. - Letters of credit provide security as the buyer's bank pays the exporter's bank upon shipment verification, protecting both buyers and sellers. - Documentary collections involve both banks acting as intermediaries, with payment transferred once the exporter provides proof of delivery. - Open accounts allow goods to be shipped and delivered before later payment, benefiting buyers but increasing risk for exporters. - Consignments see goods sent abroad and sold by an agent, with payment only remitted after end customer sales, making this