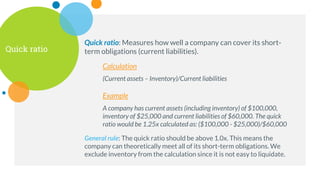

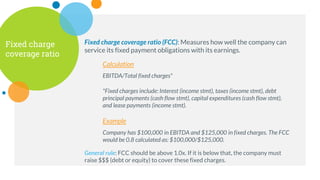

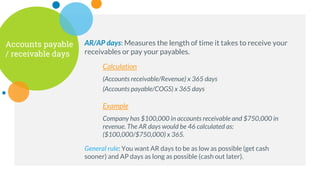

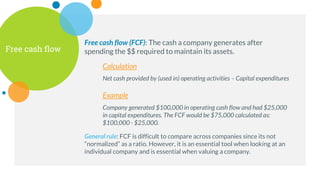

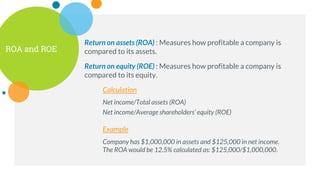

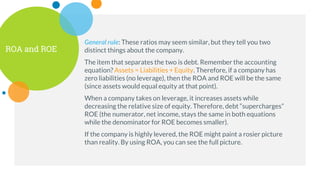

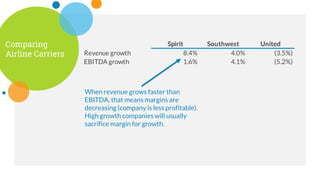

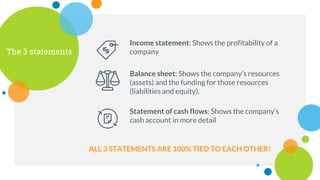

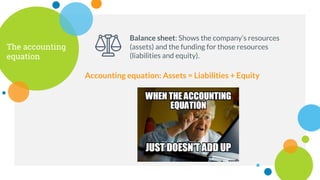

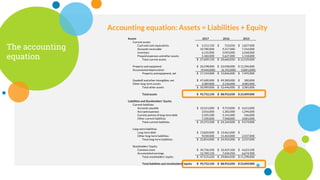

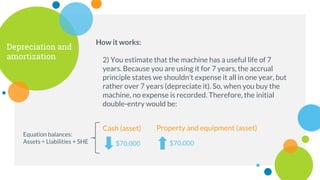

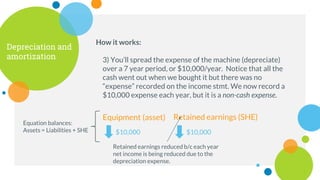

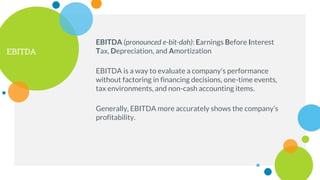

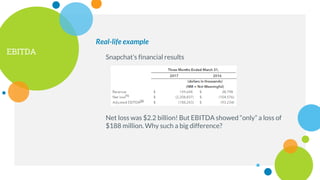

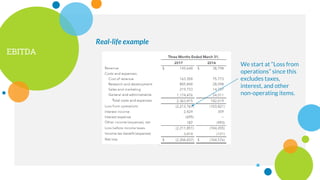

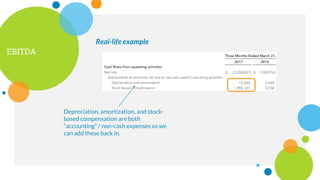

The document provides an overview of financial statement analysis and accounting principles. It explains that the three main financial statements - the income statement, balance sheet, and statement of cash flows - are interconnected and provide important information about a company's performance, financial position, and cash flows. Key accounting concepts discussed include the accounting equation, double-entry bookkeeping, accrual vs cash accounting, depreciation, and the components and uses of each financial statement. Understanding these statements and principles is important for evaluating business decisions.

![Compound

annual growth

rate (CAGR)

CAGR: The average growth rate over a period of time.

Calculation

(

𝐸𝑛𝑑𝑖𝑛𝑔 𝑣𝑎𝑙𝑢𝑒

𝐵𝑒𝑔𝑖𝑛𝑛𝑖𝑛𝑔 𝑣𝑎𝑙𝑢𝑒

)

(

1

#𝑦𝑒𝑎𝑟𝑠

)

− 1

Example

Revenue was $75,000, $100,000, and $125,000 from 2015-2017.

The CAGR would be [($125,000/$75,000)^(1/2)] -1 = 29.1%

Caution: This is not the actual growth rate each year, it is just a

convenient way to “normalize” the growth rate to one number.](https://image.slidesharecdn.com/financial-stmt-analysis-bootcamp-slides-220331132257/85/Financial-Stmt-Analysis-Bootcamp-Slides-pdf-50-320.jpg)