Download to read offline

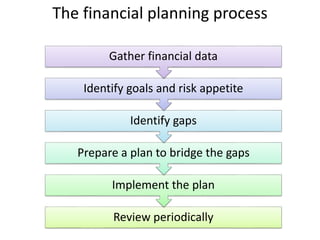

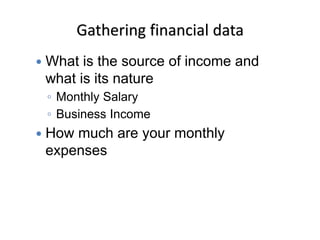

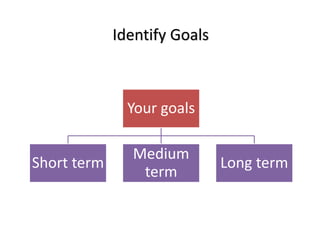

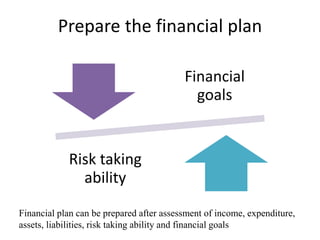

This document provides an overview of financial planning for executives. It discusses the need for financial education due to complex financial products and deteriorating personal finances. The document outlines an agenda for financial planning topics including goals, risk vs return, compounding, inflation, savings vs investments, and various financial products. It defines financial planning as a process to help investors reach their desired financial position. Key aspects of the planning process include identifying goals, income/expenses, gaps, and preparing a plan to bridge gaps.