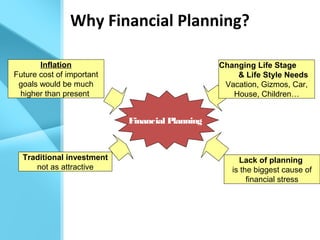

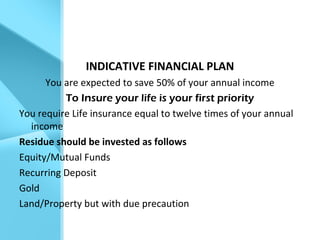

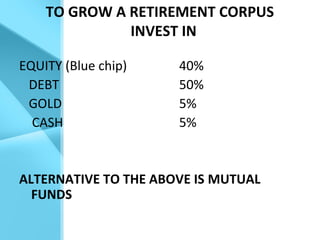

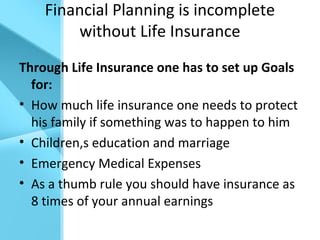

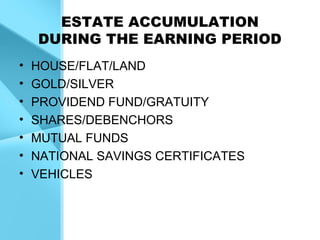

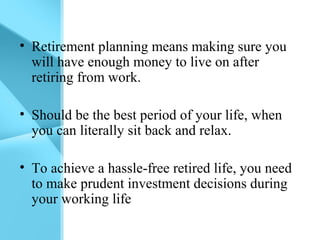

This document provides information about financial planning for retirement. It discusses the importance of saving 10-50% of annual income and investing savings in a diversified portfolio of equity, debt, gold and cash. Life insurance is also recommended to protect family. The document notes that financial planning is needed due to inflation, rising costs of goals, and changing life stages. It provides examples of asset accumulation and investing savings to grow a retirement corpus. Overall, the document emphasizes the importance of financial planning and disciplined saving/investing over one's career to ensure sufficient funds for a comfortable retirement.