Download as PDF, PPTX

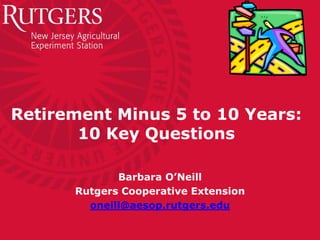

![The “Retirement Grief Cycle”

• Denial: “Not to Worry. This is just a temporary blip and things

will get back to normal soon”

• Anger: “This isn’t fair. They’re taking away [X]”

• Bargaining: “Maybe the union can get an exemption for older

workers so the [change] won’t affect me”

• Depression: “It’s hopeless. I’ll never be able to retire”

• Testing: “If I adjust my spending or work a little longer, I can

probably still retire comfortably”

• Acceptance: “I’ve decided to follow a new financial plan for

retirement”](https://image.slidesharecdn.com/afcpe2011-retirementminus5to10-fixed-tenquestions-04-11-111117195310-phpapp02/85/AFCPE-2011-Retirement-Workshop-10-320.jpg)

This document discusses 10 key questions people should answer about 5-10 years before retirement. It begins with background on the "new normal" challenges of retirement planning in today's economic environment. It then covers estimating life expectancy, calculating needed retirement funds, projecting income and expenses, investing strategies, assessing how long savings will last, choosing a location to live, pursuing hobbies and activities, obtaining health insurance, and developing a retirement plan. Critical retirement planning errors are also outlined.

![2013 sun life_canadian_unretirement_index_report_en[1]](https://cdn.slidesharecdn.com/ss_thumbnails/2013sunlifecanadianunretirementindexreporten1-130611093814-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)