Download to read offline

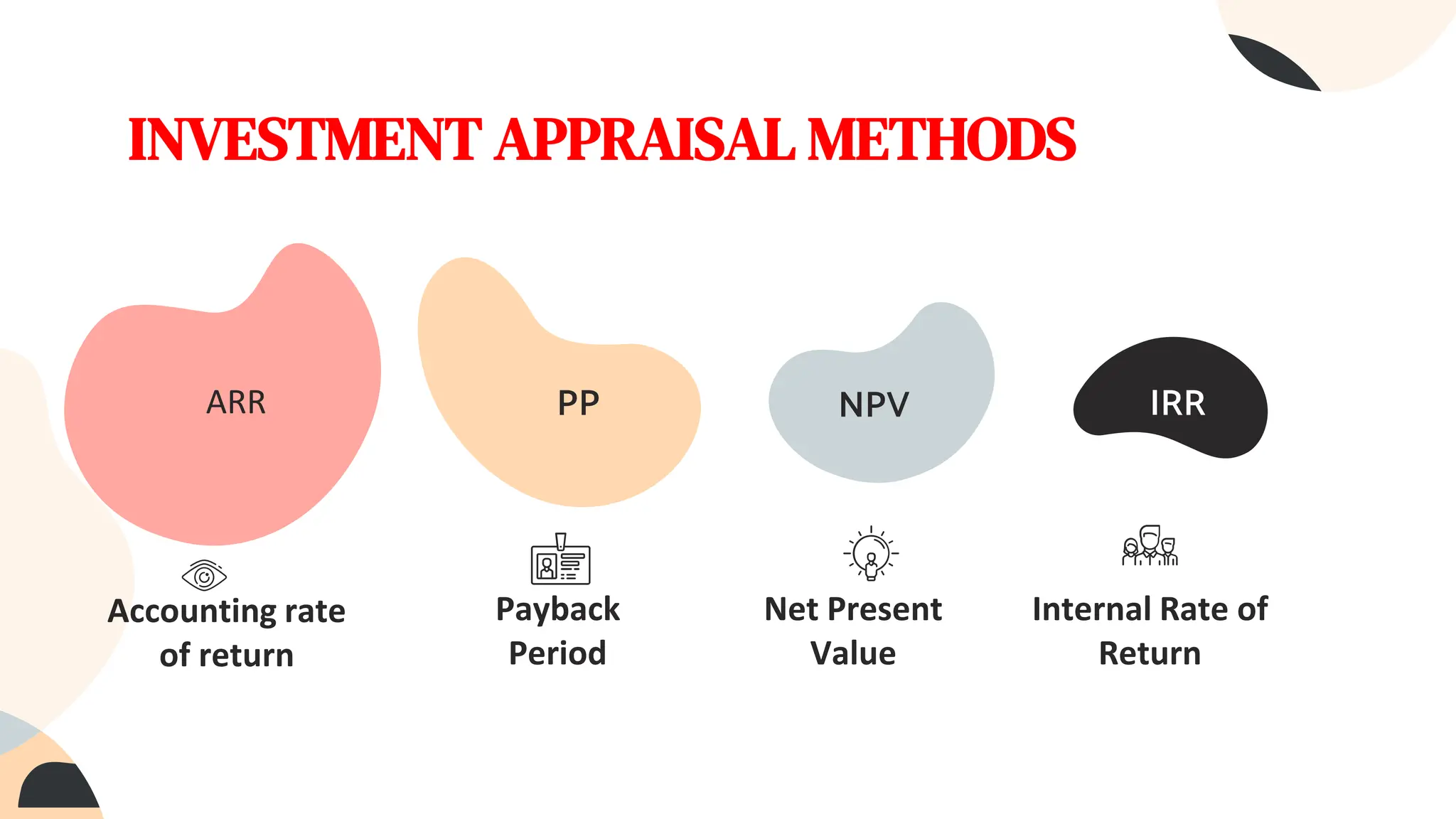

The document discusses capital investment decision making. It provides an overview of four main investment appraisal methods - accounting rate of return, payback period, net present value, and internal rate of return. Each method is examined in terms of its advantages and disadvantages. Surveys of businesses show that net present value and internal rate of return are the most commonly used methods. Strategic planning is also important for identifying profitable investment opportunities that align with a business's strengths and market opportunities. The investment appraisal process involves six key stages from determining available funds to monitoring approved projects.