Download to read offline

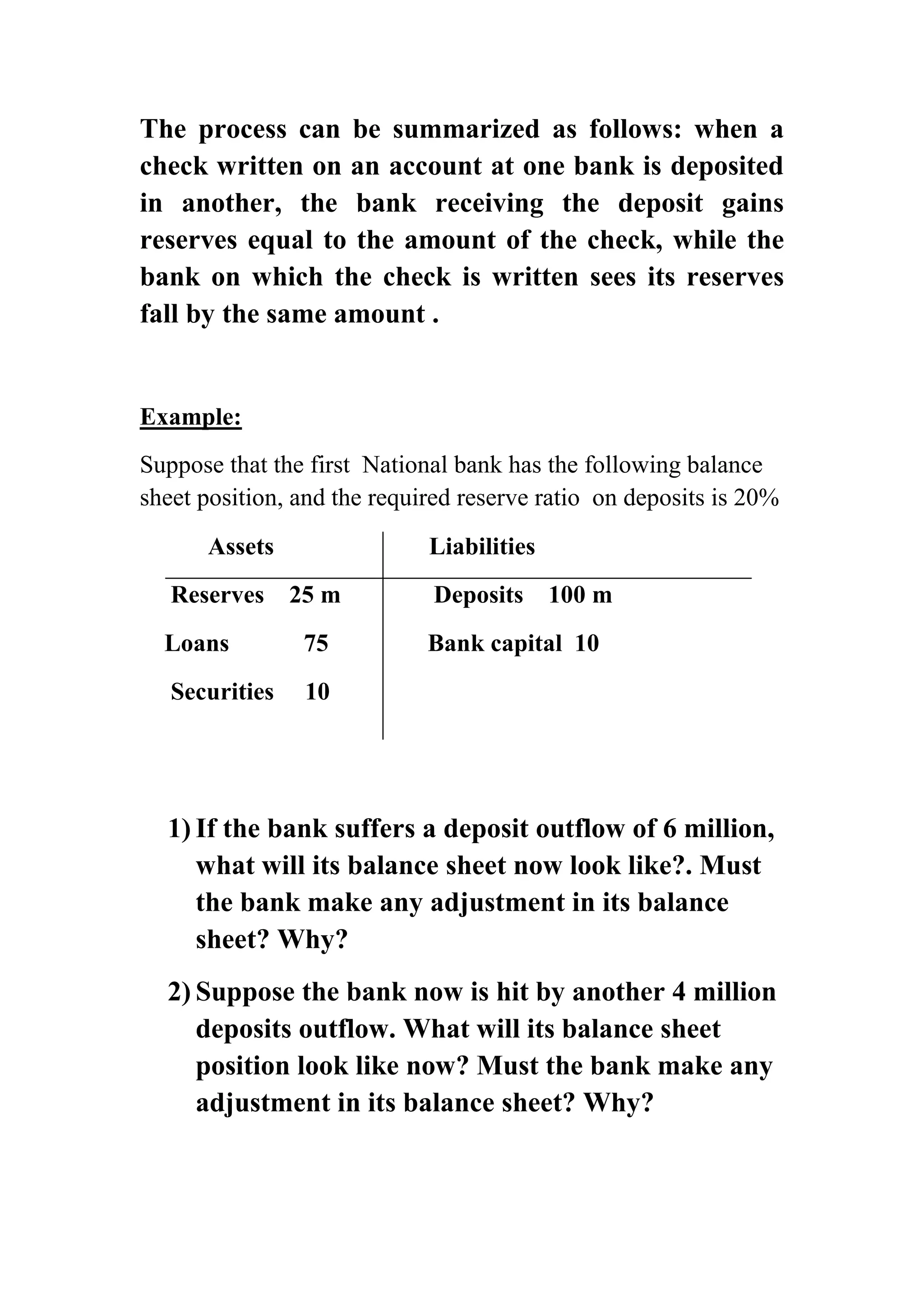

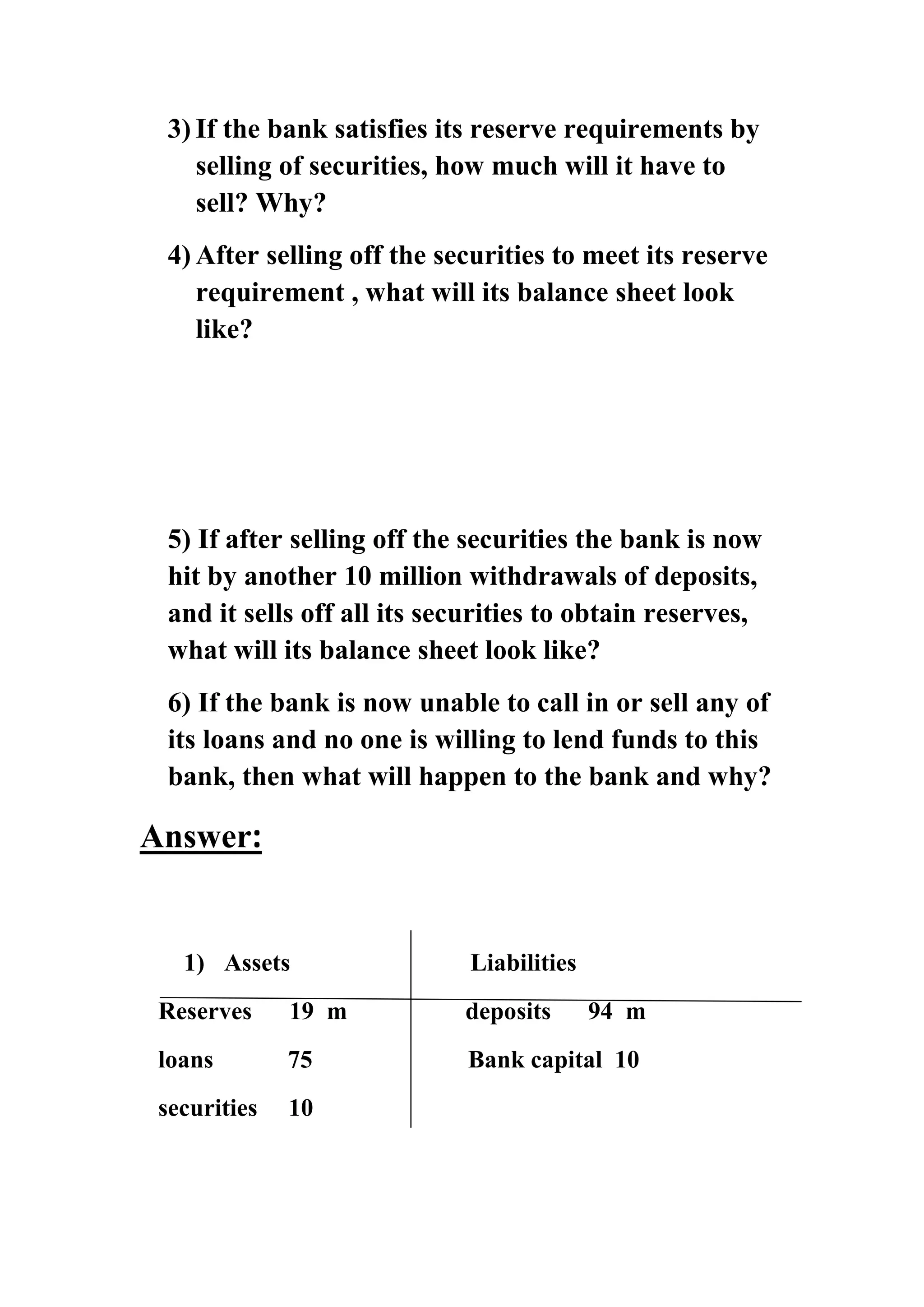

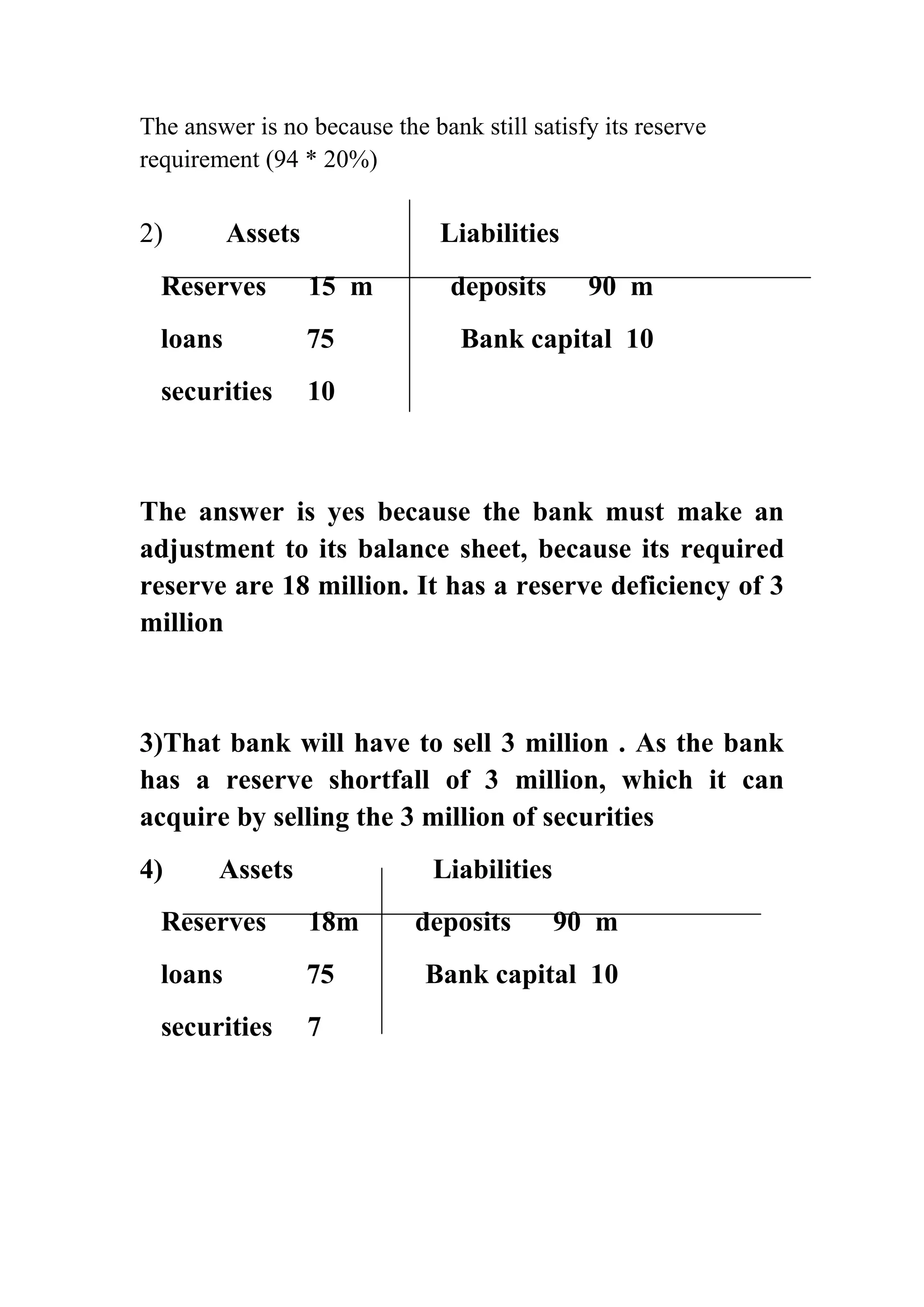

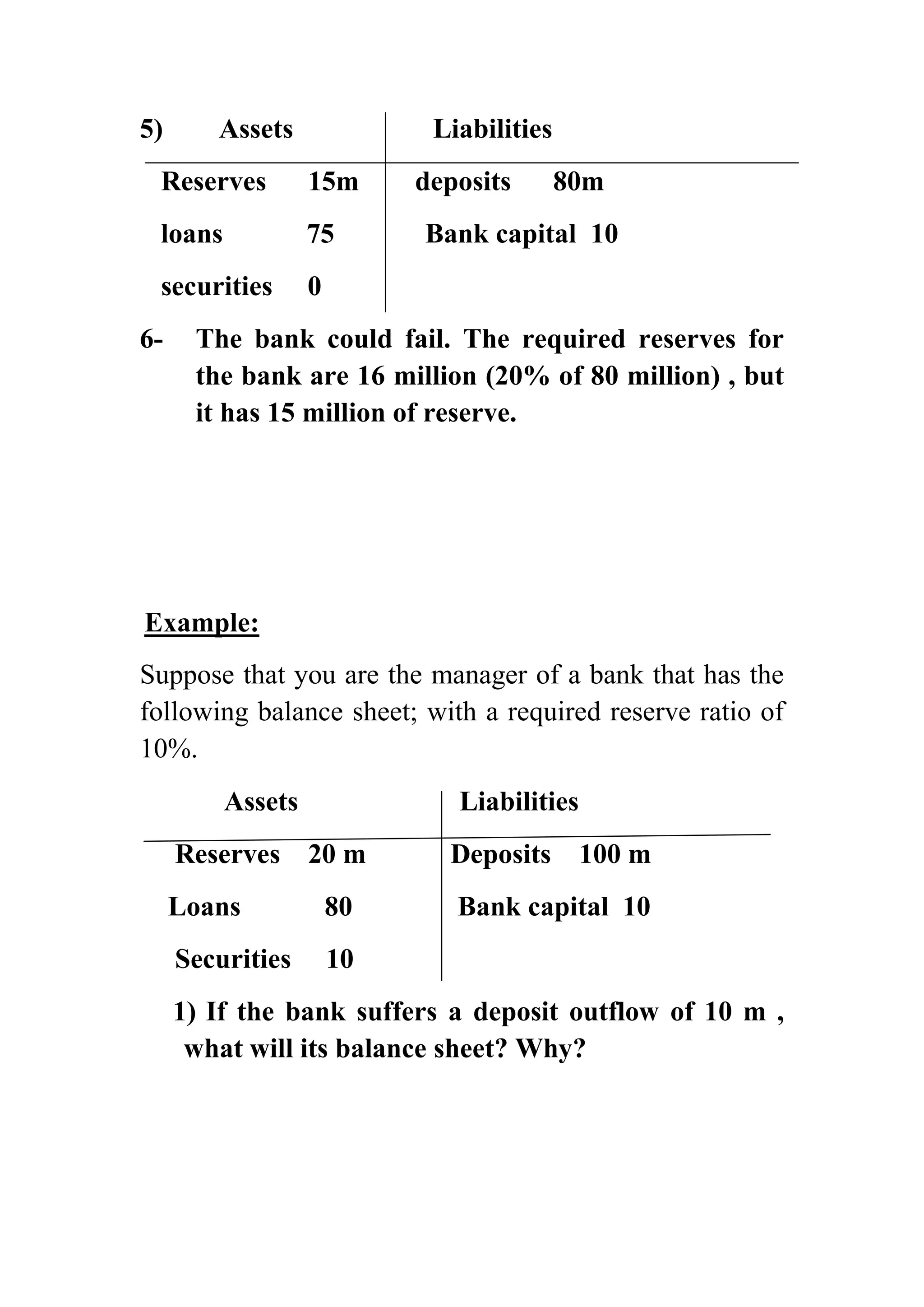

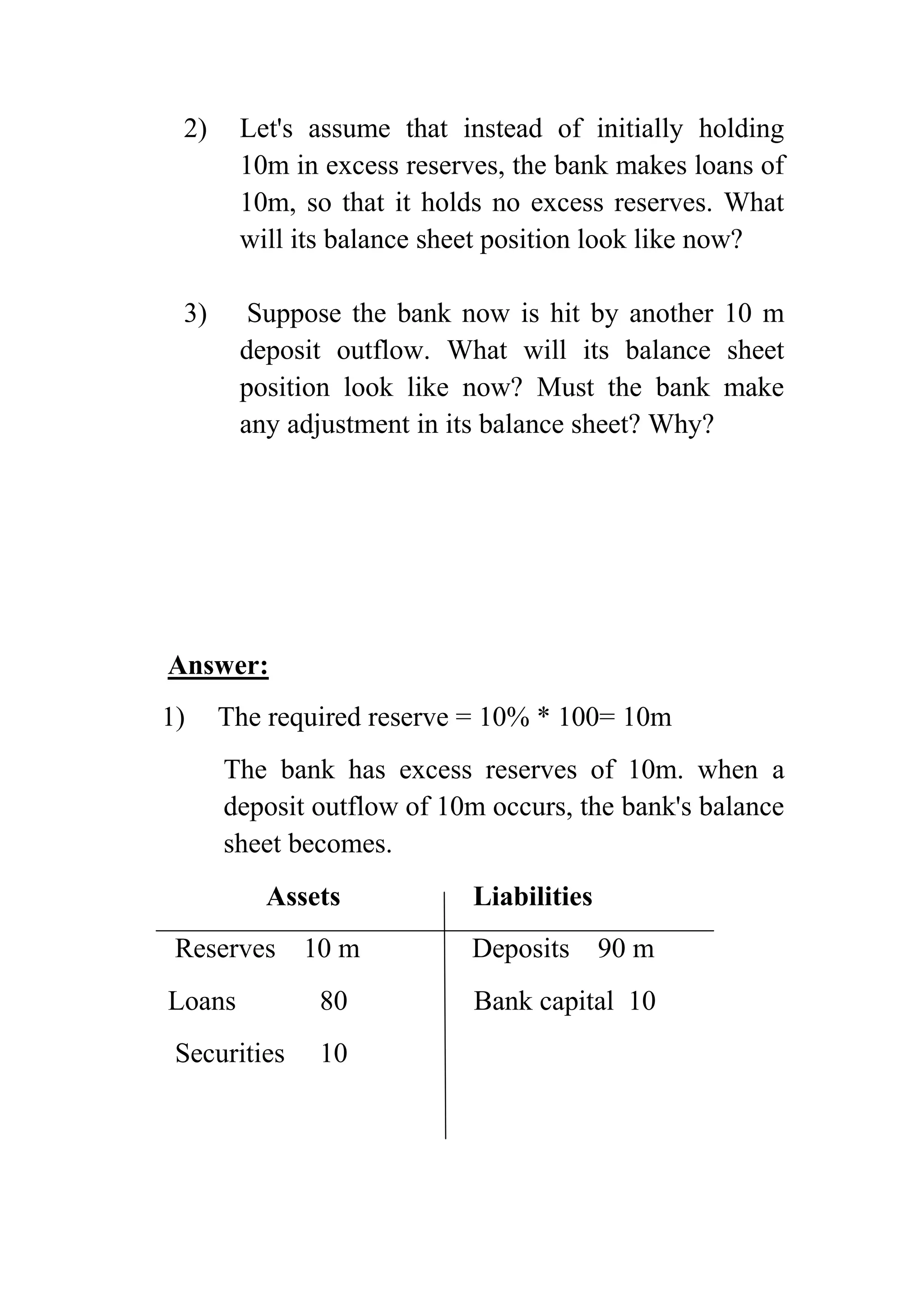

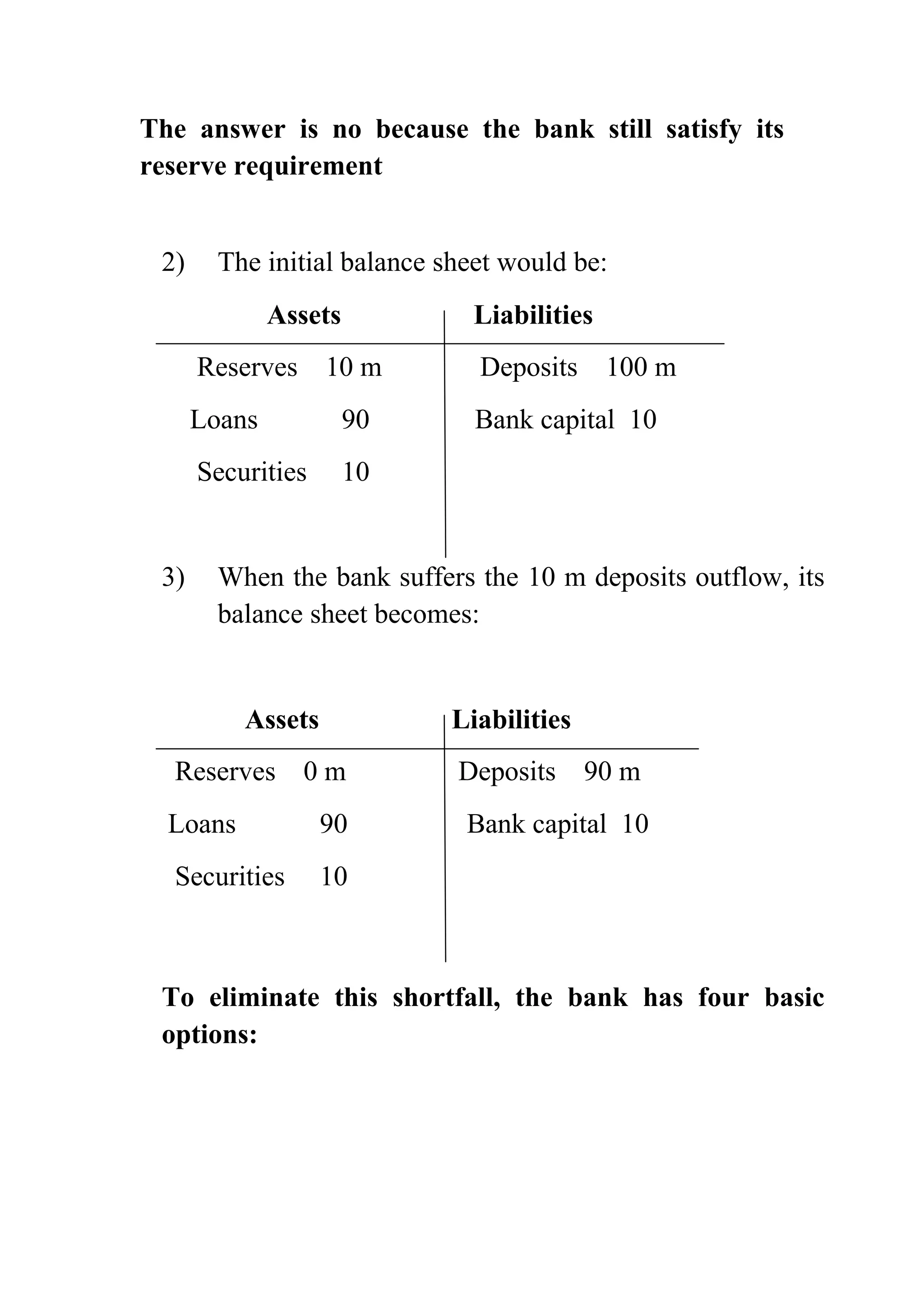

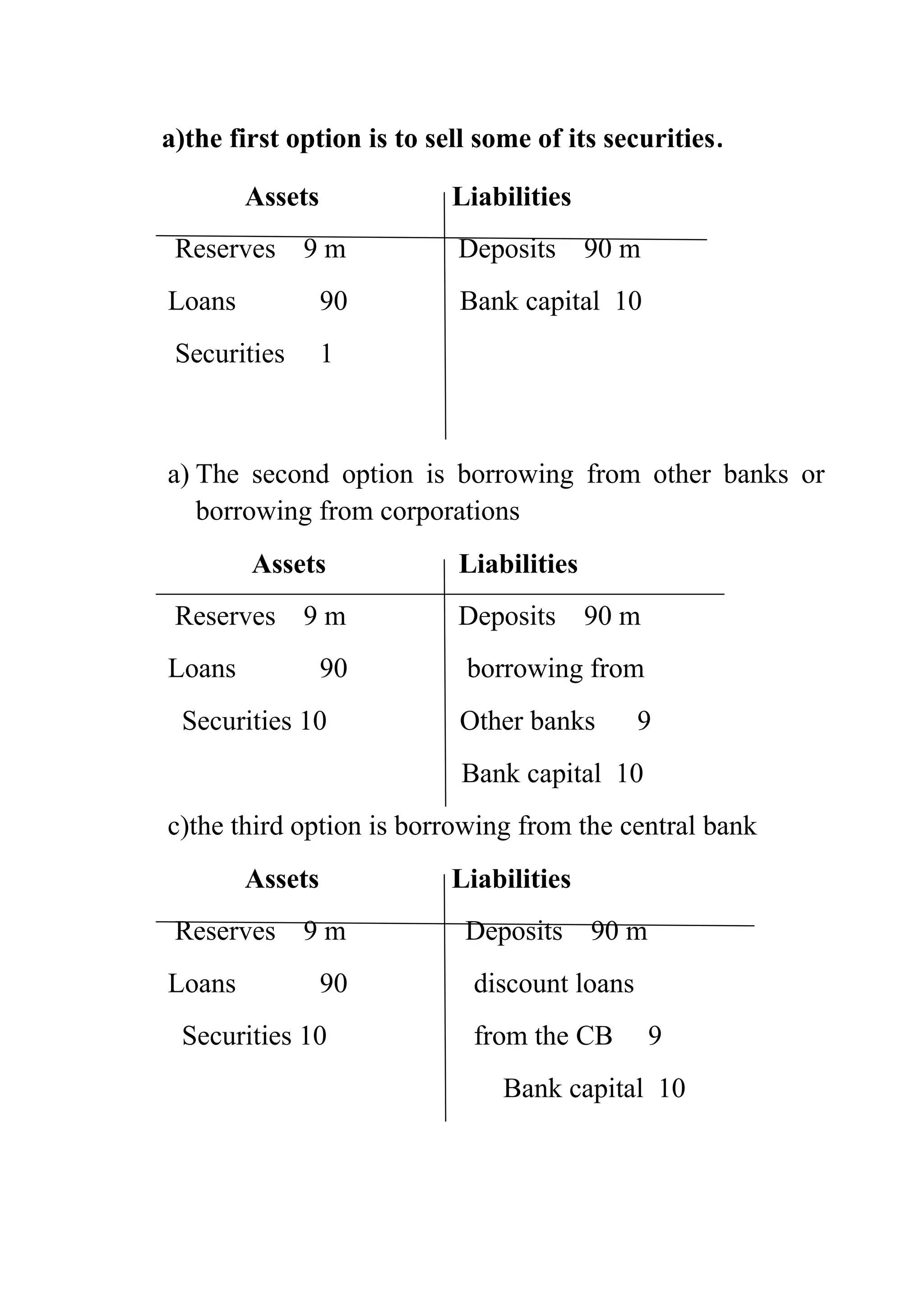

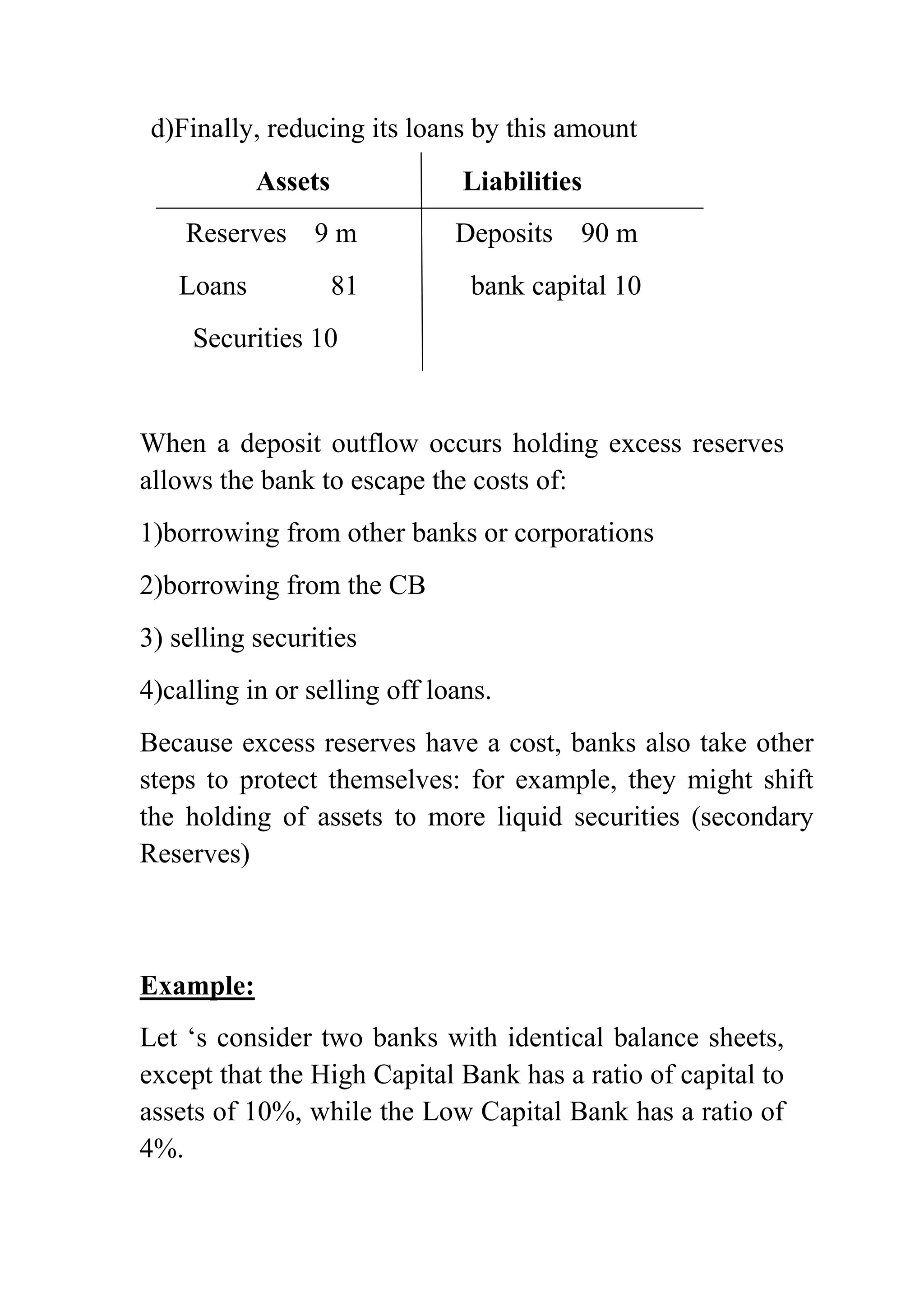

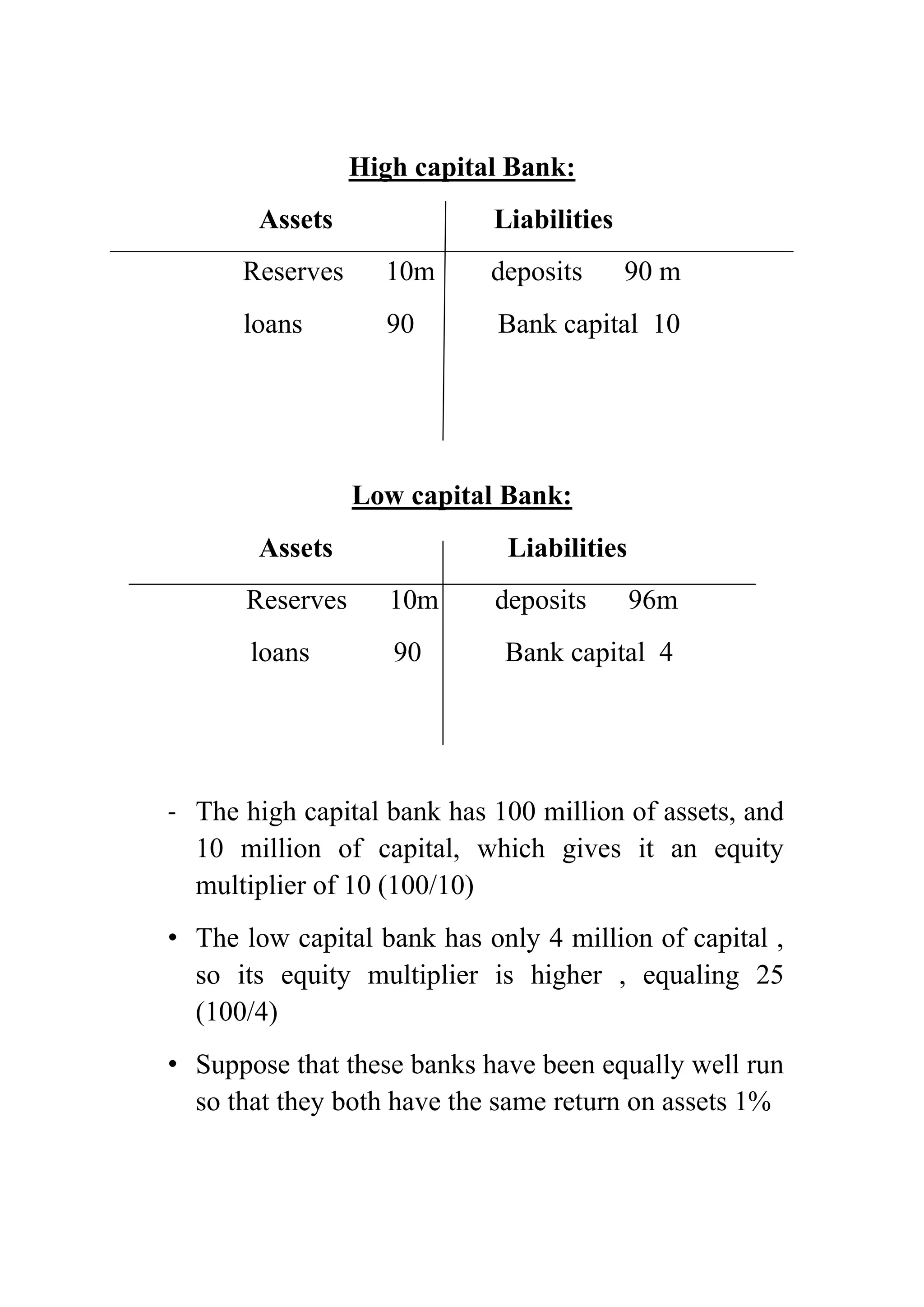

The document defines key terms related to money and banking such as banks, financial markets, monetary theory, inflation, interest rates, and balance sheets. It provides examples to illustrate bank balance sheets and how transactions impact reserves. The central bank plays an essential role as the lender of last resort, implements monetary policy, and controls credit and cash availability. The central bank uses tools like open market operations, reserve requirements, and interest rates to influence the money supply. Money functions as a medium of exchange, store of value, unit of account, and measure of value in an economy.