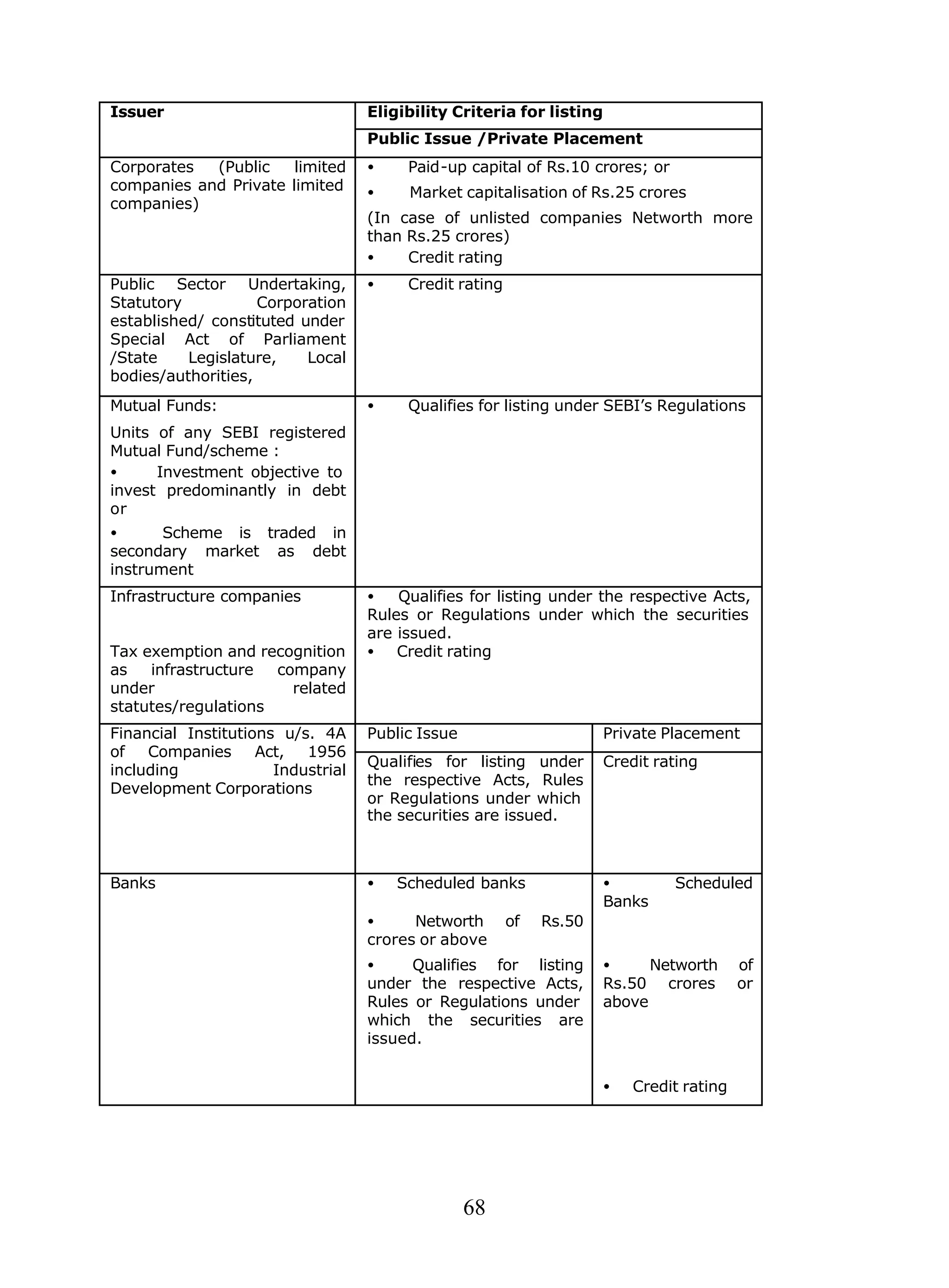

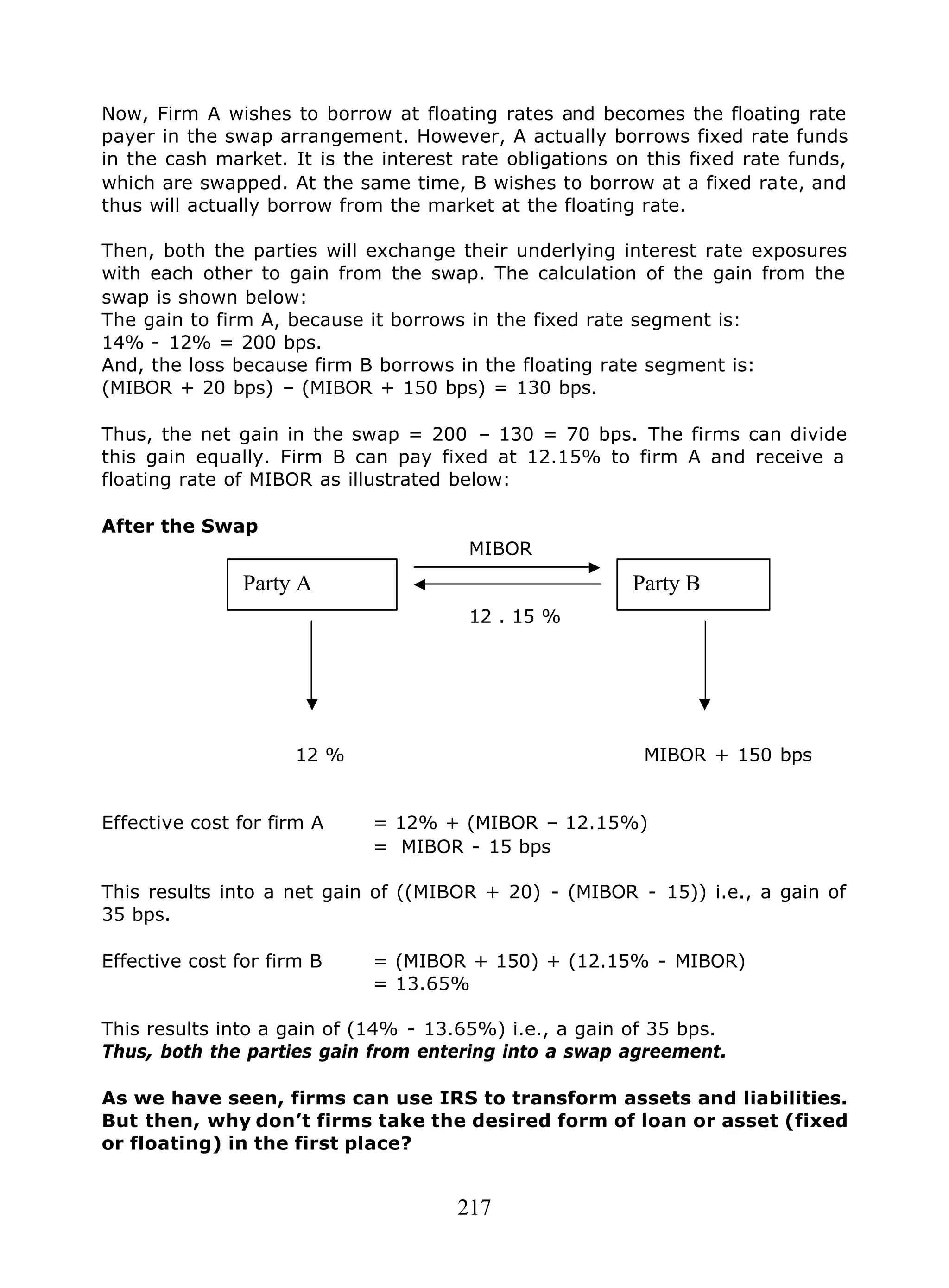

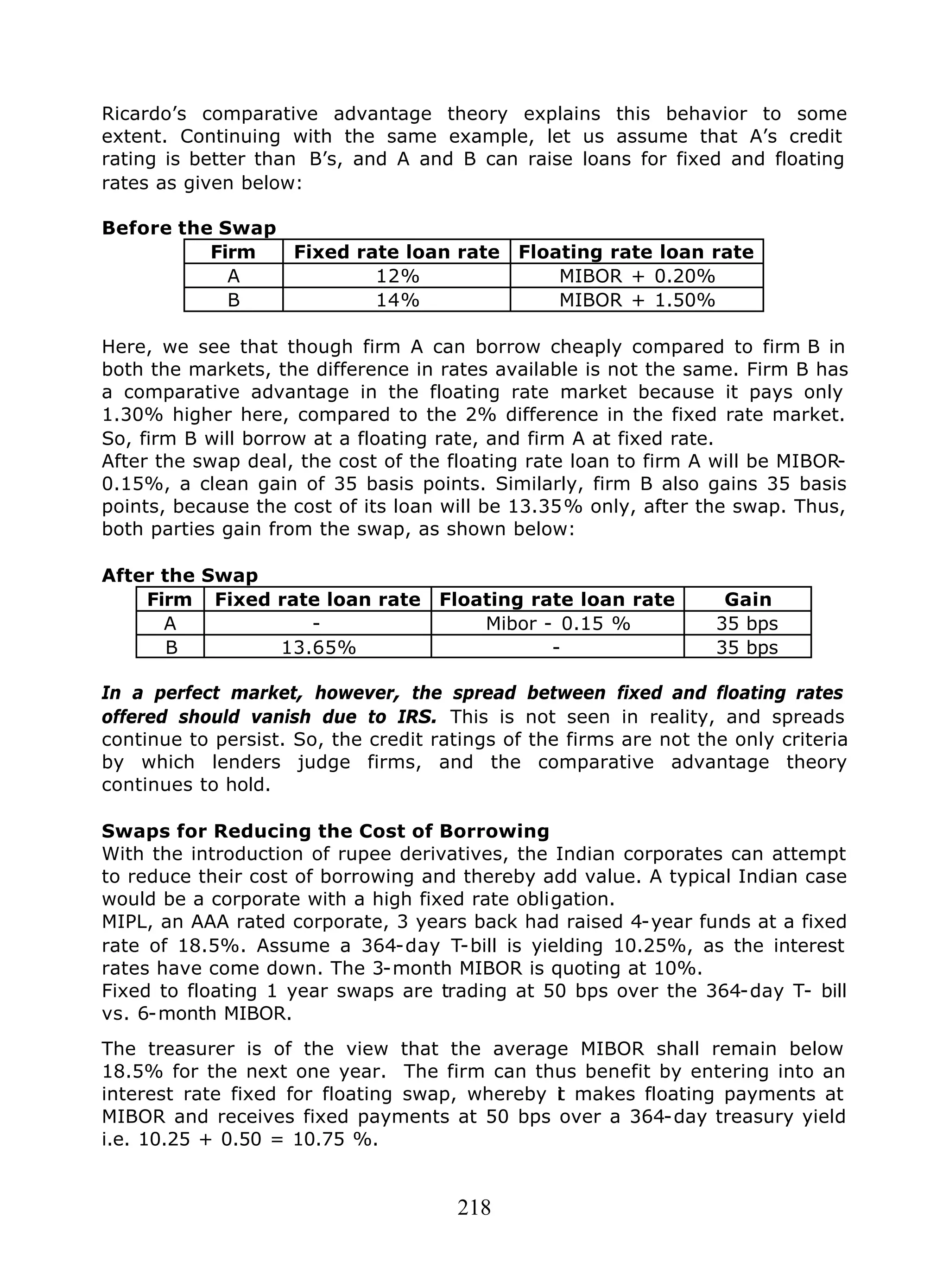

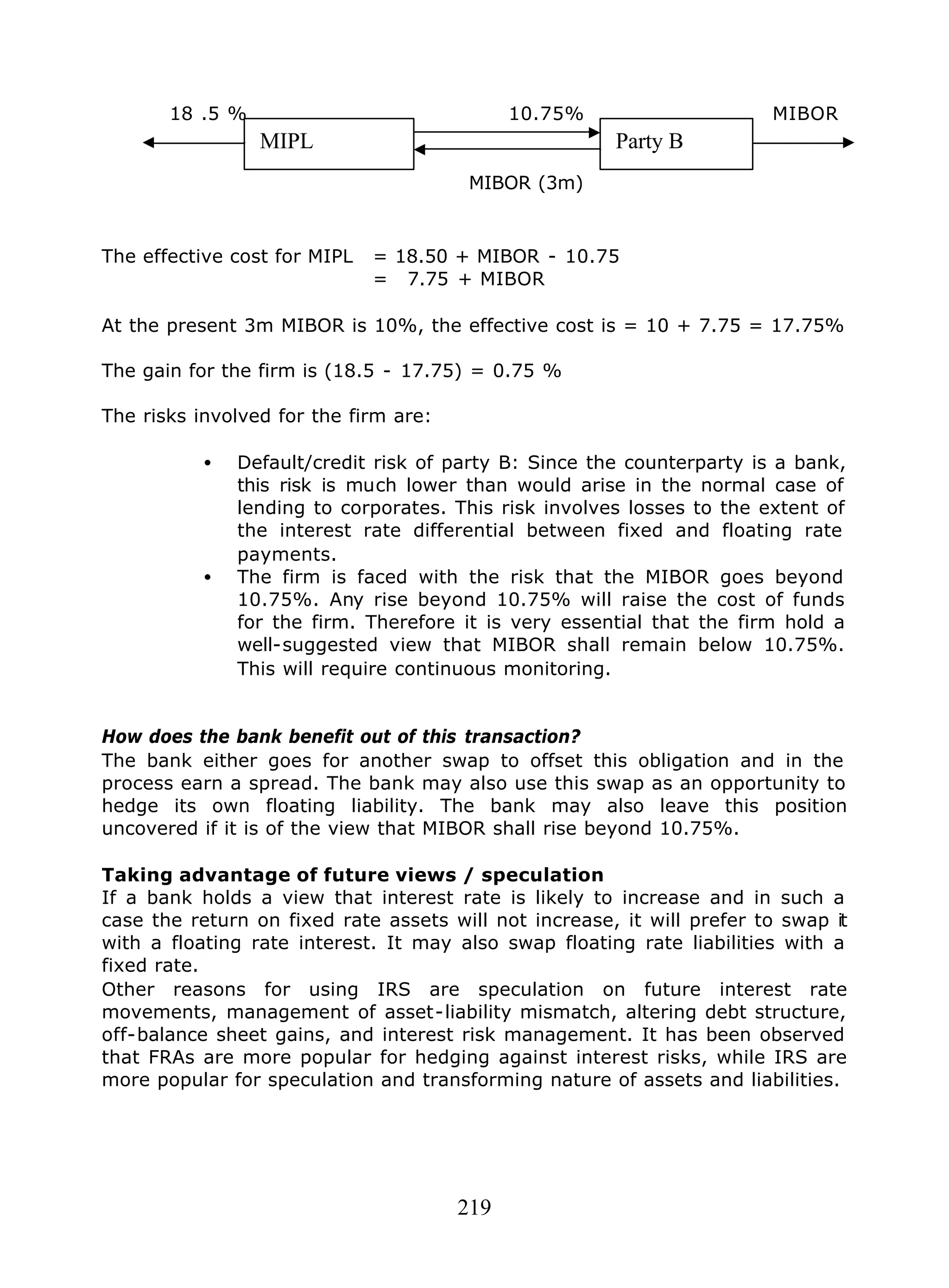

Download to read offline

![35

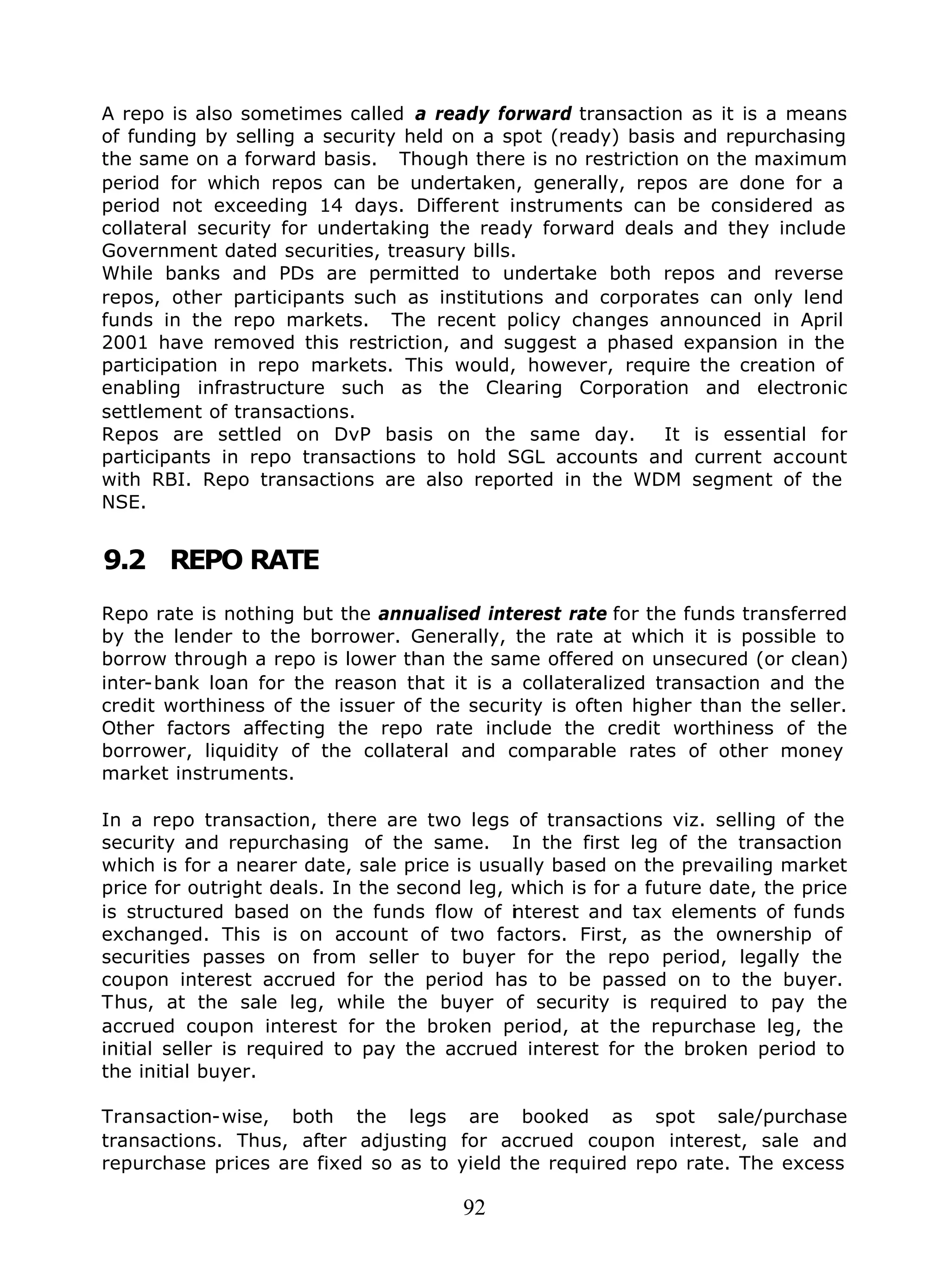

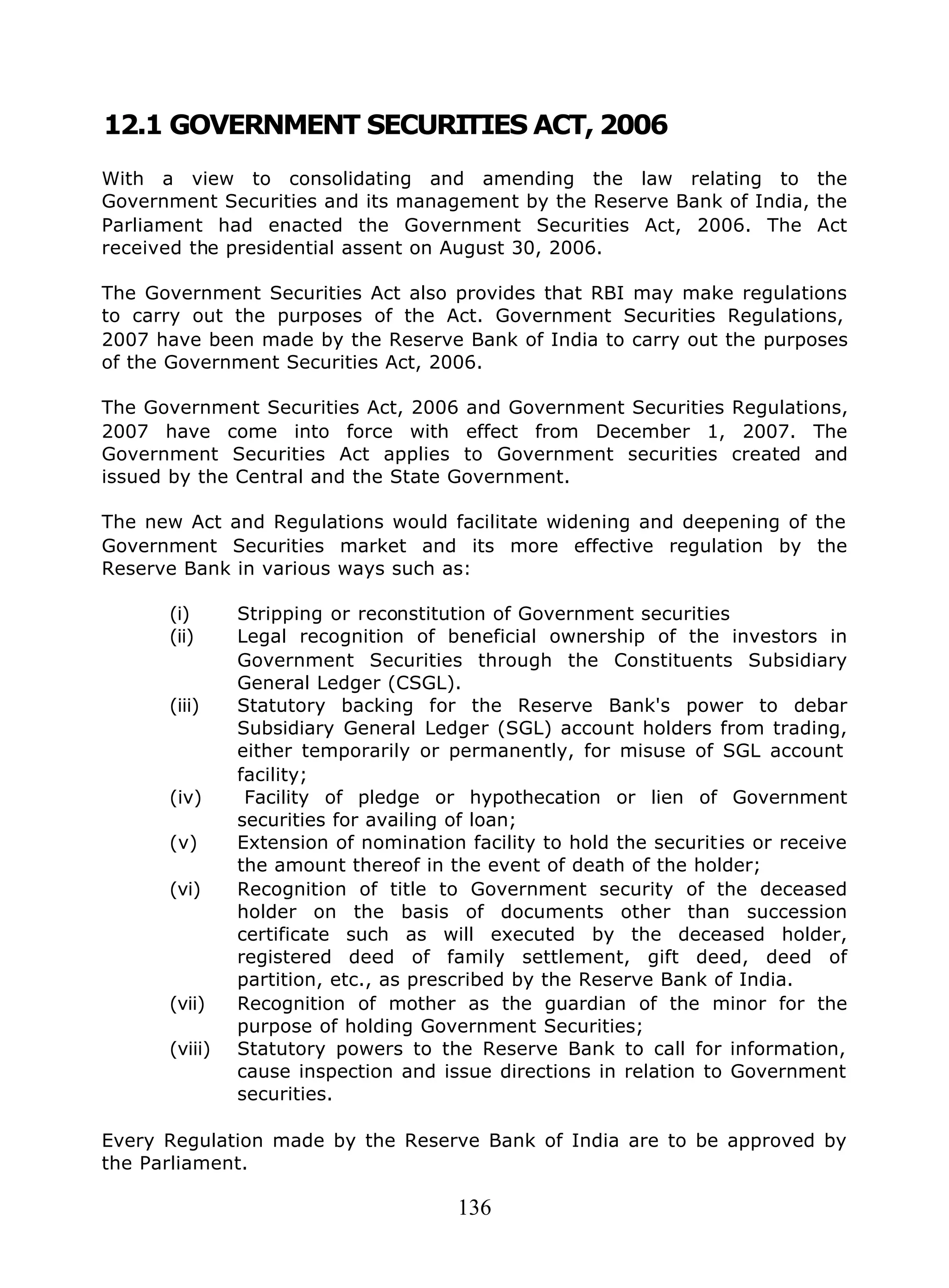

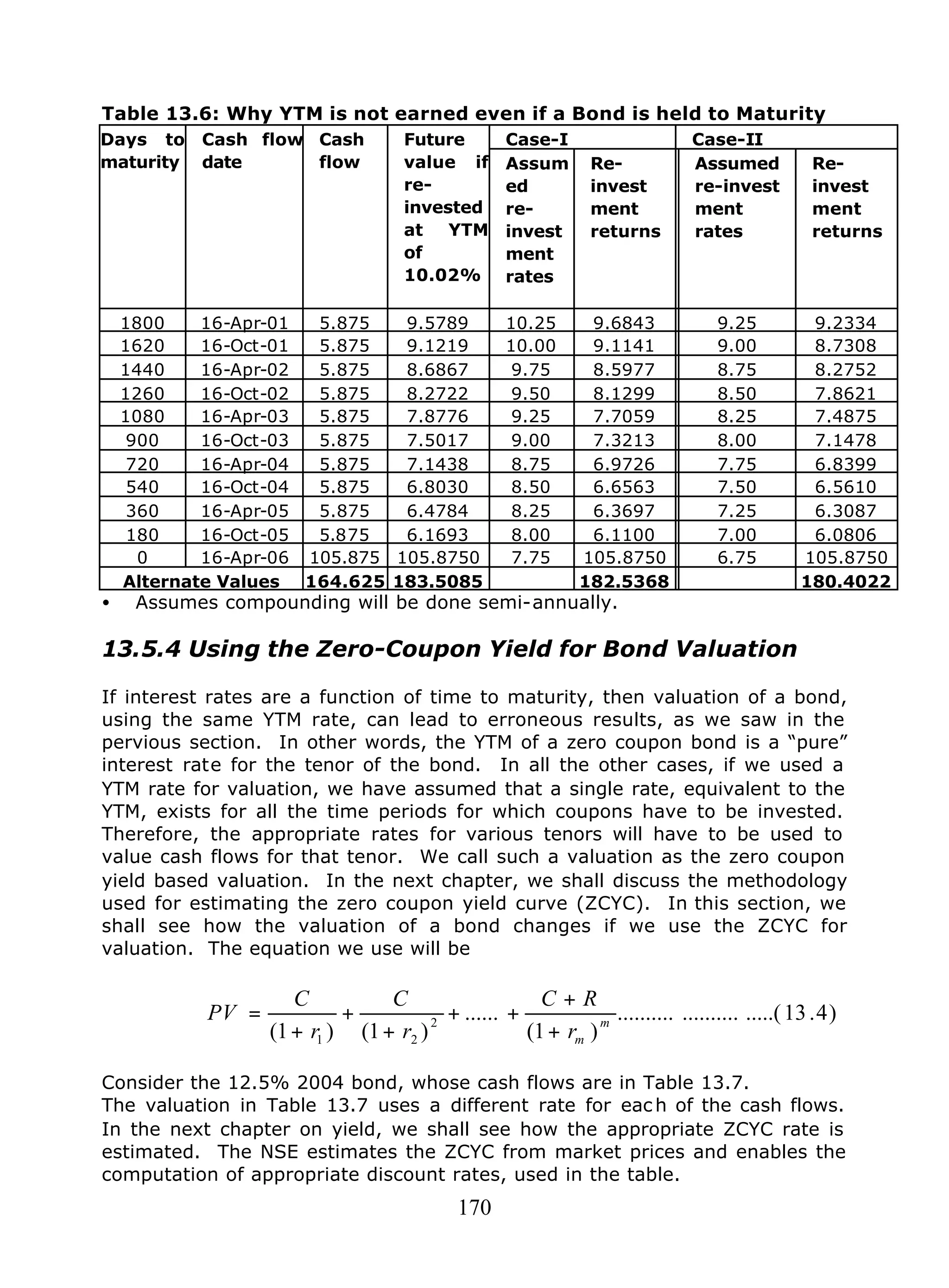

3.5 CONSTITUENT SGL ACCOUNTS

Subsidiary General Ledger (SGL) account is a facility provided by RBI to large

banks and financial institutions to hold their investments in government

securities and treasury bills in the electronic book entry form. Such

institutions can settle their trades for securities held in SGL through a

delivery-versus-payment (DvP) mechanism, which ensures simultaneous

movement of funds and securities. As all investors in government securities

do not have access to the SGL system, RBI has permitted such investors to

open a gilt with any entity authorized by RBI for this purpose and thus avail

of the DvP settlement. RBI has permitted NSCCL, NSDL, CDSL,SHCIL, banks

and PDs to offer constituent SGL account facility to an investor who is

interested in participating in the government securities market.

The facilities offered by the constituent SGL accounts are dematerialisation,

re- materialisation, buying and selling of transactions, corporate actions, and

subscription to primary market issues. All entities regulated by RBI [including

FIs, PDs, cooperative banks, RRBs, local area banks, NBFCs] should

necessarily hold their investments in government securities in either SGL

(with RBI) or CSGL account.

3.6 PRIMARY DEALERS

Primary dealers are important intermediaries in the government securities

markets introduced in 1995. In order to broad base the Primary Dealership

System, banks were permitted to undertake Primary Dealership business

departmentally in 2006-07. There are now 19 primary dealers in the debt

markets. They act as underwriters in the primary debt markets, and as

market makers in the secondary debt markets, apart from enabling the

participation of a number of constituents in the debt markets.

The objectives of setting up the system of primary dealers are 2

:

i. To strengthen the infrastructure in the government securities market in

order to make it vibrant, liquid and broad-based;

ii. To develop underwriting and market making capabilities for government

securities outside the Reserve Bank, so that the Reserve Bank could

gradually shed these functions;

iii. To improve secondary market trading system that would contribute to

price discovery, enhance liquidity and turnover and encourage voluntary

holding of government securities among a wider investor base; and

iv. To make primary dealers an effective conduit for conducting open market

operations.

2

The following sections on primary dealers and satellite dealers have been downloaded from

www.rbi.org.in.](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-36-2048.jpg)

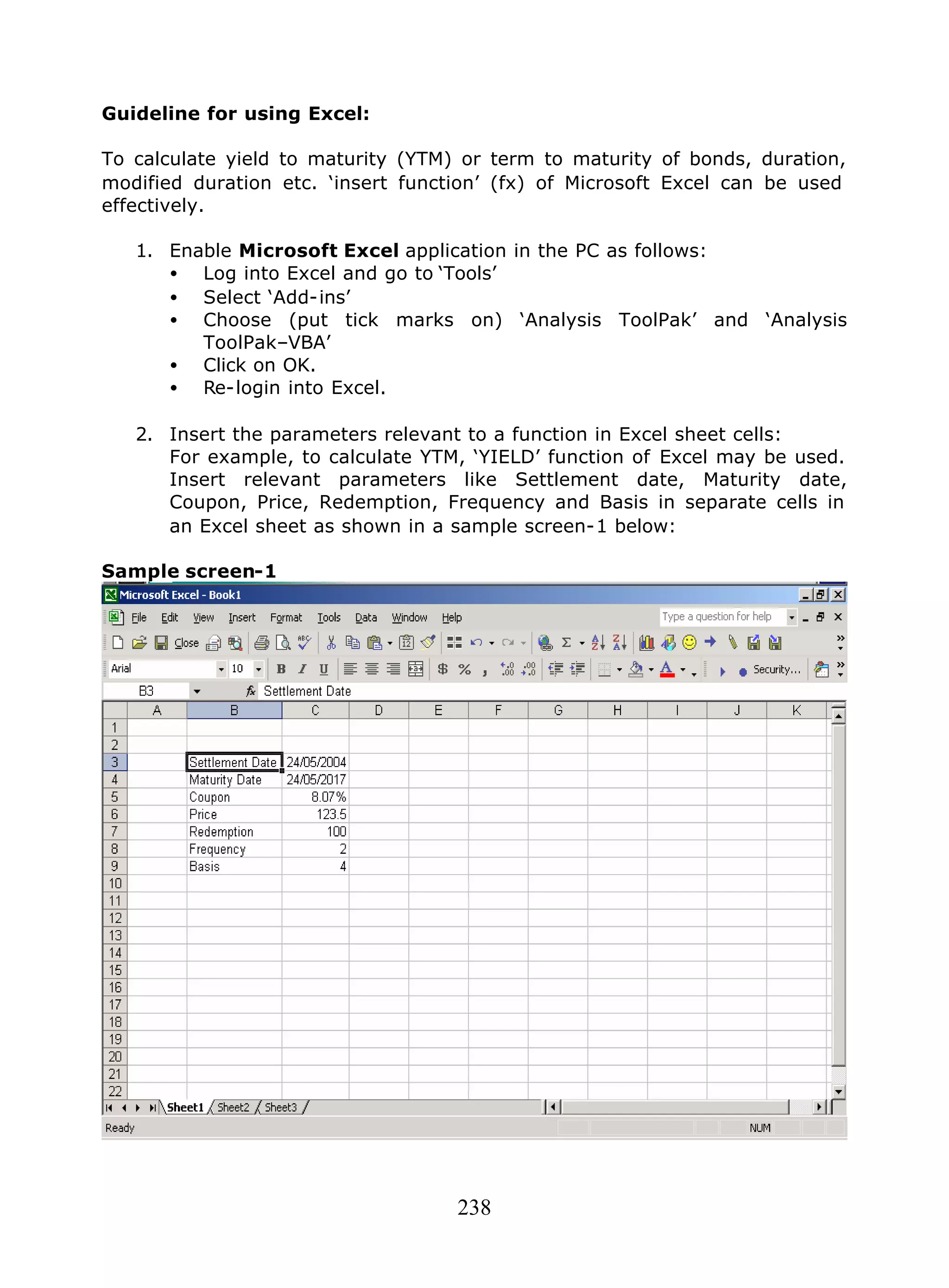

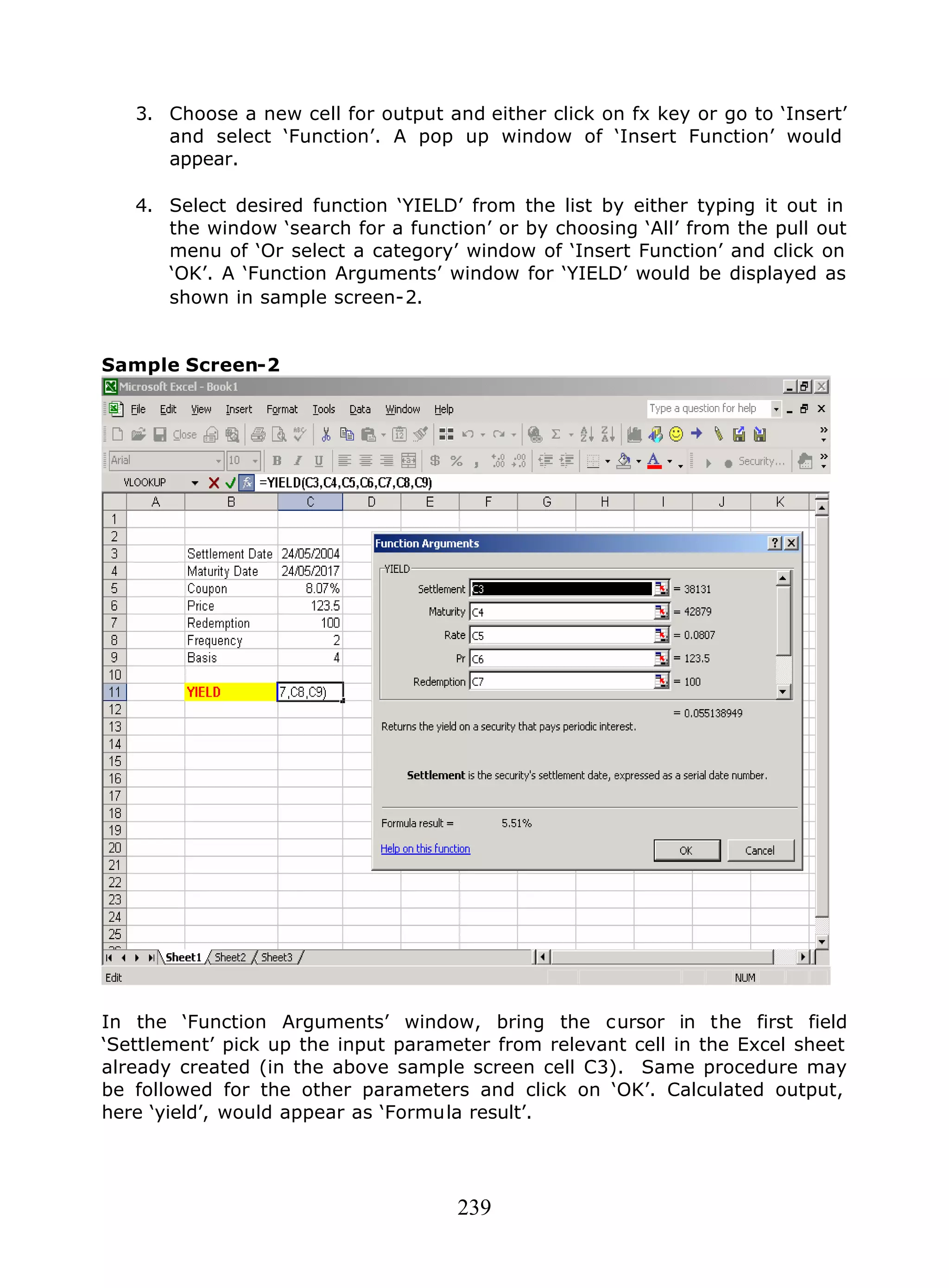

![52

Model Questions

1. A treasury bill maturing on 28-Jun-2002 is trading in the market

on 3-Jul-2001 at a price of Rs. 92.8918. What is the discount rate

inherent in this price?

Answer:

The yield is computed as:

= [(100-price)*365]/ (Price * No of days to maturity)

= [(100-92.8918)*365]/ (92.8918*360) = 7.7584%

2. What is the price at which a treasury bill maturing on 23rd March

2002 would be valued on July 13, 2001 at a yield of 6.8204%?

Answer:

The price can be computed as

= 100/ {1+ [yield% * (No of days to maturity/365)]}

= 100/ {1+ [6.8204 %*( 253/365)]} = Rs. 95.4858

3. What is the day count convention in the treasury bill markets?

a. 30/360

b. Actual/Actual

c. Actual/360

d. Actual/365

Answer: d](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-53-2048.jpg)

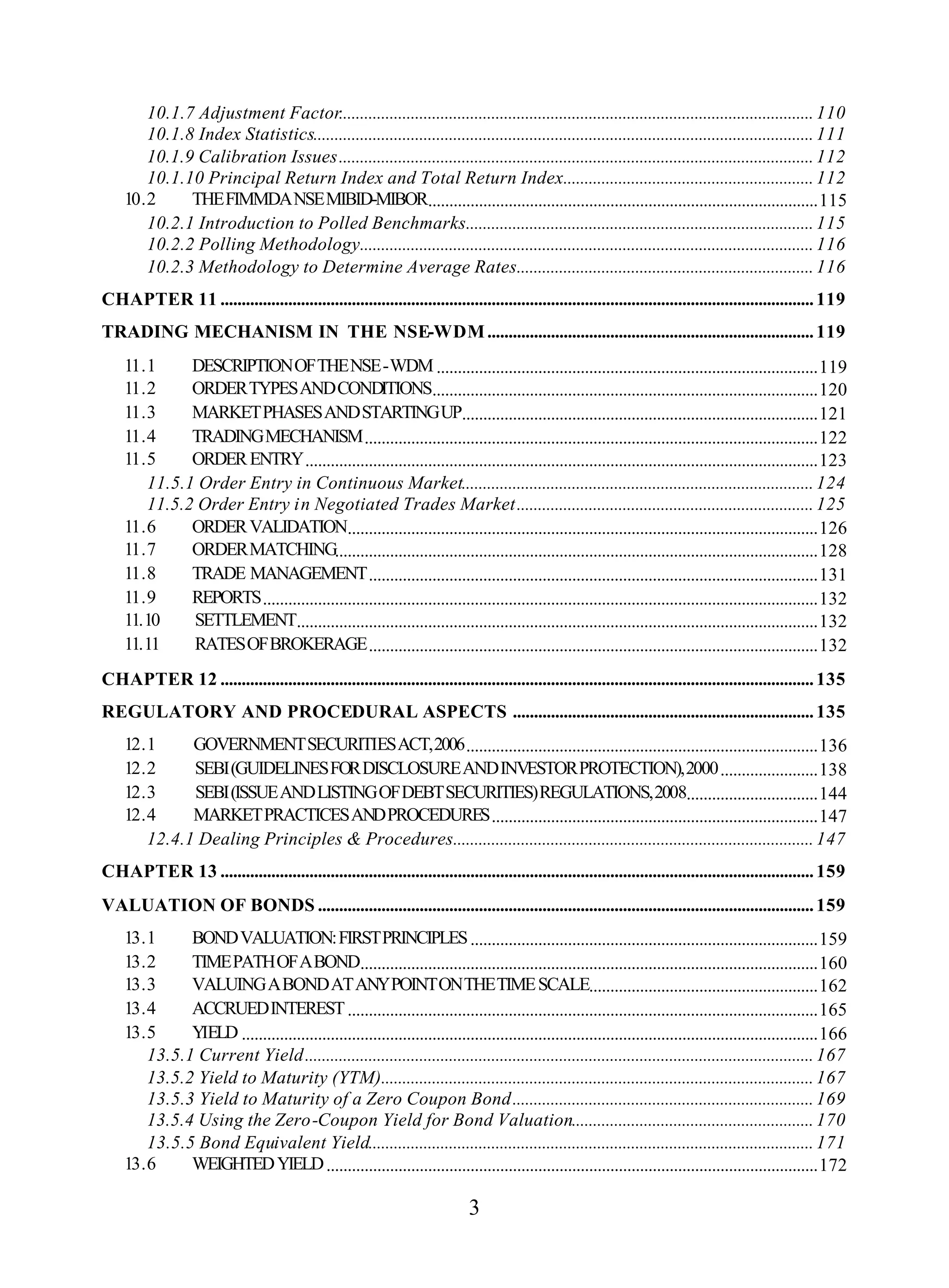

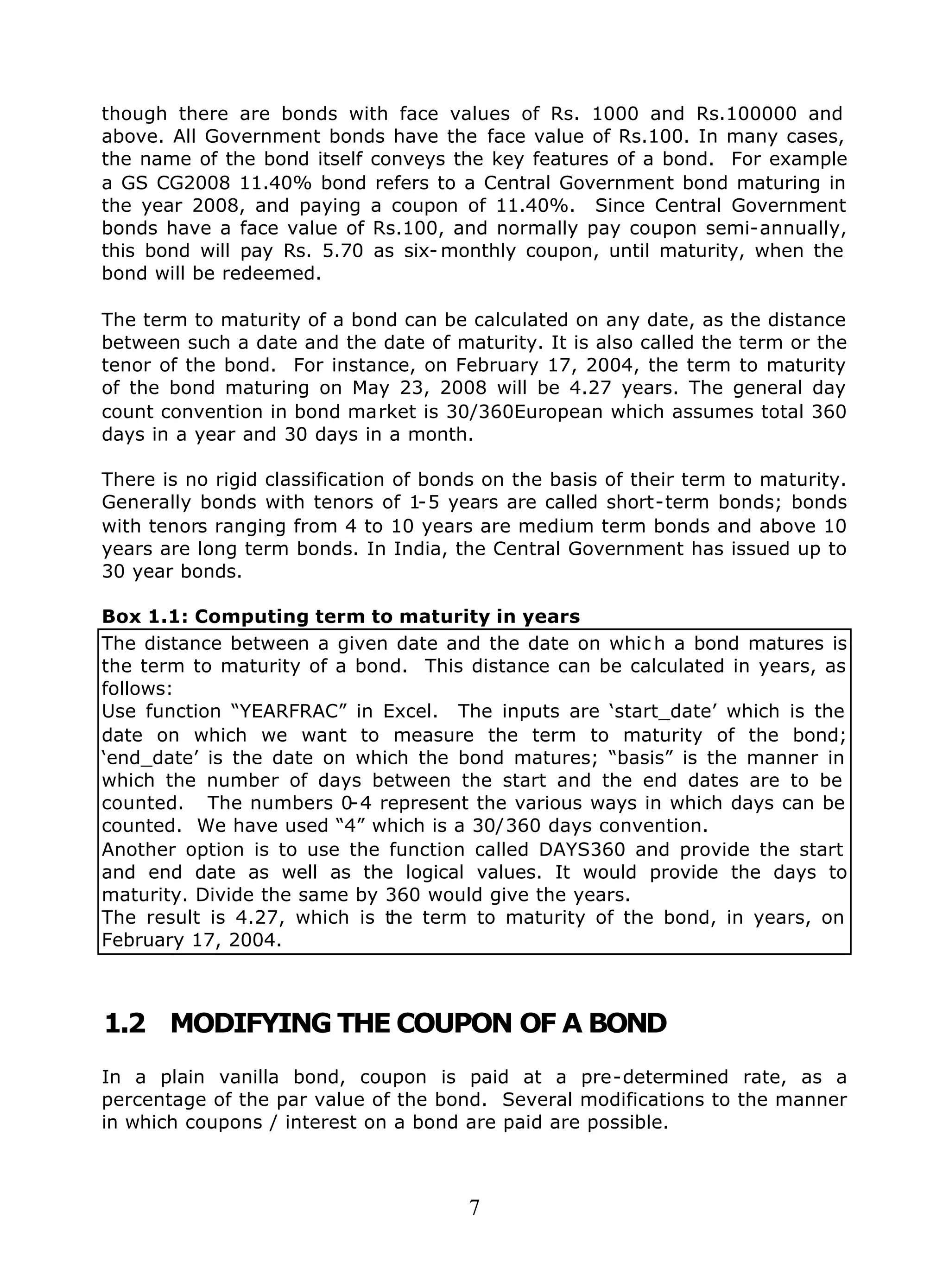

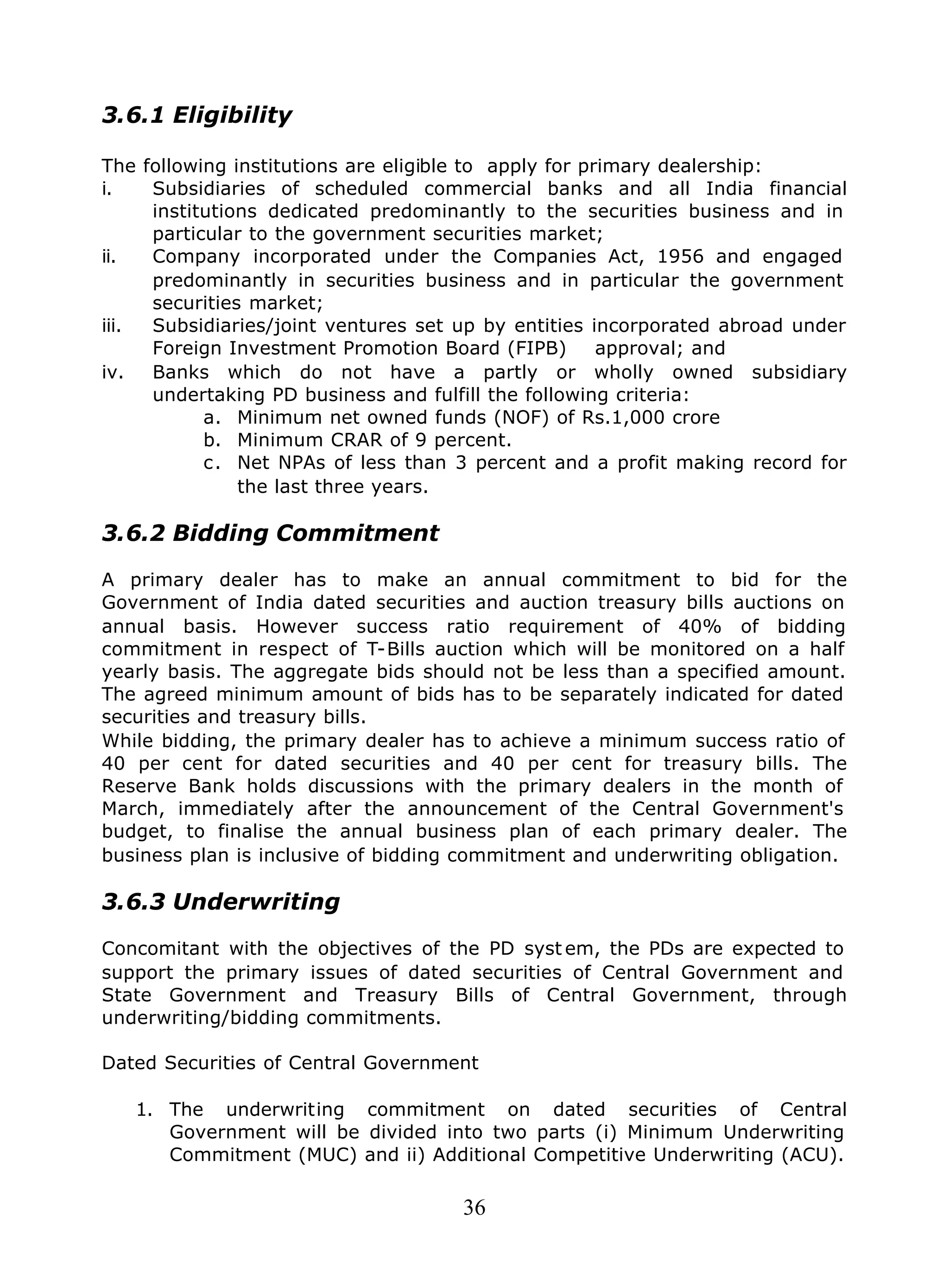

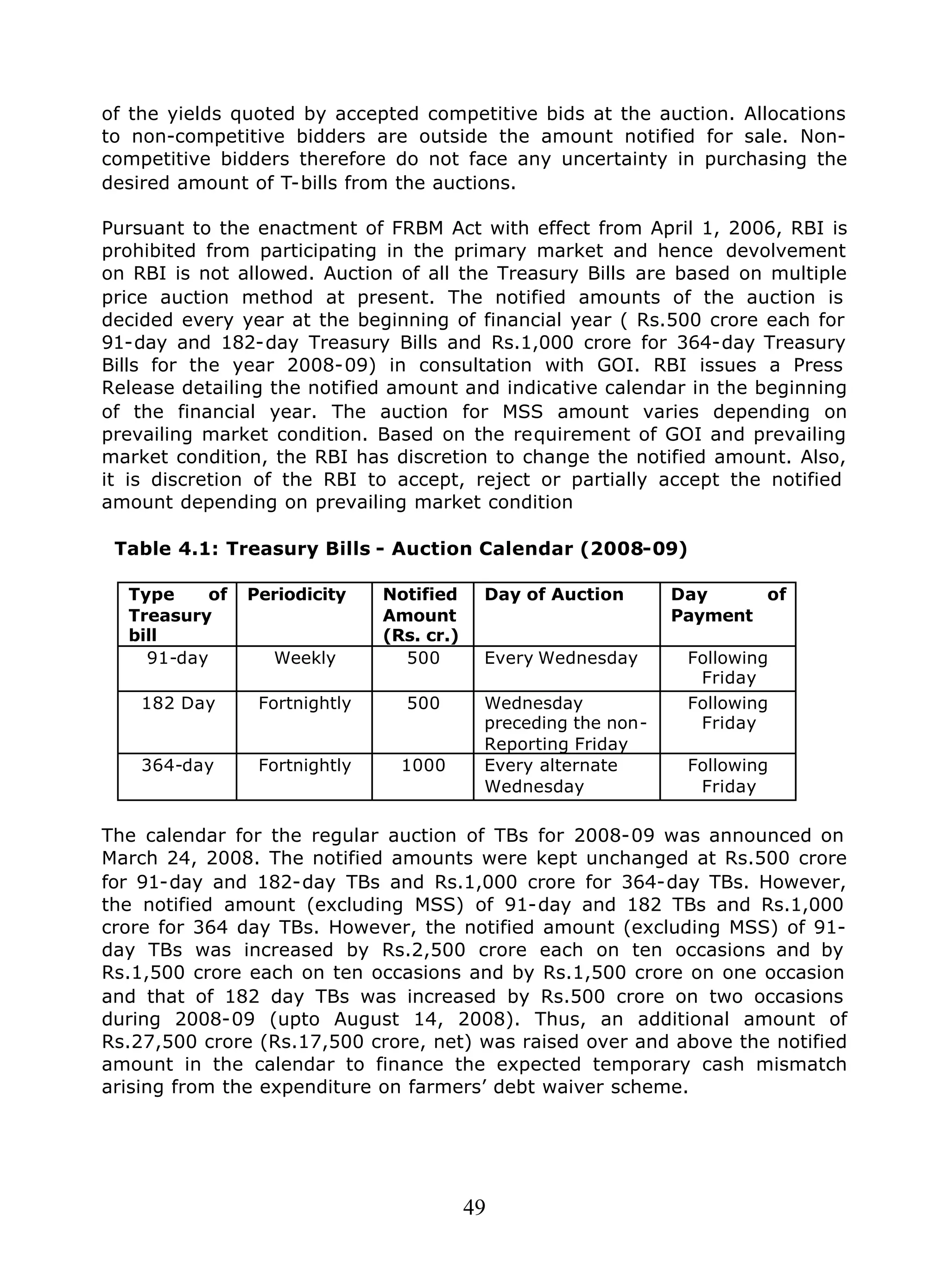

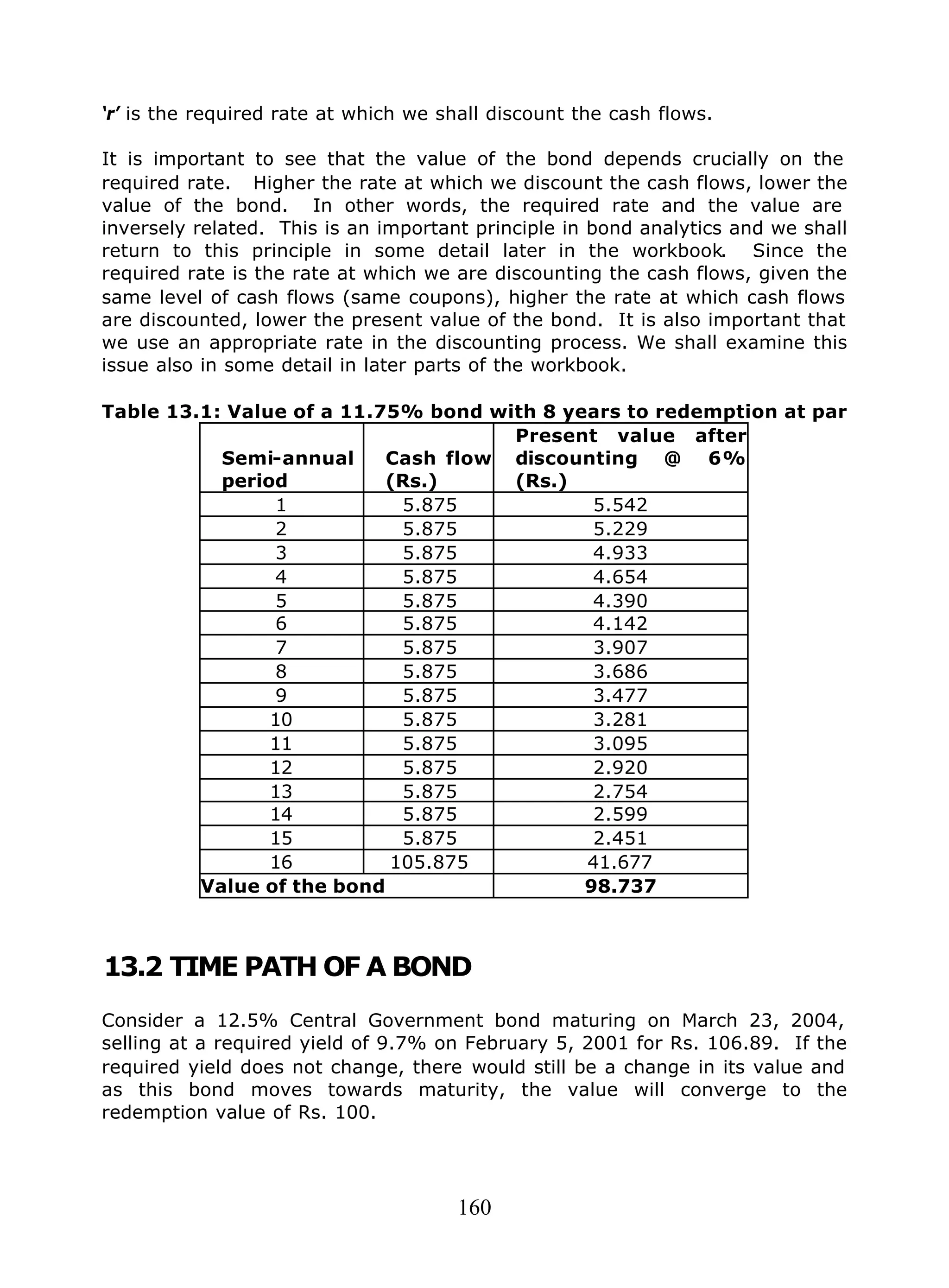

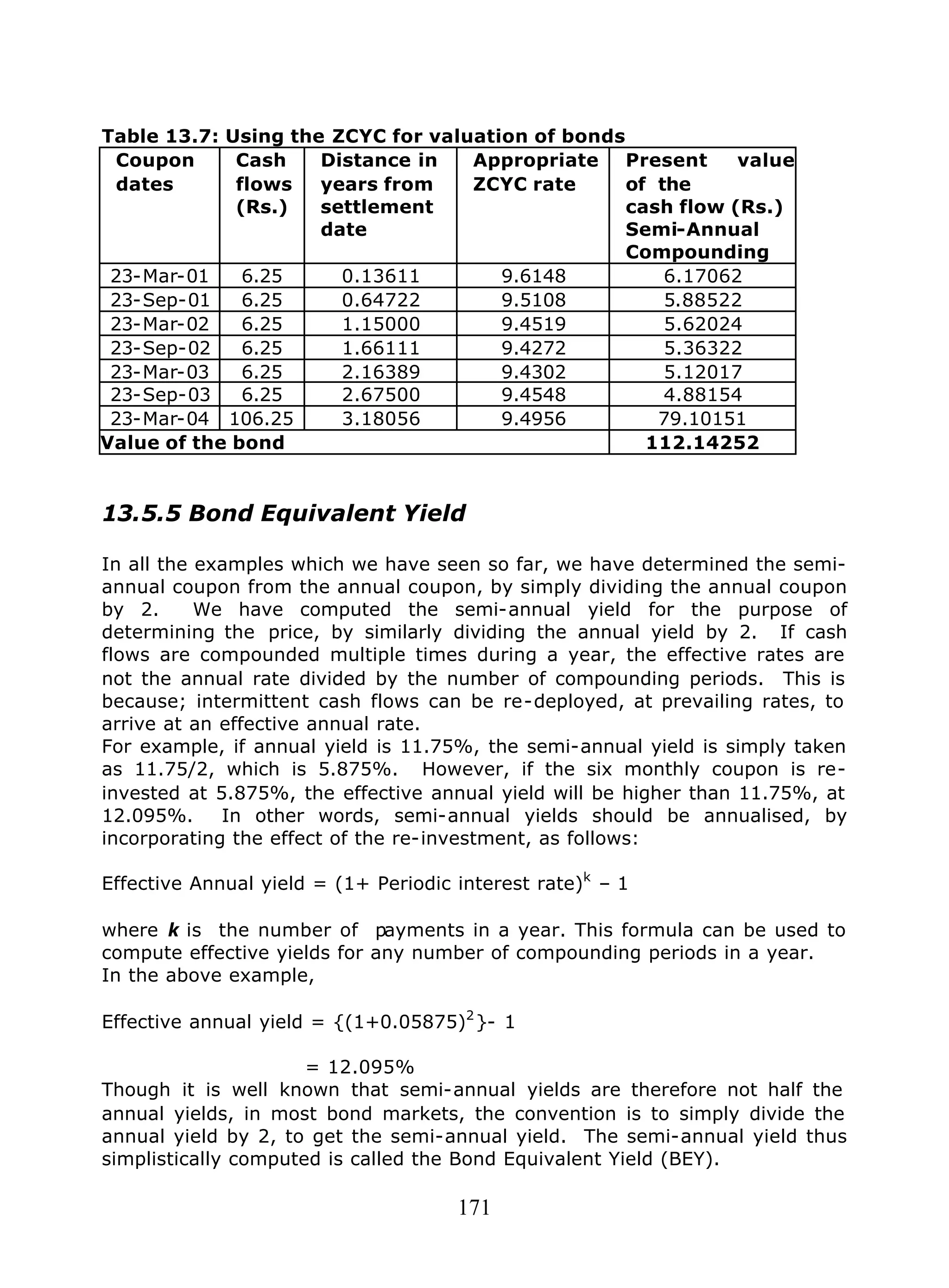

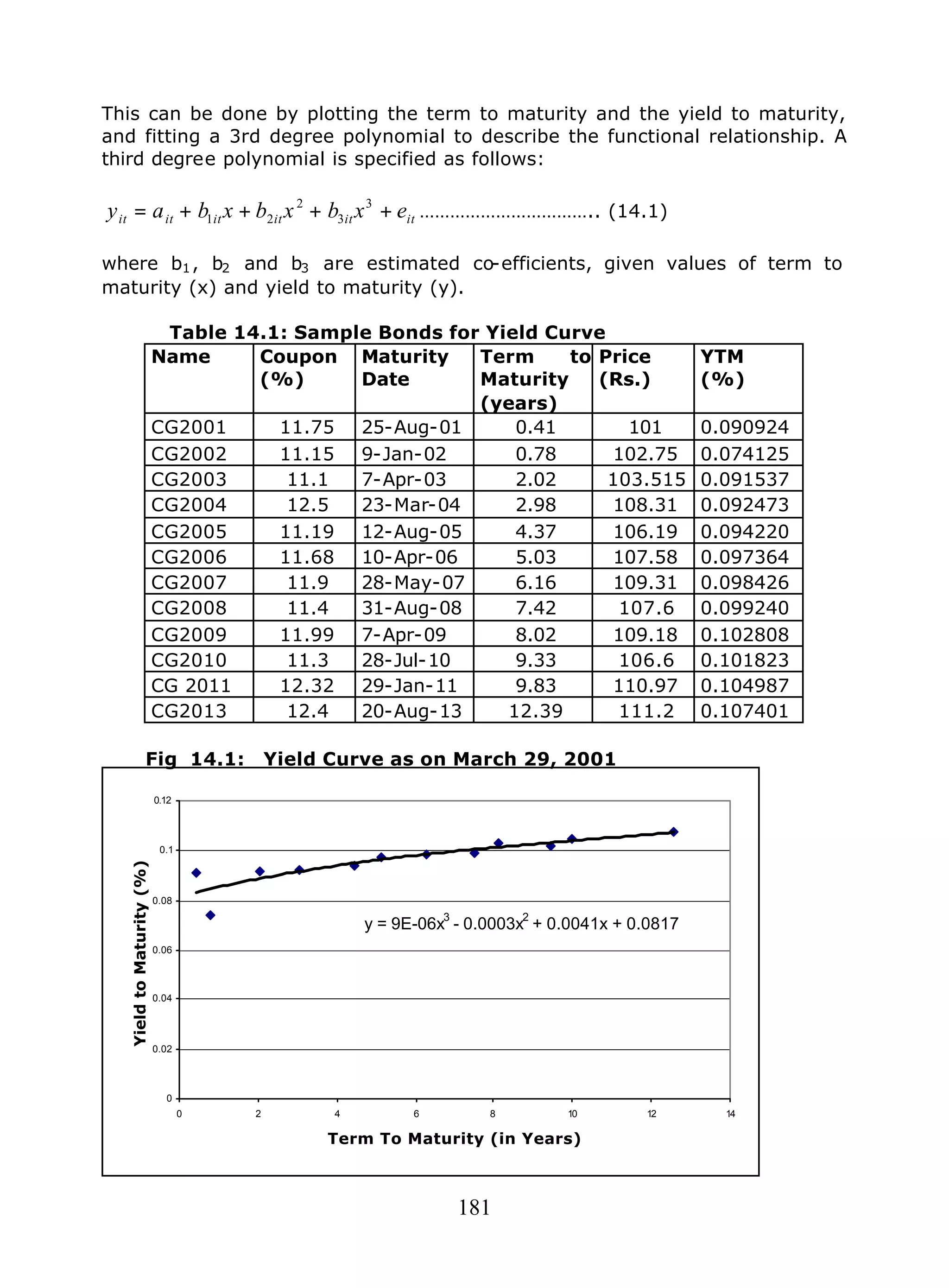

![164

Table 13.4: Coupon days for settlement date February 5, 2001

Name of the

Security

Maturity

Date

Number

of

coupons

until

maturity

Number of

days in the

coupon

period

Number of

days from

previous

coupon

to settlement

Number of

days from

settlement to

next coupon

CG 12.5% 2004 23-Mar-04 7 180 132 48

CG 11.68% 2006 10-Apr-06 11 180 115 65

CG 11.5% 2008 23-May-08 15 180 72 108

CG 11.3 % 2010 28-Jul-10 19 180 7 173

In order to value a bond, on a settlement date that is not a coupon date, we

have to re-cast the bond valuation equation 13.1, as follows:

)]/()1[()]/(1[

2

)/(

1

0

)1(

.........

)1()1( dicpdncn

n

dicpdncdicpdnc

r

c

r

c

r

c

P +−+

++

+

+

= …………(13.2)

Where c1, c2 .. cn are expected cash flows from the bond. Given the

redemption value, coupon rate and frequency of coupons, we can compute

these cash flows.

dnc is the number of days to the next coupon

dicp is the days in the coupon period

Since the first cash flow c1, is only dnc/dicp periods away from the settlement

date, we discount it only for that period. For the subsequent cashflows, we

can generalise the period for which discounting is to be done, as [(n-1) +

dnc/dicp]. We can use the “price” function in Excel, in order to use equation

13.2 in actual valuation of a bond. Alternatively, we can use the coupon

functions to find out the values in equation 13.2 and value the bond using the

PV function.

The value of the same bond, by merely varying the day count convention

(change the basis in Excel to 1, 2 and 3) can vary to Rs. 99.0136, Rs.

99.0143 ands. 99.0134 respectively.

Using Excel, readers can check the impact of changes in the day count

convention and the frequency of coupon payments on the value of the bond.

Are there any generalisations here?](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-165-2048.jpg)

![185

= 6.542 + [(6.675-6.542)] x [(42-40)/(52-40)]

= 6.56416%

3. The bootstrapping technique is sensitive to the liquidity and depth in

the market. In a market with few trades, and limited liquidity,

bootstrapping is only an approximation of the true term structure, due

to simple assumptions (like linear interpolation) made for linking up

rates for one tenor and the rates for another. It is not uncommon for

some to use more sophisticated non-linear interpolations.

14.3 ALTERNATE METHODOLOGIES TO ESTIMATE THE

YIELD CURVE

In the estimation of the yield curve from a set of observed market prices, the

following are important considerations:

a. The spot rates and the yield curve that is estimated should have a

close fit with market prices. That is, the prices estimated by the

model and the prices actually prevalent in the market should have a

close fit.

b. The mo del must apply equally well to bonds which are not part of the

sample used for estimation. That is, if a very close fit is sought to be

achieved, it may come at the cost of the model not being able to value

out-of-sample bonds. The model would have incorporated “noise” in

the estimation.

c. The estimated yield curve should be smooth, such that the spot and

forward rates derived from them do not show excessive volatility.

A number of mathematical techniques are used to generate a fitted yield

curve from a set of observed interest rate points. They involve optimality

criteria consistent with the assumptions regarding the term structure of

interest rates.

14.3.1 NSE –ZCYC (Nelson Seigel Model)

In the Indian markets, term structure estimation has been done, and is

disseminated every day by the National Stock Exchange. The Zero Coupon

Yield Curve (ZCYC) published by the NSE, uses the Nelson-Seigel

methodology. 12 The Nelson-Siegel formulation specifies a parsimonious

representation of the forward rate function given by

)]/exp()/[()/exp(),( 210 ττβτββ mmmbmf −∗+−∗+=

……………..(14.4)

12

The paper (Gangadhar Darbha, et al, 2000) that describes the methodology can be downloaded

from www.nse.co.in `products`zcyc. The following section is extracted from this paper.](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-186-2048.jpg)

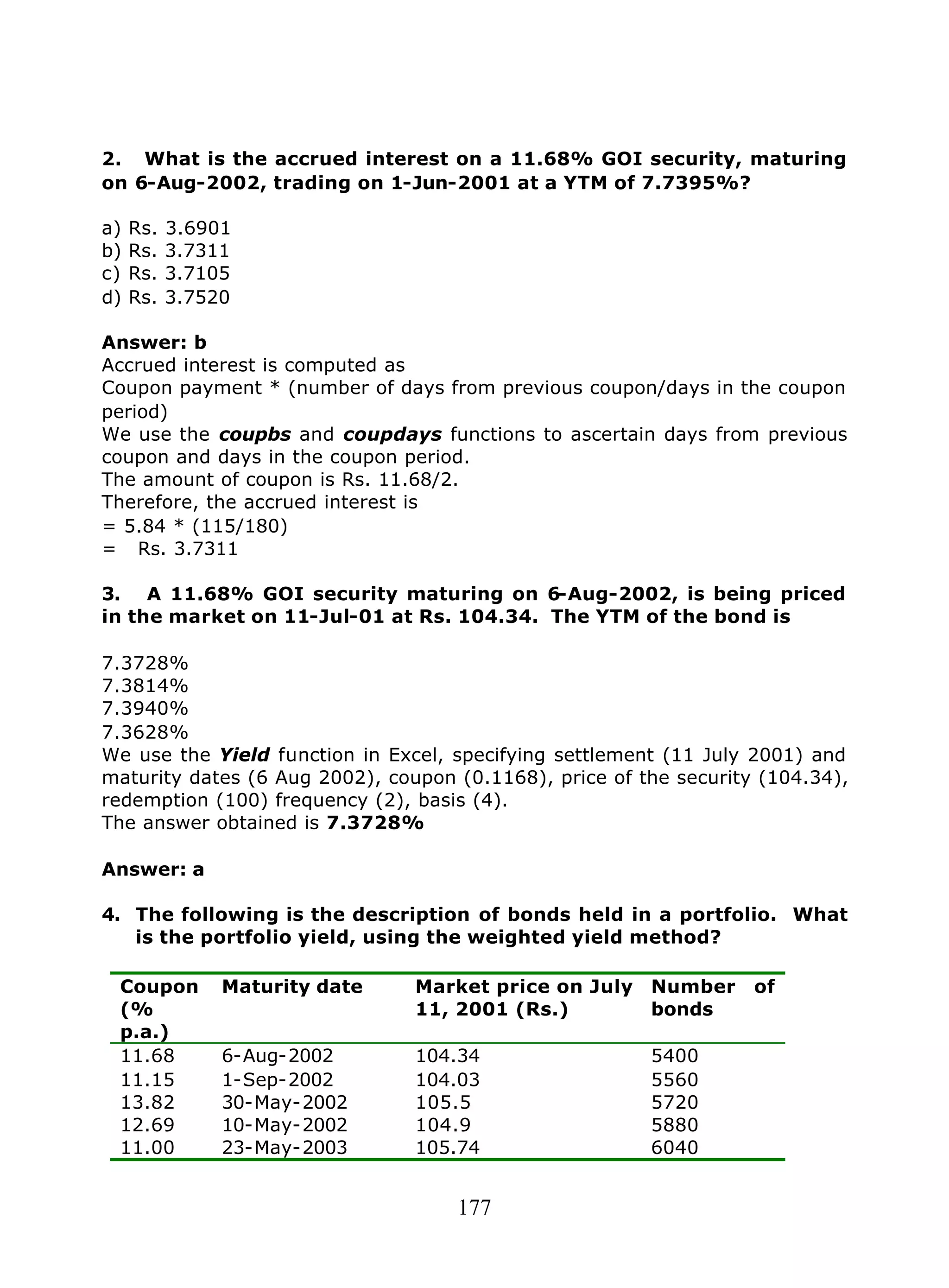

![186

where ‘m’ denotes maturity and b=[ β0, β1, β2 and τ] are parameters to be

estimated.

Since the model is based on the expectations hypothesis, it develops the term

structure from the no-arbitrage relationship between spot and forward rates.

The forward rate function can be mathematically manipulated (integrated) to

obtain the relevant spot rate function, the term structure:

)/exp()//()]/exp(1[)(),( 2210 τβττβββ mmmbmr −∗−−−∗++= …………………(

14.5)

In the spot rate function, the limiting value of r(m,b) as maturity gets large is

β0 which therefore depicts the long term component (which is a non-zero

constant). The limiting value as maturity tends to zero is β0 + β1, which

therefore gives the implied short-term rate of interest.

With the above specification of the spot rate function, the PV relation can now

be specified using the discount function given by

∗

−=

100

),(

exp),(

mbmr

bmd …………………..(14.6)

The present value arrived at is the estimated/model price (p_est) for each

bond. It is common to observe secondary market prices (pmkt) that deviate

from this value. For the purpose of empirical estimation of the unknown

parameters in term structure equation above, we postulate that the observed

market price of a bond deviates from its underlying valuation by an error

term ei, which gives us the estimable relation:

iii eestppmkt += _ ……………………(14.7)

This equation is estimated by minimising the sum of squared price errors. The

steps followed in the estimation procedure are as follows:

i. A vector of starting parameters (β0, β1, β2 and τ) is selected,

ii. The discount factor function is determined using these starting

parameters,

iii. This is used to determine the present value of the bond cash flows and

thereby to determine a vector of starting ‘model’ bond prices,

iv. Numerical optimization procedures are used to estimate a set of

parameters (under a given set of constraints viz. non-negativity of long

run and short run interest rates) that minimise the sum of squared price

errors,

v. The estimated set of parameters are used to determine the spot rate

function and therefrom the ‘model’ prices (this is the first set of results

we compute for each day),

vi. These ‘model’ prices are used to compute associated ‘model’ YTMs for

each bond (this is the second set of results).

Plots of the estimated term structure for any particular day can be obtained

by following the procedure below:](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-187-2048.jpg)

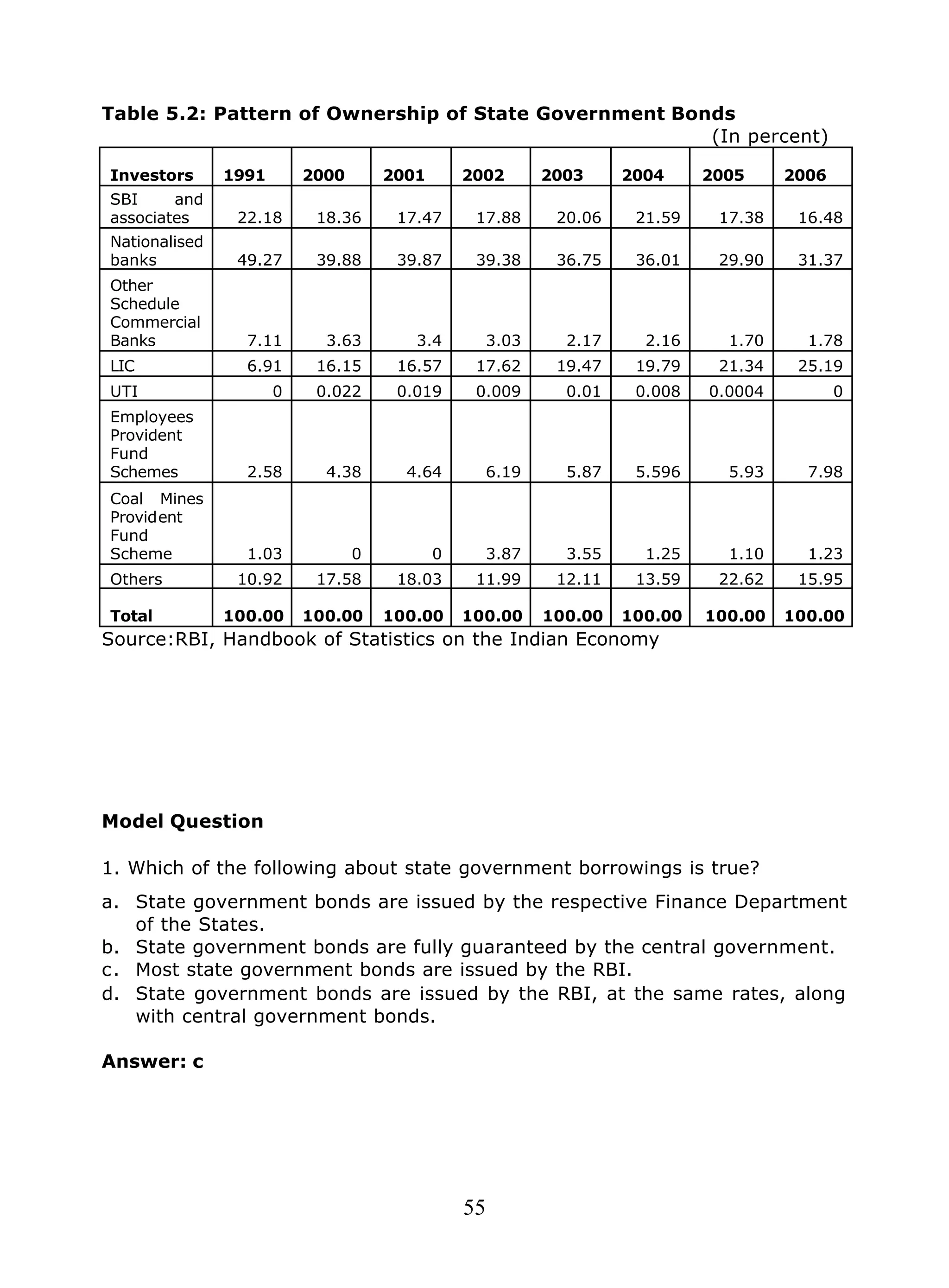

![190

Model Questions

1. The NSE ZCYC estimates for July 11, 2001 are as follows:

Beta 0 = 11.4652

Beta 1 = -2.2510

Beta 2 = -10.7202

Tau = 1.4197

What is the spot rate for a term to maturity of 3.5 years?

Answer:

We use the ZCYC valuation equation (14.5)

)/exp()//()]/exp(1[)(),( 2210 τβττβββ mmmbmr −∗−−−∗++=

We can take the values provided by NSE to an Excel Spreadsheet, and key in

the formula above, substituting 3.5 for m in the equation, and substituting

the NSE estimates for B0, B1 and B2 and Tau. We then get

= 11.4652 + ((-2.2510-10.7202)*(1-exp(-3.5/1.4197))/(3.5/1.4197)-(-

10.7202*exp(-3.5/1.4197))

= 7.56185%

2. If there are 2 bonds trading in the market as follows, on July 11,

2001 as detailed below:

i. 11.98% 2004 (Maturity 8-Sep-2004): Rs. 111.8

ii. 11.19% 2005 (Maturity 12 Aug 2005): Rs. 111.83

What is the linearly interpolated rate for 3.5 years, using the above

data?

Answer:

Using the Yield function, we can find out the YTM of the above bonds as

7.6917% and 7.7524% respectively. Using the yearfrac function, we can

find the term to maturity of these bonds as 3.1583 years and 4.0861 years

respectively. To find the YTM for a 3.5 year bond, we can do a linear

interpolation, as follows:

= 7.6917 + (7.7524-7.6917)*((3.5-3.1583)/(4.0861-3.1583))

= 7.7141%

3. If the yield curve is upward sloping, which of the following is

false?

a. The market expects short term interest rates to increase.

b. The liquidity premium is increasing with increase in tenor.

c. There is an excess of demand over supply in shorter maturities.

d. The interest rates are positively related to term, along the yield

curve.

Answer: c](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-191-2048.jpg)

![222

b) If the hedge is not found to be "highly effective" no set off will

be allowed and the underlying securities will be marked to

market as per the norms applicable to their respective

investment category.

c) Trading position in futures is not allowed. However, a hedge

may be temporarily rendered as not “highly effective”. Under

such circumstances, the relevant futures position will be

deemed as a trading position. All deemed trading positions

should be marked to market as a portfolio on a daily basis and

losses should be provided for and gains, if any, should be

ignored for the purpose of Profit & Loss Account. SCBs and

AIFIs should strive to restore their hedge effectiveness at the

earliest.

d) Any gains realized from closing out / settlement of futures

contracts can not be taken to Profit & Loss account but carried

forward as "Other Liability" and utilized for meeting

depreciation provisions on the investment portfolio.

vii) Capital adequacy : The net notional principal amount in respect of

futures position with same underlying and settlement dates should

be multiplied by the conversion factor given below to arrive at the

credit equivalent:

Original Maturity Conversion Factor

Less than one year 0.5 per cent

One year and less than two years 1.0 per cent

For each additional year 1.0 per cent

The credit equivalent thus obtained shall be multiplied by the

applicable risk weight of 100%.

viii) ALM classification: Interest rate futures are treated as a

combination of a long and short position in a notional government

security. The maturity of a future will be the period until delivery or

exercise of the contract, as also the life of the underlying

instrument. For example, a short position in interest rate future for

Rs. 50 crore [delivery date after 6 months, life of the notional

underlying government security 3½ years] is to be reported as a

risk sensitive asset under the 3 to 6 month bucket and a risk

sensitive liability in four years i.e. under the 3 to 5 year bucket.](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-223-2048.jpg)

![234

PVBP

Also called the Price Value of a Basis Point or Dollar Value of 01. This is one

way of quantifying the sensitivity of a bond to changes in the interest rates. If

the current price of the bond is P(0) and the price after a one basis point rise

in rates is P(1) then PVBP is -[P(1)-P(0)]. This can be estimated with the help

of the modified duration of a bond, as (Price of the bond * modified duration*

.0001)

Repo

Repo or Repurchase Agreements are short-term money market instruments.

Repo is nothing but collateralized borrowing and lending. In a repurchase

agreement securities are sold in a temporary sale with a promise to buy back

the securities at a future date at specified price. In reverse repos securities

are purchased in a temporary purchase with a promise to sell it back after a

specified number of days at a pre-specified price. When one is doing a repo, it

is reverse repo for the other party

Reverse Repo

See Repo

Risk Free Rate

An interest rate given out by an investment that has a zero probability of

default. Theoretically this rate can never exist in practice but sovereign debt

is used as the nearest proxy.

SGL

Subsidiary General Ledger Account is the demat facility for government

securities offered by the Reserve Bank of India. In the case of SGL facility the

securities remain in the computers of RBI by credit to the SGL account of the

owner. RBI offers SGL facility only to banks and primary dealers.

SLR

This is the acronym for Statutory Liquidity Ratio. That part of their Net

Demand and Time liabilities (NDTL) that a bank is required by law to be kept

invested in approved securities is known as SLR. The approved securities are

typically sovereign issues. The maintenance of SLR ensures a minimum

liquidity in the bank's assets.

Spread

Spread is the difference between two rates of interests. It is often generalised

to imply the difference between either price or yield. Spreads can be between

two risk classes or can be between tenors in the same risk class. For example

130 bps between AAA and GOI means a 1.30% spread between a AAA issue

and that made by the Government of India. 5 paisa spread between bid and

ask means that in the two way price quoted the difference between the buy

and sell price is 5 paisa 60 bps spread between 3 month T Bill over 10 Year](https://image.slidesharecdn.com/fimmda-101119095005-phpapp01/75/Fimmda-235-2048.jpg)

The document provides information about copyright and ownership of the content in the book titled "Debt Instruments and the Indian Debt Market". It states that the book, including all text, graphics, images, and data is the property of National Stock Exchange of India. The content from the book cannot be copied, reproduced, sold or used for commercial purposes without permission. It also cannot be stored or transmitted electronically or otherwise.