Download to read offline

![MARKET-LINKED TERM INVESTMENTS

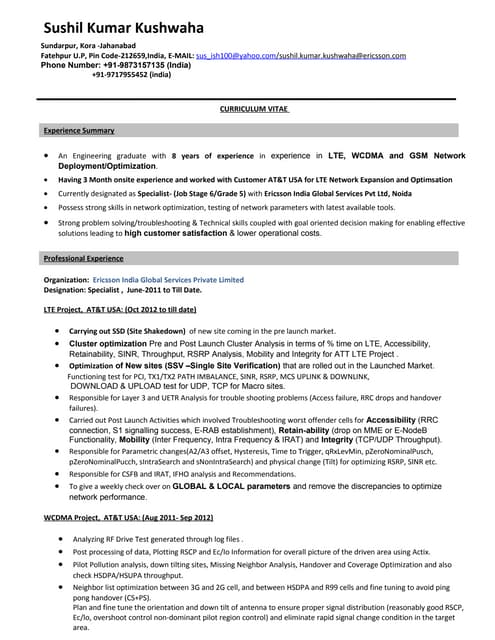

Features

Minimum Deposit 1

$500

Deposits are accepted up to age 95.

Eligibility for registered plans 2,3 RRSPs, RRIFs, LIRAs, LIFs, TFSA and non-registered

Surrender option

The Initial Deposit may be surrendered or transferred in full or in part at any time.

Surrender Value = Current Value – [(compound interest rate on Deposit with similar remaining term + 1.5%)

X number of years to maturity remaining X Current Value]

The Surrender Value cannot be greater than the Initial Deposit.

Death Benefit guarantee

The Death Benefit amount is equal to 100% of the Initial Deposit.

Interest on Deposits made

before an Initial Date

Interest rate of the special Daily Interest Fund: 1%

Management fees

No fees

Participation rate

100%

Assuris protection

Yes

Creditor protection

4

When a “preferred” Beneficiary or an irrevocable Beneficiary is named.

Specific Business Days

Specific Business Days are used to calculate the Investment rate of Return.

3 years et 2 days

5 years et 2 days

Healthcare

December 12, 2016

January 12, 2017

February 13, 2017

December 12, 2018

January 15, 2019

February 12, 2019

Consumer Staples

Financials

Global Diversified

December 14, 2016

January 17, 2017

February 14, 2017

December 14, 2018

January 15, 2019

February 14, 2019

To write on the Contract Application

“GA” followed by the name of the basket of securities and the return option chosen by the client. For example:

GA Healthcare 0-10

GA Financials 5-18

All Deposits are initially invested in a special Daily Interest Fund pending their investment on

the next issue date. The sum accumulated (minimum $500) on this date, called the Initial Date,

constitute the Initial Deposit and will be invested in Guarantee Advantage®. The maturity date

of a PAC depends on the Initial Date and term.

2

Eligible for LIFs only under the Quebec legislation.

3

No periodic payments for a RRIF or a LIF.

4

This is for your information only and does not constitute a legal opinion. The exemption from

seizure rules can differ by province and can be very complex. Contracts are subject to seizure if it

can be proven that the plan was set up to avoid paying off a debt or if the insured goes bankrupt

within one year of designating a Beneficiary. We recommend that you contact a lawyer or notary

to review your specific situation.

The information contained in this material is subject to change without notice.

Desjardins Insurance reserves the right to suspend Guarantee Advantage® Deposits for

the February 2014 campaign or to postpone the Initial Date.

09014E (13-11)

1

Desjardins Insurance refers to Desjardins Financial Security Life Assurance Company.

100%

®

Registered trademark owned by Desjardins Financial Security](https://image.slidesharecdn.com/featurestable-ga-february2014-131127121549-phpapp01/85/Guarantee-Advantage-February-2014-campaign-2-320.jpg)

This document describes market-linked term investments offered by Desjardins Insurance in February 2014. It lists the securities in various sectors including healthcare, consumer staples, financials, and global diversified. The terms are either 3 years and 2 days or 5 years and 2 days, with initial dates in February 2014 and maturity dates in February 2017 or February 2019 depending on the term. The return options provide either a guaranteed minimum return between 0-1.5% or a potential maximum return between 7-18% depending on the sector and term. The investments have features such as a $500 minimum deposit, eligibility for registered plans, a surrender option, a death benefit guarantee, and Assuris protection.

![Benefit gold brochure[1]](https://cdn.slidesharecdn.com/ss_thumbnails/benefitgoldbrochure1-130524121432-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Mas 500] Various Topics](https://cdn.slidesharecdn.com/ss_thumbnails/mas-500-6-prototype-to-product-131127121510-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)