Download to read offline

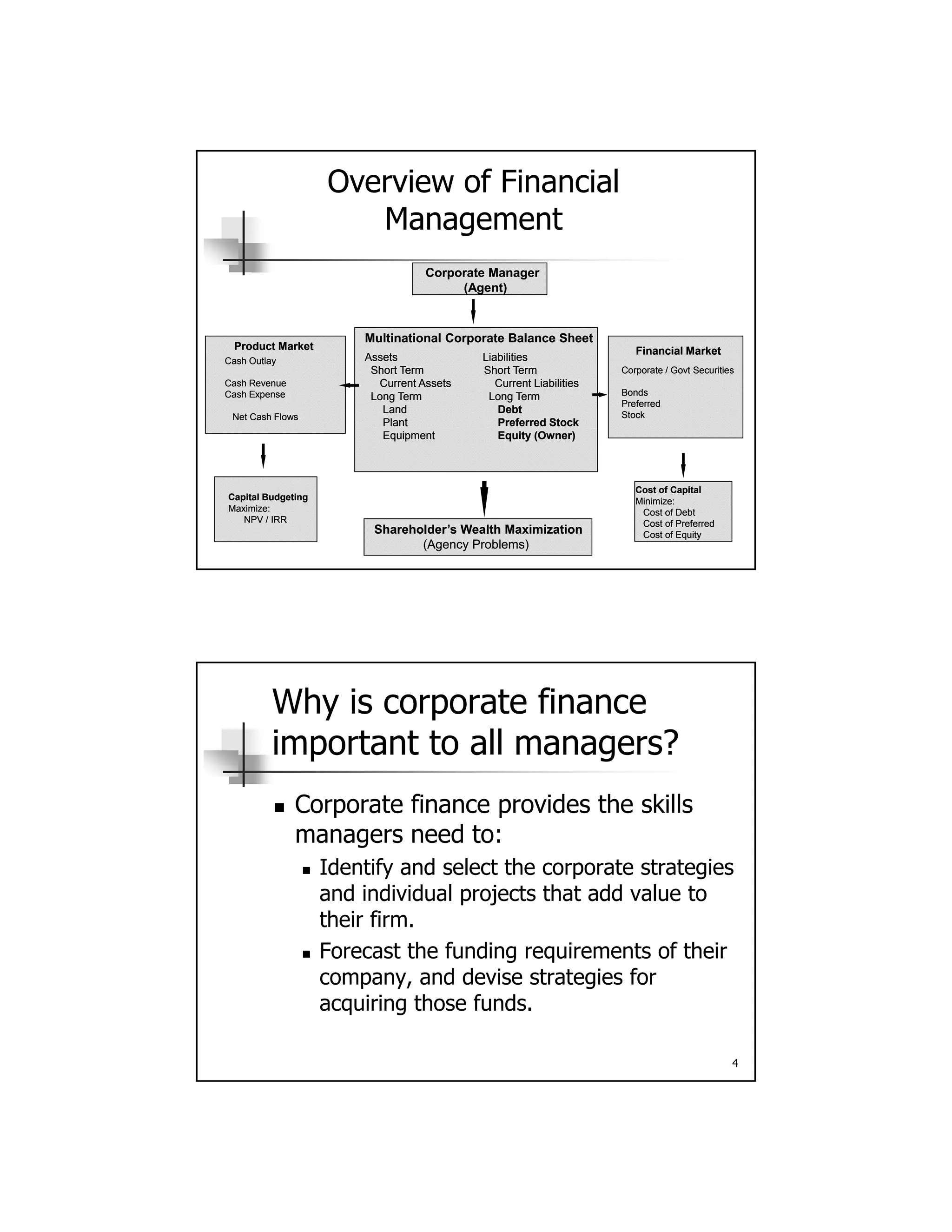

This chapter provides an overview of financial management and the financial environment. It discusses forms of business organization including sole proprietorships, partnerships, and corporations. The chapter explains that the primary objective of corporate managers should be to maximize shareholder wealth. It also outlines key concepts such as free cash flows, weighted average cost of capital, and how the cost of debt and equity capital are determined. The chapter concludes with a discussion of financial securities, primary and secondary markets, and how secondary markets are organized.