Download to read offline

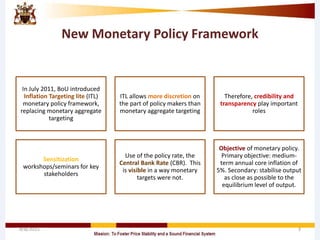

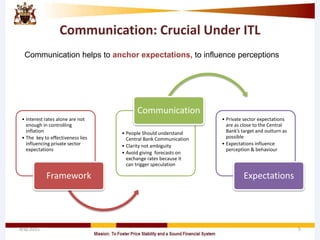

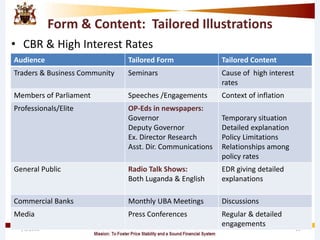

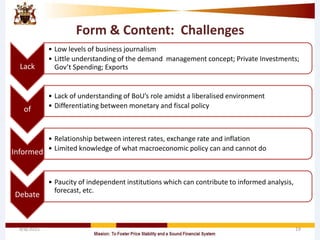

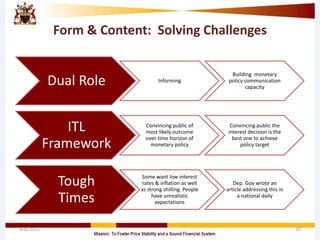

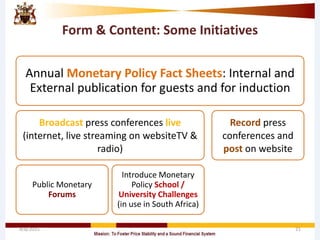

The document discusses the shift to an inflation targeting lite (ITL) monetary policy framework introduced by the Bank of Uganda in July 2011, emphasizing the importance of communication in managing private sector expectations and ensuring the framework's effectiveness. It outlines the roles of various stakeholders in communicating monetary policy decisions, the challenges faced, and the strategies employed to engage different target audiences through media and tailored content. The conclusion highlights that effective communication significantly enhances the credibility and transparency of monetary policy, making its understanding crucial for stakeholders.

![Donor_Coordination[1]](https://cdn.slidesharecdn.com/ss_thumbnails/f1c36507-c22f-4ff8-93c6-d51d26ffdb30-150519103644-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)