Executive summary for "Look Back in Anger" report

This is the executive summary for the “Look Back in Anger” global energy forecast. It’s so called because it imagines the reactions of energy industry veterans arriving in 2050 to a net-zero emission world. Yes, that’s cause for celebration, but why were there so many barriers put in their way? Why did we make it so hard for ourselves? To get to this moment, instead of looking through the lens of how it has always been, “Look Back in Anger” assumes key tipping points along the way. It’s a simplified global energy model, from now until 2050 that anyone can use to test their own business assumptions. The report assumes the effect of official decarbonisation policy in the top 21 countries by energy usage, accounting for about 84% of electricity use. From there it plots the minimum that will be spent on renewables and builds a picture of the energy world in thirty years’ time. By definition, this leaves a set of imponderables like: What is the impact of home-heating and cooling in the age of electrification by 2050? What happens when solar manufacturers double their capacity and have to sell twice as much, triggering price wars? What happens when rooftop solar accelerates? The report is part of the unique “Rethink Energy” research service that offers full access to all previous report plus 12 other new forecasts each year on a variety of topic drawn from batteries, solar, wind, EV recharging, and decarbonising industries like Steel. More information at https://rethinkresearch.biz/reports-category/rethink-energy-research/

Recommended

More Related Content

Similar to Executive summary for "Look Back in Anger" report

Similar to Executive summary for "Look Back in Anger" report (20)

Recently uploaded

Recently uploaded (20)

Executive summary for "Look Back in Anger" report

- 1. R E T H I N K T E C H N O L O G Y R E S E A R C H https://rethinkresearch.biz Companies mentioned in this report: Android, Amazon, Apple, Bloomberg, BP, BYD, Canadian Natural Resources, Cemex, Chevron, China National Offshore Oil Corp, China Petrochemical Corp, China Petroleum & Chemical Corp, ConocoPhillips, DHL, DPD, Duke, Ericsson, ExxonMobil, FedEx, Ford, General Motors, Google, GWEC, IEA, Imperial Oil, Jaguar Land- Rover, Mercedes, NIO, Netflix, PSEG, Qualcomm, R&D, Rivian, Rolls Royce, Royal Dutch Shell, Scania, SEIA, Shell Energy North America, Sony, S&P Global, Spotify, Suncor, Tesla, Total, Uber, UPS, Volkswagen, Wood Mackenzie, Xcel Energy Lead analyst: Peter White Look Back in Anger IT’S 2050 AND THE WORLD IS CLOSE TO ZERO EMISSIONS HOW DID WE DO IT? “ R e t h i n k h a s a c o m m i t m e n t t o f o r e c a s t i n g m a r k e t s t h a t o t h e r s s h y a w a y f r o m – t h o s e o n t h e v e r g e o f r a d i c a l t r a n s f o r m a t i o n ”

- 2. Copyright © 2021 Rethink Research, All rights reserved. 2 CONTENTS Page Contents 2 Graphs and Tables 4 Look Back in Anger 5 How to Look Back in Anger 6 Stock Markets 7 Energy Trade 8 Bankruptcies 8 Transition in a Nutshell 9 Electric Vehicle revolution 10 How do solar and wind progress to 2015 11 How do you wind down the oil industry? 13 Any old cars 14 Will electricity be any cheaper? 15 The Distributed Energy Revolution 17 The world “Sans gas” 19 But still they were angry 20 Fake News 21 How Change Works 23 What about 100 year-olds? 23 The forecasts so far are rubbish 25 To forecast change you practice on industries that actually change 29 The great PC crash of 2000 30 Investor pressure 32 The Myth of Primary Energy 34 Electricity Growth 36 A bursting grid 37 The Global view 38 Emissions from electricity 38 Natural Gas For Electricity generation 39 Steel Making 40 Cement Making 41 Coal Usage 42 Land Transport 43 I want one, I can afford one and I know someone who has one 45

- 3. Copyright © 2021 Rethink Research, All rights reserved. 3 Keeping ICE all together 46 The top end goes hydrogen first 47 Hydro Generation 48 Nuclear Power 49 Total Global Generation 50 Leading country energy profiles 51 China 51 Home Heat 51 EV uptake 52 Steel and Cement 52 USA 54 Home Heat 54 EV uptake 55 Steel and Cement 55 India 56 Home Heat 56 EV uptake 57 Steel and Cement 58 Germany 58 Home Heat 59 EV uptake 59 Steel and Cement 60 Japan 60 Home Heat 61 EV uptake 61 Steel and Cement 62 South Korea 62 Home Heat 63 EV uptake 63 Steel and Cement 64 Significant Others 64 Conclusion 65 Methodology 69 Contacts 71 About Rethink Technology Research 72

- 4. Copyright © 2021 Rethink Research, All rights reserved. 4 GRAPHS AND TABLES Page Growing profit margins of Utilities 16 PC forecast vs actual sales from 1998 to 2002 30 Land Transport in Transition to 2050 by number of vehicles 33 China total electricity output by fuels 2020 34 China total electricity output by fuels and extras 2050 35 China total electricity output by fuels and extras 2050 35 Non-CO2 electricity generation growth by major countries to 2050 39 Global Natural Gas Electricity Generation 39 Amount of electricity needed for steelmaking, growth to 2050 40 Amount of electricity needed for cement making, growth to 2050 42 Global Coal electricity generation to 2050 42 Land Transport in Transition to 2050 by CO2 emissions 43 EV sales by units by country to 2050 44 Land Transport - EV annual shipments and cumulative totals to 2050 45 Global Hydro Electric power planned to 2050 48 Global electricity generation from nuclear power to 2050 49 Global Total Electricity Demand 2050 - absorbing transport, steel, cement and home heat 50 Chinese electricity usage by source to 2050 in GWh 51 EV growth in China to 2050 52 Electricity expected to be used in steelmaking in China in GWh 53 USA electricity usage by source to 2050 in GWh 54 EV growth in USA to 2050 55 Indian electricity usage by source to 2050 in GWh 56 Germany electricity usage by source to 2050 in GWh 58 Japanese electricity usage by source to 2050 in GWh 60 South Korea electricity usage by source to 2050 in GWh 63 Other majors - Extra electricity to decarbonize in percentage terms 64

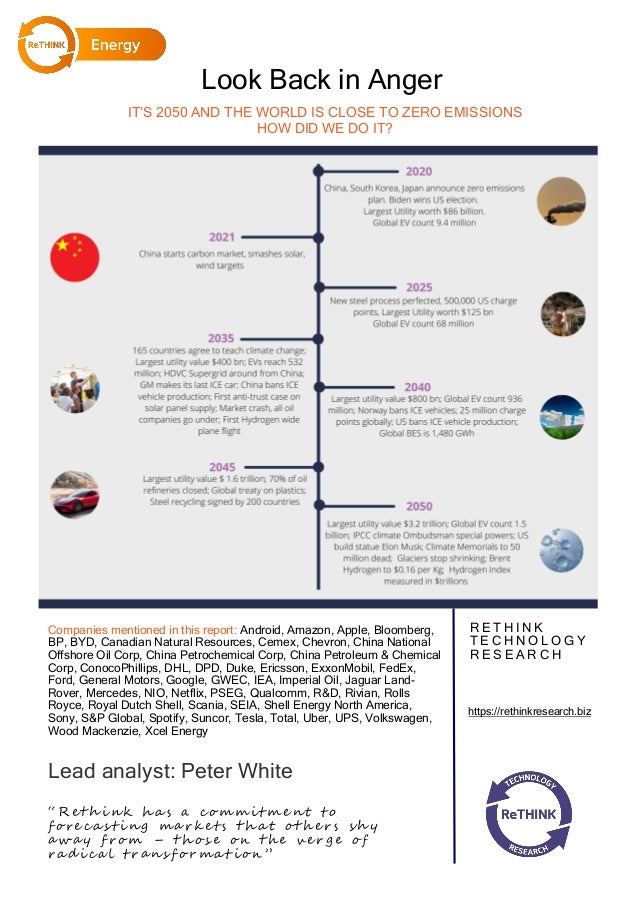

- 5. Copyright © 2021 Rethink Research, All rights reserved. 5 Look Back in Anger is about imagining that it’s 2050, and that we have, more or less, achieved net zero emissions. So, what would it look like? To find out you need a confident forecast of just what steps it took to achieve it, and from there it seems to us it is possible to put some detail on the bare bones of what it must have taken to get there. The title of this paper belongs to a famous play written in 1956, reflect- ing the anger of a working class intellectual in a class war he felt he could not win. It is where the expression “Angry young men” came from. Today it is perhaps schoolchildren like Greta Thunberg and young eco-warriors, who are angry with the climate war. Perhaps the men and woman who have taken it upon themselves to make this revo- lution happen – mostly engineers working at utilities, renewable devel- opers and vendors - and perhaps when they look back, they too may end up feeling a little angry, that this transition was made so hard for them, when it could have been so easy, so predictable. By the time we reach 2050, will anger remain the abiding memory of the energy transition? Climate change deniers today tend to be over 60 – in 2050 those same people will be over 90, as will most investors who remember investing in coal, and the young who are today calling for a climate emergency will be close to 50, perhaps ready to recount their life stories – “What did you do in the climate war Daddy?” Even reactionary politicians today, who simply could not imagine aid- ing the death of the internal combustion engine or ridding the world of coal jobs or supporting energy subsidies for solar, will have grown used to the new energy economy. And as renewables prices continue to fall – possibly by 80% in solar and wind once again, as they have in the past 10 years – then surely all resistance to renewables must evaporate by 2030. By 2050 they are facts of life. People will be very used to the idea of decarbonizing. It has almost be- come second nature to some already. It will be taught in schools all Look Back in Anger

- 6. Copyright © 2021 Rethink Research, All rights reserved. 6 over the world, climate change denying will be impossible to maintain, and those who remember it will be far older, and eventually forgotten. But there will remain a seething resentment that all this was really easy to get done – decarbonizing, once we started to get on and do it. It was much simpler in the final days, than it has been in than the early days, when everything was against an energy transition ever happening and no-one knew why or quite who the enemy was. As we look back at decarbonization in 2050 we find that Elon Musk is 79 years old, someone who refused to sit on the sidelines, and who turned the idea of the energy transition into a fortune. By now there are over 100 Elon Musk style billionaires, neatly arranged on every conti- nent and in every sector of the energy space. They all got it right. By using Rethink Energy’s 30 year model, we can see that looking back it was all pretty obvious, all we needed to do was to give some talented engineers the cash to go and solve problems, but we also had to be sure they solved the right problems. Not geo-engineering or CCUS, or Di- rect Air Capture, which are battling to provide life-support against the terminal decay of fossil fuels. To have an inkling how it happened, you must first have a good stab at just how these things could have come about, and that’s what this pa- per is all about. Perspective is a wonderful thing, and if you have to ask yourself how China will manage to multiply its nuclear capacity six- fold within this forecast - the answer will be that centralized govern- ance can control spending, safety and prices; today China has already has 32 nuclear power stations in planning. But ask the same question about how it can possibly reach over 16 times the renewables that it has installed today by 2050, and the truth is that at the rate at which wind and solar declined in price over the past decade, it meant that there was barely an increase total annual in spend from 2020. In the next 20 years, solar will fall to around 20% of its price today; wind perhaps to 40% of its current price. So a 16-fold growth in renew- How to Look Back in Anger

- 7. Copyright © 2021 Rethink Research, All rights reserved. 7 ables will require just 3.75 times the spend on renewables that was spent in 2020. For wind the sum is a little more, but then again its output is also much more predictable. To pay for this, China will be able to harness substantially larger revenues each year, from selling so much more electricity, and at much the same price as it always has. In the attached graphic “Transition in a nutshell” we can see that today the largest energy utility is worth $86 billion – but at the current rate of growth and the same multiple, by 2050 some of these companies will be delivering so much more energy, and at such a high margin, they will be worth $3.2 trillion. At least one of these will be in Chi- na. We must always remember that someone ended up owning all this gener- ational capacity. And because the price of electricity will not have fallen so very much for the consumer, many utility companies around the world will have increased in size by at least 10-fold, some 20-fold. Their value will have increased by closer to 40 times, depending on market controls and how much the central government regulates electricity pricing. But once prices start to fall, regulation may no longer be appropriate to protect consumers. Falling electricity prices have not been seen for 100 years. For this report we simply looked up the amount of energy each country used, and looked at its current rate of change and intelligently projected it to 2050, taking into account where it was visible, any long term saturation to the density of electricity used per person. We considered if further in- dustrialization was likely and set a growth rate for general purpose elec- tricity usage via the grid. We forecast each country based on what governments have promised the IPCC in terms of renewables and emissions, except where we felt those numbers are not geopolitically possible, and decided what would be the remaining energy sources on a least cost basis, and based upon existing governmental and industrial preferences. This way we could track the de- clines of gas and coal, and the relative frozen level of nuclear and hydro in the mix, leaving much of the responsibility for growth on renewables. Methodology

- 8. Copyright © 2021 Rethink Research, All rights reserved. 8 We then forecast the transition of each of home heat, electric vehicles, steel making and cement making based on the size of these markets now and to 2050 in each country, and tried to work out the size of the additional elec- tricity resources this would require. In many ways that is the point of this report, to put some form of upper limit on the ambition of these transitions. We began initially focusing on 44 of the major electricity using countries, but in the end reduced this to the largest 21 and treated the remaining mar- kets as additional, and included them only in summing up global numbers. The 21 countries represent 85% of electricity usage in the world. In some sense this is about creating a model that shows the level of ambition for governments and the renewables industry, and its investors and sets an anticipated “pace” that ambition can be measured against. We have not tried to quantify air and ship travel, or CO2 reduction from changed farming techniques or tree planting, and in particular we have not assumed any freeing up on existing electricity supplies due to energy effi- ciency, although these will certainly be considerable, where they occur. We understand that what we have done is an over-simplification of a very difficult task, building a global energy model, that almost anyone can afford to buy, but more than anything it is a refutation of all “primary” energy cal- culations used by fossil fuel companies, and it provides a way of putting every problem into the universal language of electricity generation. Throughout this report we have assumed that almost ALL industrial “extra” were provided through hydrogen, certainly in cement manufacture, but also in other metals and some in steel production. But we have only fo- cused on the electricity to make the hydrogen, so have no forecast the num- ber of electrolysis GW that are installed, which we shall leave to other re- ports. Also throughout this report we assumed that the renewables mix, which to- day is roughly one third wind, one third solar and one third other, has come to rely more on Wind and solar, with an aggressive growth curve for geo- thermal, as a partner technology. Naturally this has necessitated an enor- mous amount of stationary battery to support wind and solar.

- 9. Copyright © 2021 Rethink Research, All rights reserved. 9 Who should buy this report? Everybody who has anything to do with the creations of electricity, who’s fate is currently tied up with the future of the oil and gas indus- tries, every investor in any kind of energy and every venture capitalist that does not want to miss out on the coming energy transition, needs to read this report. We would encourage all utilities at C suite executive levels to read it too, and their strategic planning team, energy regulators, renewables vendors and government departments – to also read this report It is why we have made it extra affordable: For $2,300 (for 1 to 5 people), we will give you access to every report, webinar and podcast we produce in the next 12 months, as well as from the last 12. We will also throw in an annual subscription to our Weekly Analysis. That same is true at $3,800 for a corporate license, for any number of subscribers above 5.

- 10. Copyright © 2021 Rethink Research, All rights reserved. 10 Rethink Energy: Taking a different view of the energy transition Rethink Energy is our energy service, made up of our Weekly Analysis ($595 on its own) and a series of “breakthrough” forecasts which show the true rate at which the Energy Transition is happening. So far mostly US based research groups pick away at renewables, energy storage and hydrogen as if they are “nice to have” which can co-exist with oil, gas and coal – they cannot. These research firms are overly influ- enced by fossil fuel thinking. Rethink Energy is the only forecaster that can see quite clearly how the energy markets are like a circle of dominoes – push one and they all fall over. It is very different forecasting a market that is on the edge of a precipice, compared to one which is on a flat hilltop. This year we have issued reports on how gas assets will inevitably be- come stranded; a forecast on how the US acceleration in energy storage will trigger a global uptake of the technology; how multiple “Tesla” style visionary businesses will dominate post transition stock markets; a fore- cast for global offshore wind, and two tracking statements of where we are in Wind and Solar global installations. In all of these cases, we see the energy transition accelerating, not stalling. We see fossil fuels on death row. Our latest report is entitled, “Look Back in Anger”. Buy it here. Previous forecasts include; • Perovskites poised to disrupt solar supply chains everywhere • Wind accelerates past nuclear, hydro in post Covid power markets • What a difference a day makes; Biden win triggers solar acceleration • Europe goes all in on hydrogen for the transport economy • Energy through the looking glass | What stock markets look like on the other side of the energy transition • USA flying start triggers rush for Energy Storage leadership

- 11. Copyright © 2021 Rethink Research, All rights reserved. 11 RETHINK LEADERSHIP RETHINK ENERGY’S MAIN CONTRIBUTORS Peter White - Principal Analyst peter@rethinkresearch.biz +44 (0)7734 - 037414 Harry Morgan - Analyst harry@rethinkresearch.biz +44 (0)117 329 1480 Andries Wantanaar - Author andries@rethinkresearch.biz Peter White - CEO and Co-founder peter@rethinkresearch.biz +44 (0)117 925 7019 Caroline Gabriel - Research Director caroline@rethinkresearch.biz +44 (0)207 450 1230 www.rethinkresearch.biz

- 12. Copyright © 2021 Rethink Research, All rights reserved. 12 Rethink is a thought leader in quadruple play, renewable energy, and 5G wireless. It offers consulting, advisory services, research papers, webi- nars, plus three weekly research services; Wireless Watch, a major influ- ence among wireless operators and equipment makers; Faultline, which tracks disruption in the video ecosystem, and OTT video, Rethink Ener- gy, which monitors investment opportunities in the changing energy landscape. About Rethink Technology Research Need more information? Natalia Szczepanek (Marketing and Client Relations Manager) natalia@rethinkresearch.biz +44 (0)117 925 7019

- 13. Copyright © 2021 Rethink Research, All rights reserved. 13 Bristol & Exeter House Lower Approach Road Temple Meads Bristol BS1 6QS United Kingdom Tel. +44 (0) 1173 291480 Tel. +44 (0) 1179 257019 www.rethinkresearch.biz Published March 2021