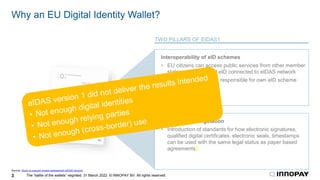

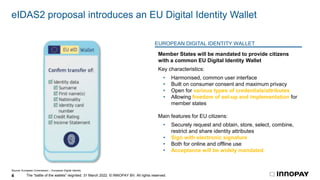

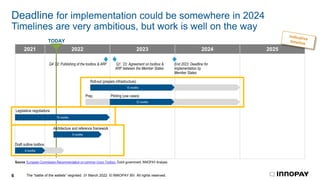

The EU is developing an EU Digital Identity Wallet that will standardize digital identity across Europe. The wallet will be mandated for acceptance by public and private sectors. It restricts third party digital identity services and data custodians. While aiming to harmonize digital identity, it may fragment the landscape due to different national implementations. Banks and other organizations should prepare for its impact on digital identity and data management in Europe.