Downloaded 20 times

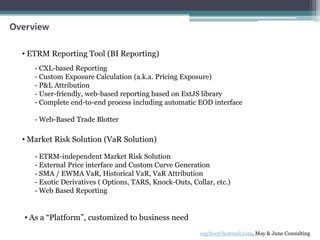

The document describes an ETRM reporting and market risk management solution including: - A BI reporting tool for market data, exposures, P&L, trades, and operations from an ETRM system. - A market risk solution for curve generation, VaR calculation, reporting, and structured derivative valuation. - The system architecture uses Oracle databases, HTTP server, and R for calculations, with a web interface for reporting, simulation, and risk management. - It has been in use since September for daily exposure, P&L, and VaR reporting.