Download to read offline

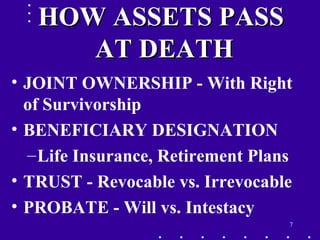

Estate planning is simpler than many young couples think. It involves planning for death, disability, asset protection, and advanced tax planning. The definition of estate planning is helping solve problems clients don't know they have in a way they can understand. Even those who think they have everything planned with a simple will may benefit from revisiting their plan as family and tax circumstances change over time. Effective estate planning requires understanding how assets pass at death and how property is taxed.