Download as PDF, PPTX

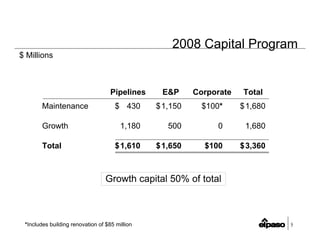

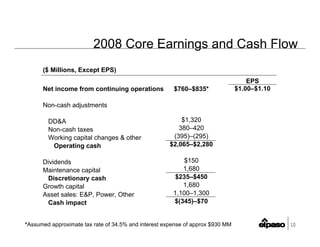

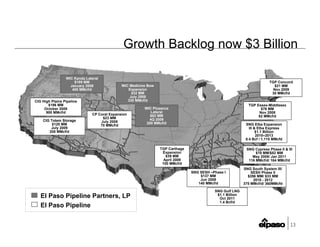

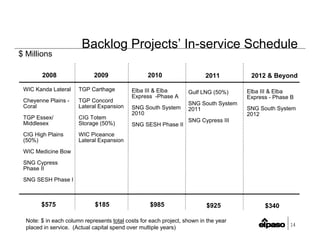

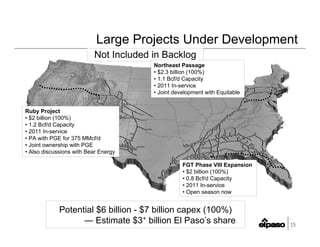

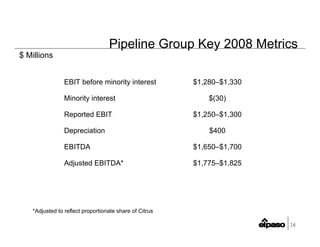

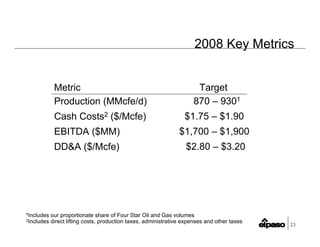

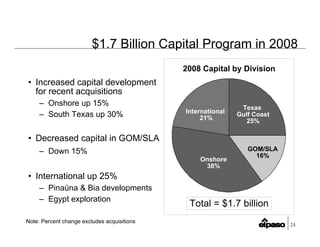

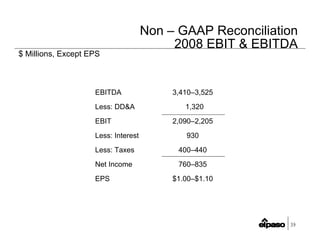

The document provides guidance for the company's 2008 financial year. It summarizes the company's accomplishments in 2007, including reducing debt by over $2.5 billion. It outlines the company's assumptions for 2008 including natural gas and oil hedge positions. The document discusses the company's 2008 capital program and core earnings and cash flow estimates, forecasting net income between $760-835 million and discretionary cash between $235-450 million. It also summarizes the pipeline business unit's accomplishments in 2007 and growth backlog increasing to $3 billion.