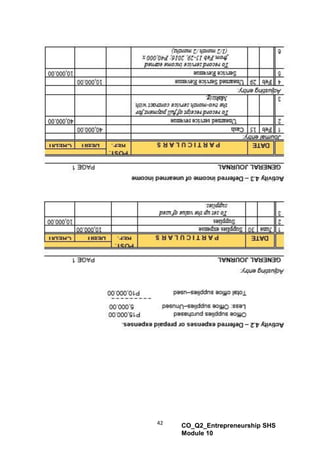

The document is a module for Grade 12 students on bookkeeping within the context of entrepreneurship, outlining concepts, principles, and processes necessary for developing a business plan and understanding market dynamics. It includes a structured approach to learning key bookkeeping tasks, such as recording transactions and preparing financial statements, divided into lessons and assessment activities. Additionally, it provides definitions and frameworks regarding accounting entries, asset management, and the roles of debit and credit in bookkeeping.