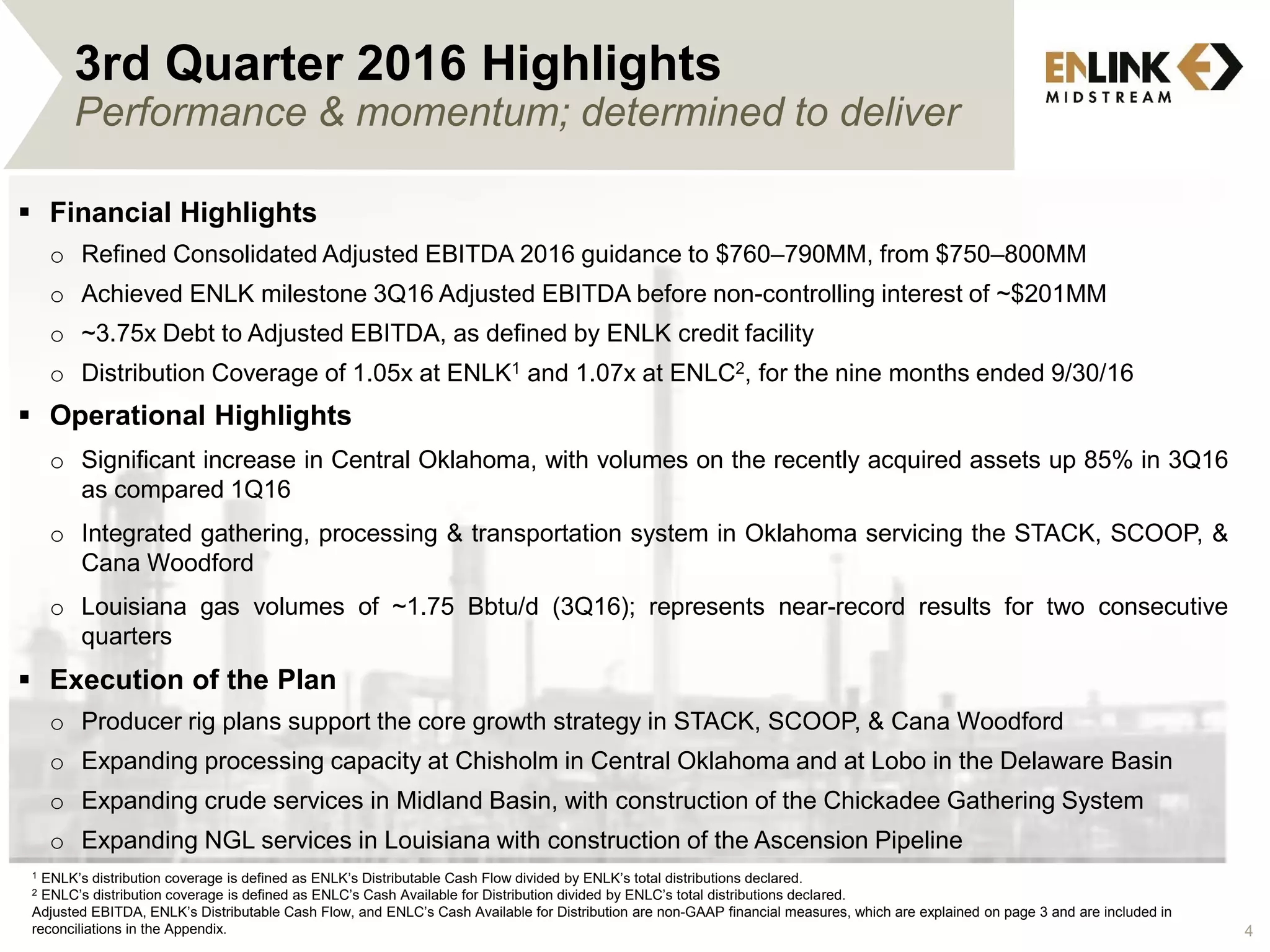

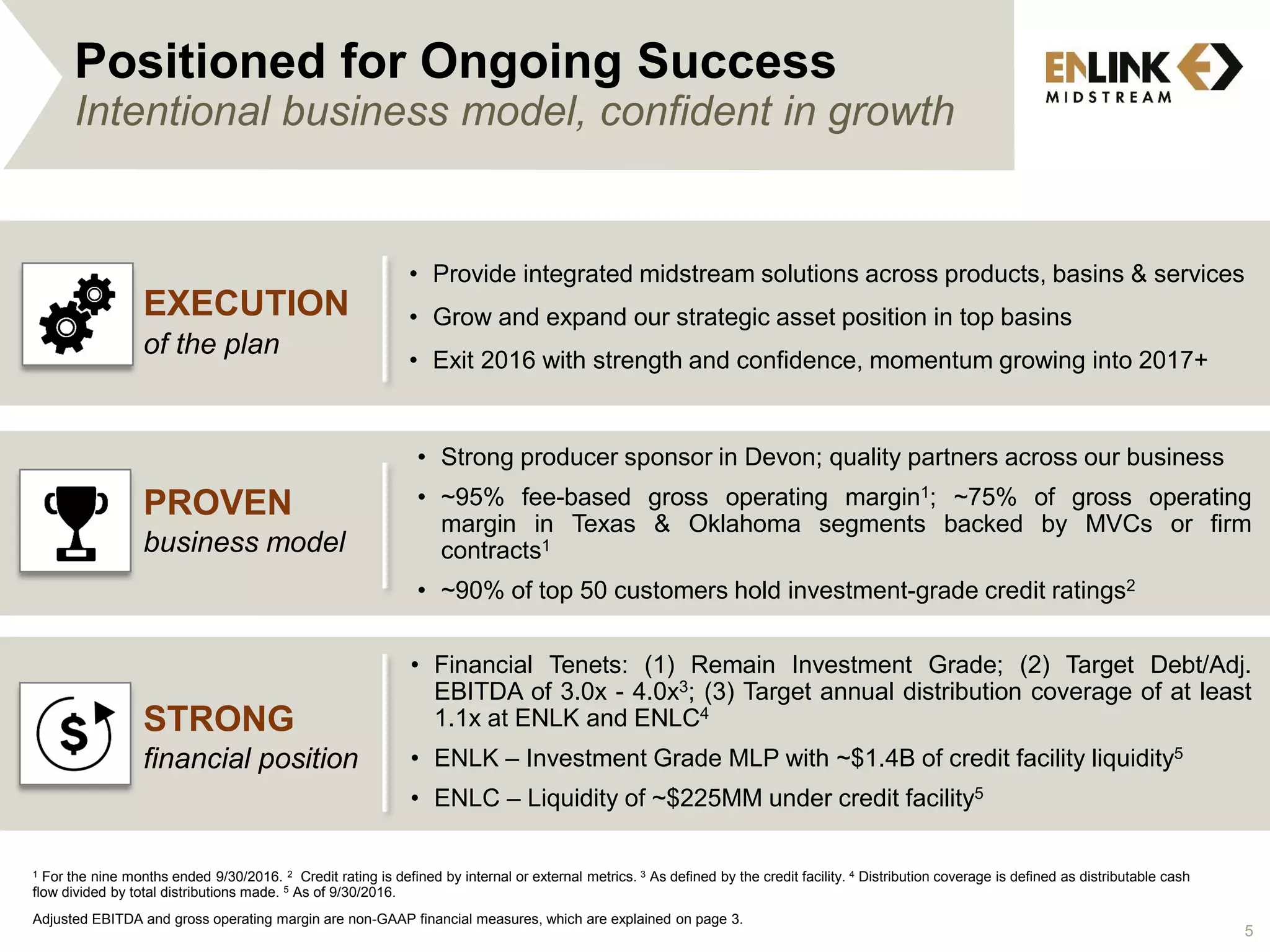

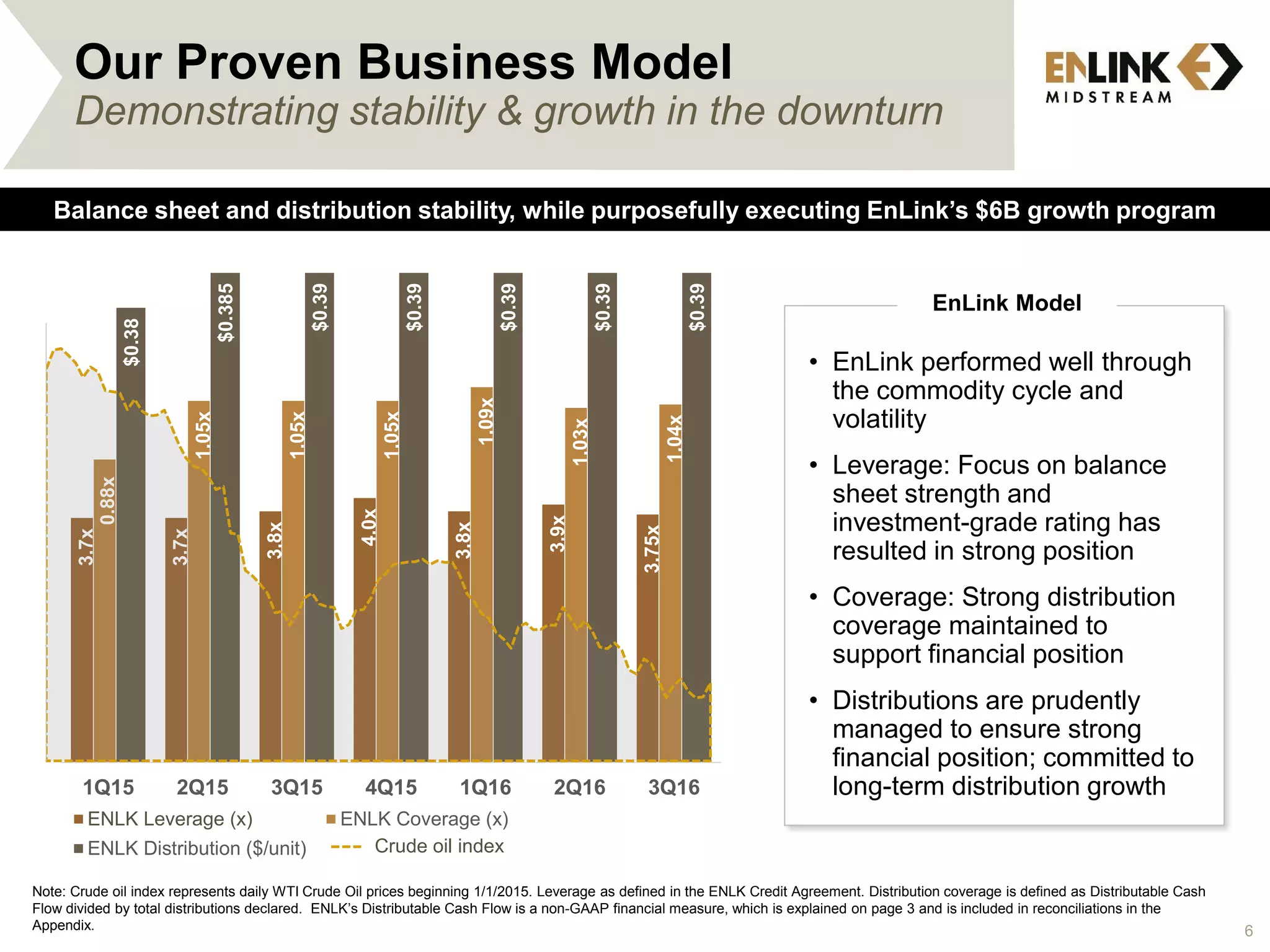

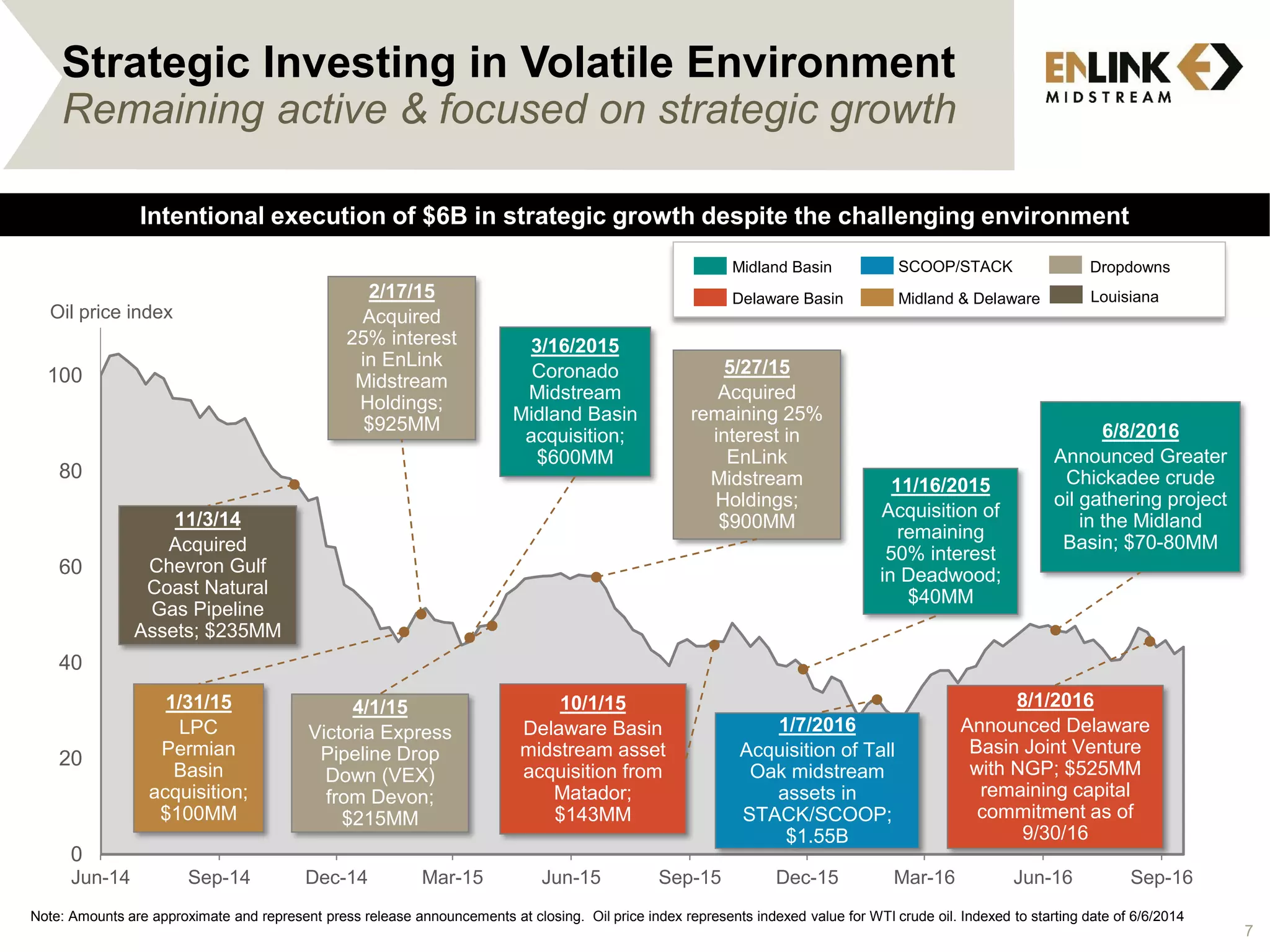

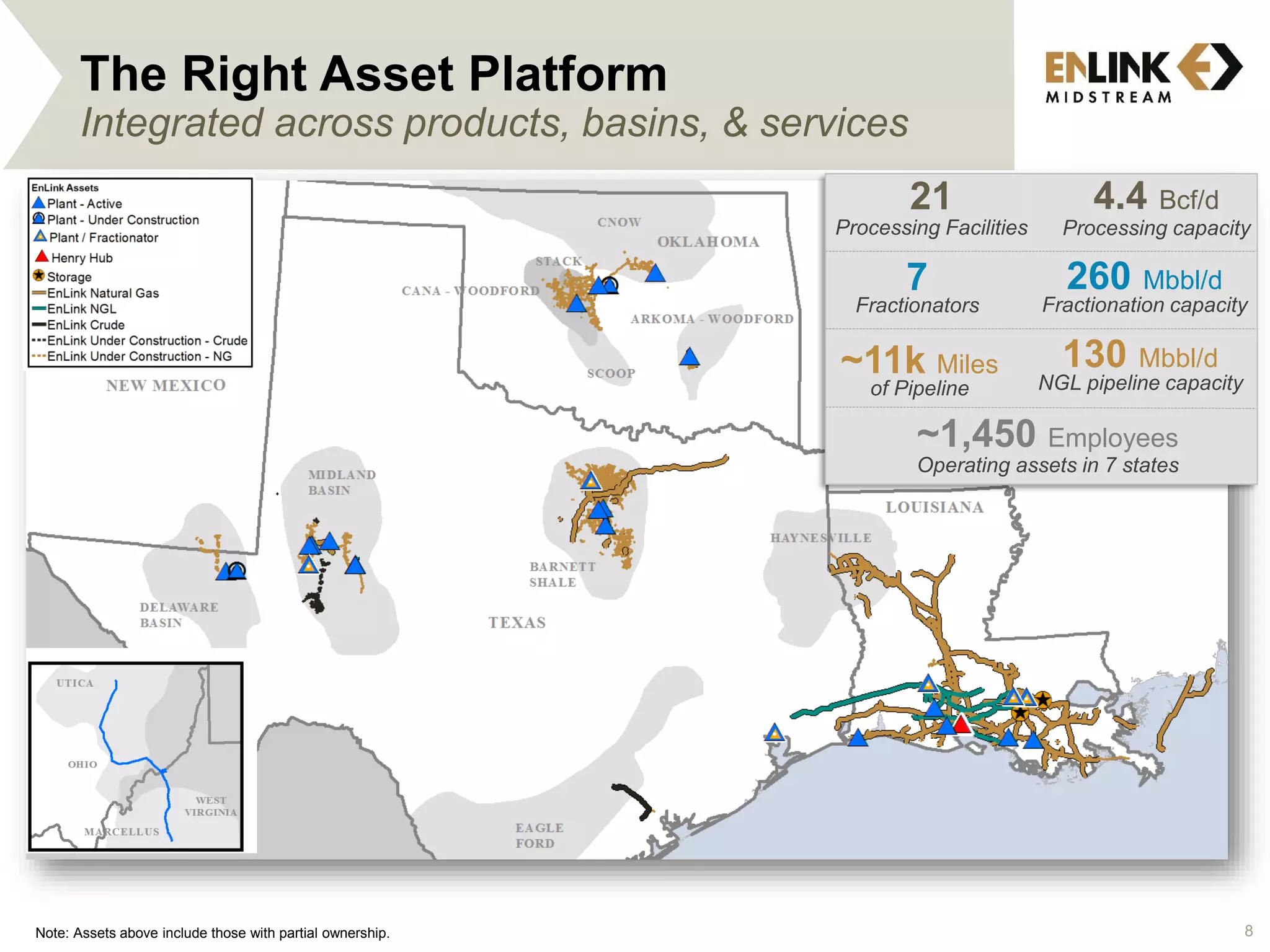

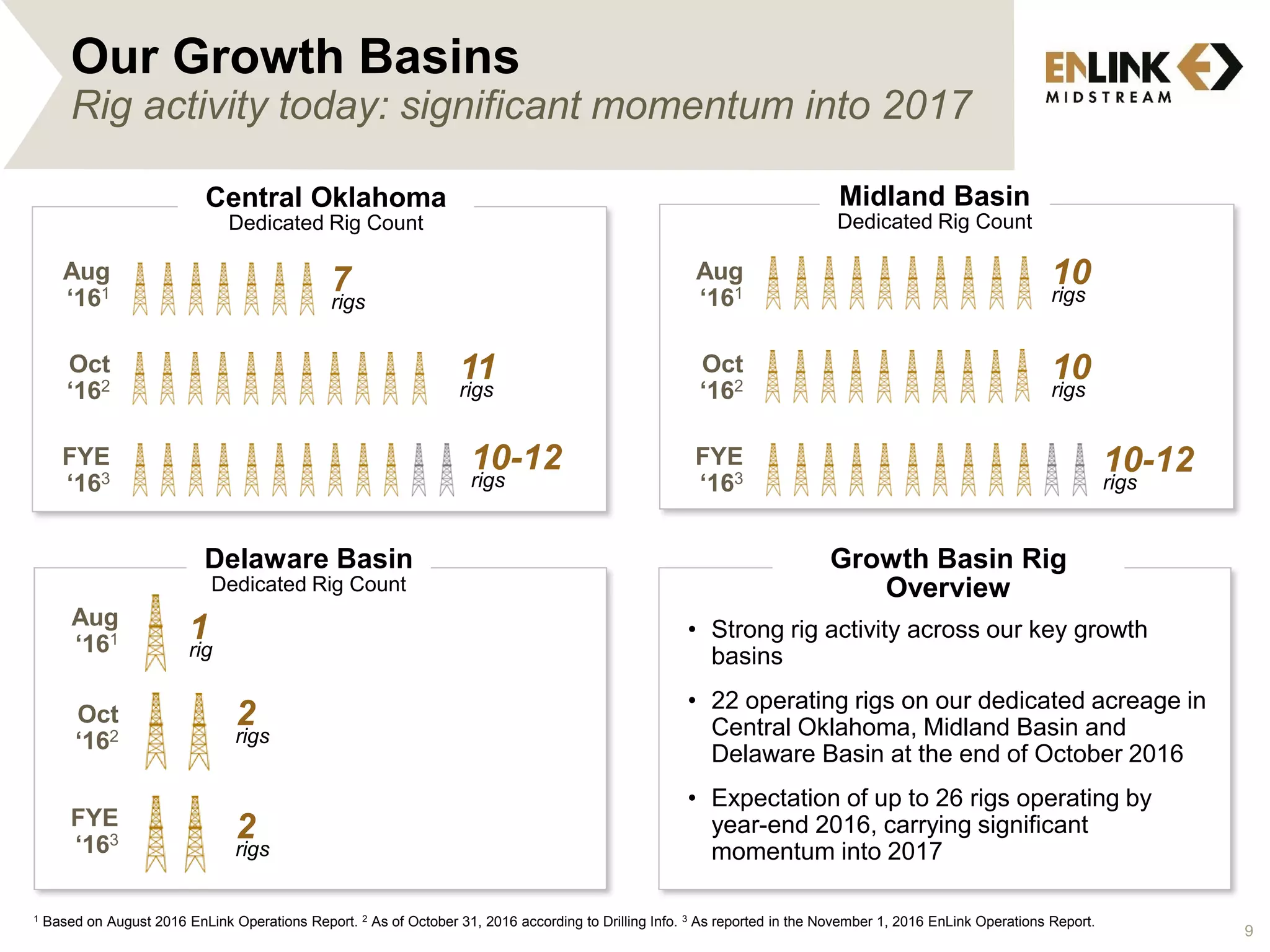

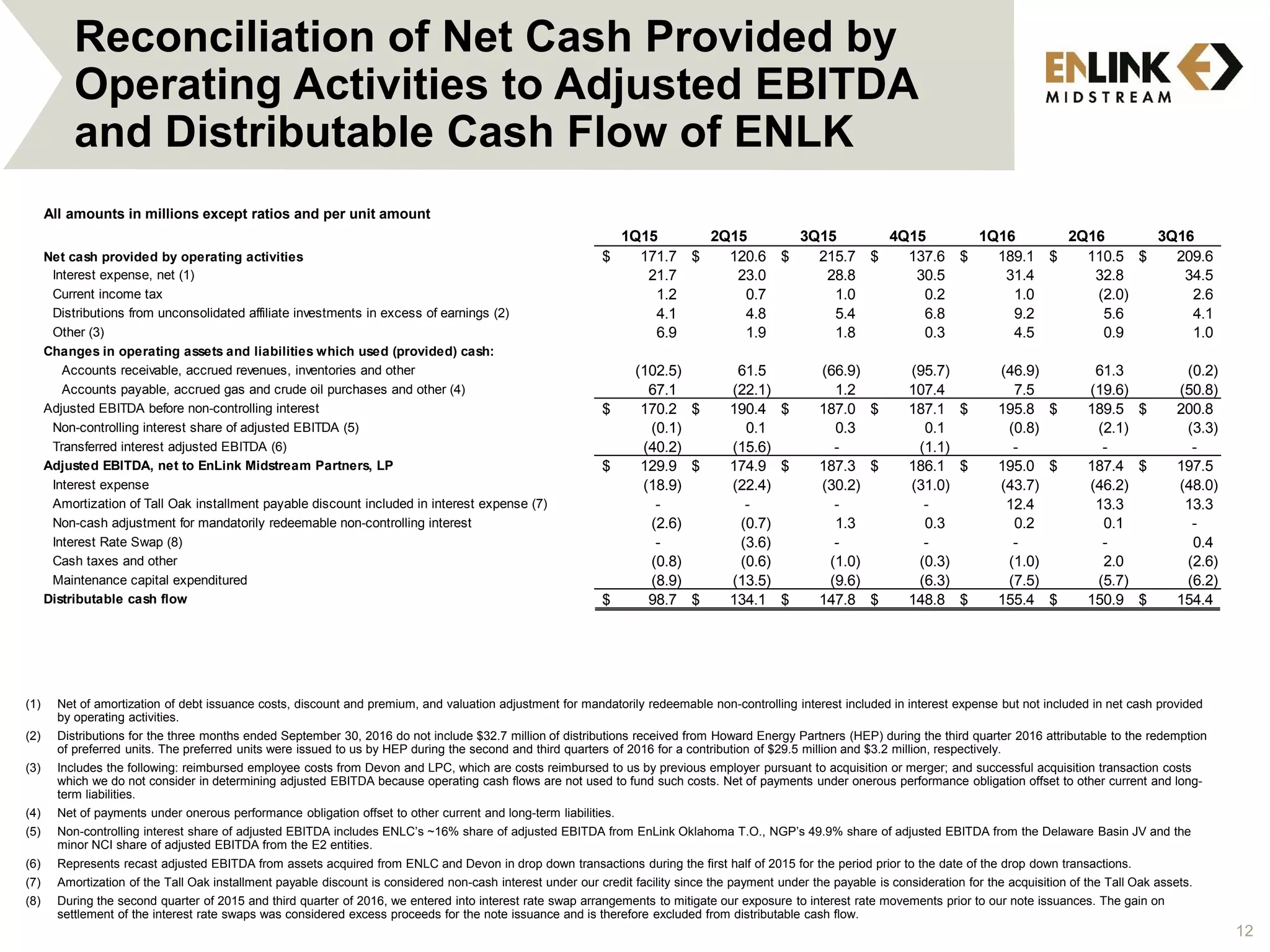

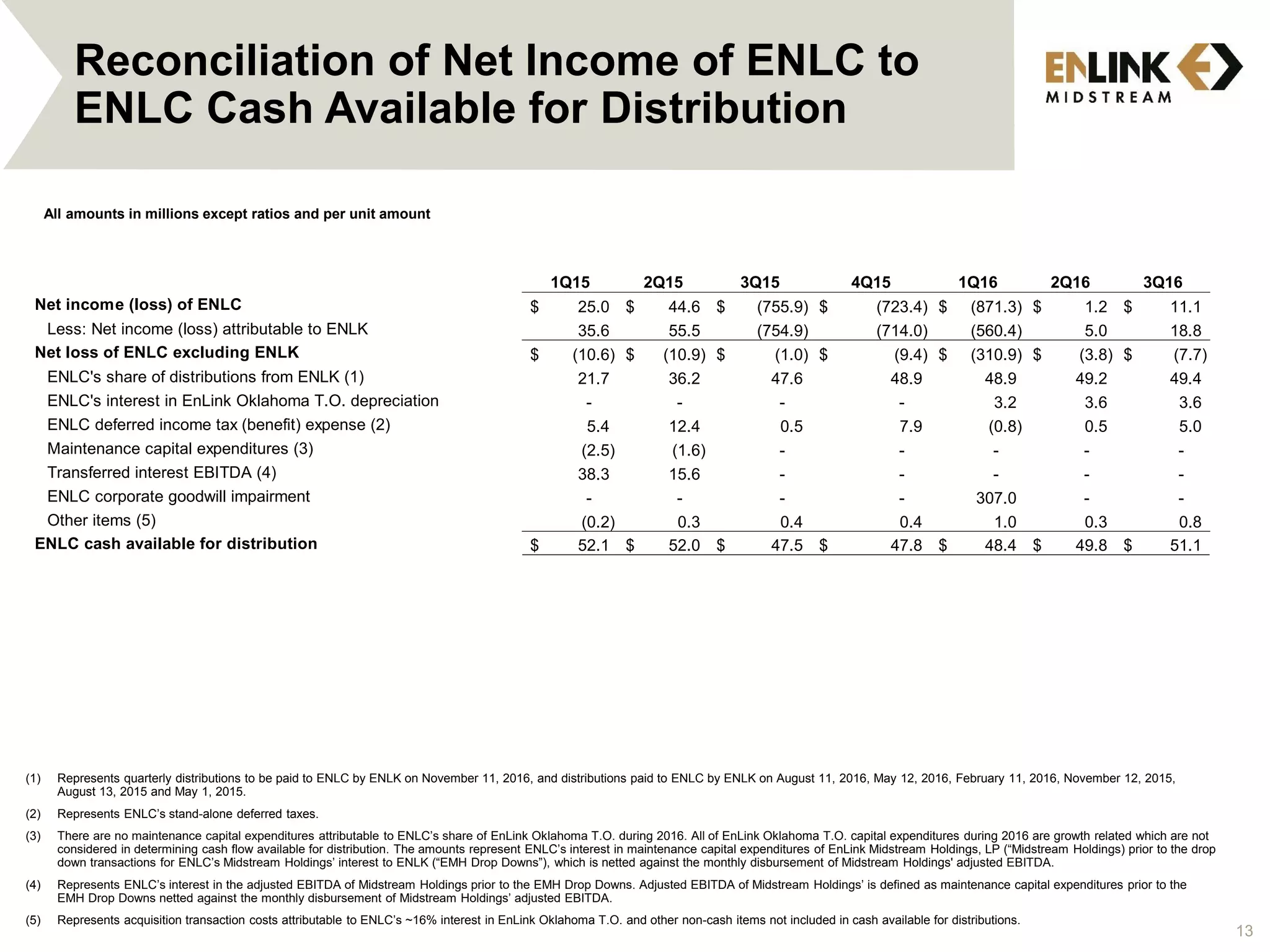

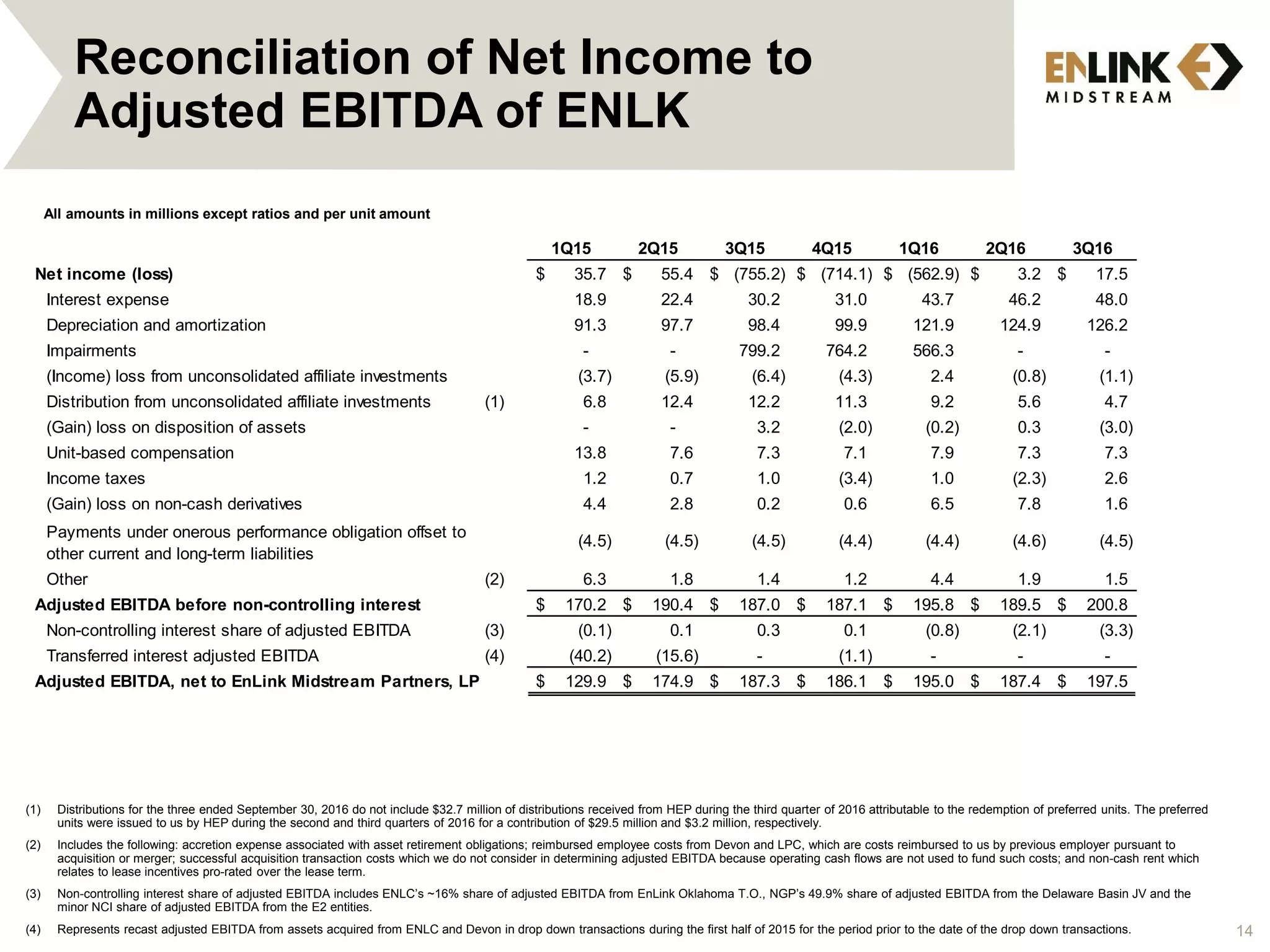

This document provides an overview of Jefferies Energy Conference and includes forward-looking statements and notices about the presentation. It discusses EnLink Midstream's 3rd quarter 2016 financial highlights including refining their consolidated adjusted EBITDA guidance range to $760-790 million, achieving approximately $201 million in adjusted EBITDA before non-controlling interest for ENLK in 3Q16, and a debt ratio of approximately 3.75 times. It also includes notices about non-GAAP financial measures used and forward-looking statements.