Downloaded 24 times

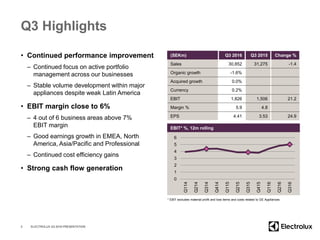

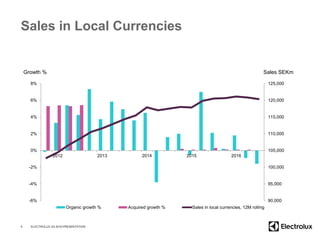

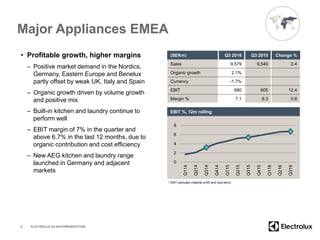

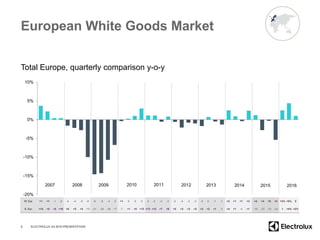

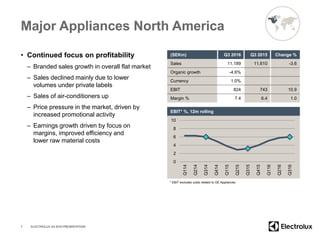

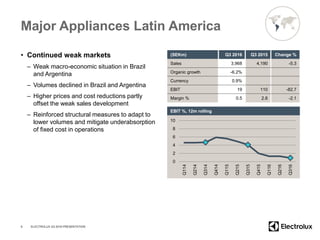

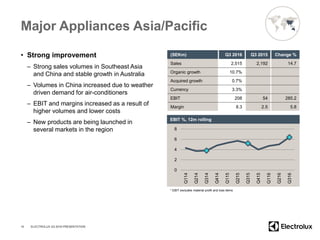

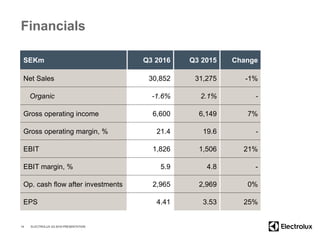

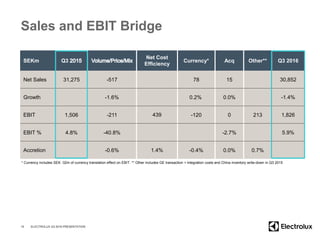

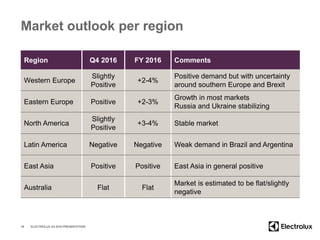

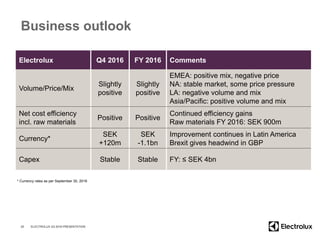

In Q3 2016, Electrolux reported a sales decline of 1.4% compared to Q3 2015, with strong performance in EMEA, North America, Asia/Pacific, and professional products, while Latin America continued to face challenges. The company achieved an EBIT margin of 5.9%, largely due to improved efficiencies and strong cash flow generation. Although the market outlook shows slight growth in several regions, economic uncertainties persist, particularly in Latin America and Brexit-related impacts in the UK.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)