- Mobile banking is growing rapidly and is now the preferred method of interacting with banks for many customers, especially those aged 30-60.

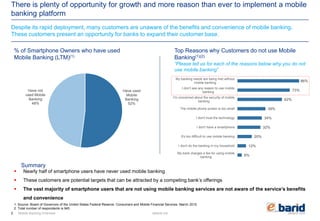

- Nearly half of smartphone users have not yet adopted mobile banking, representing an opportunity for banks to expand their customer base.

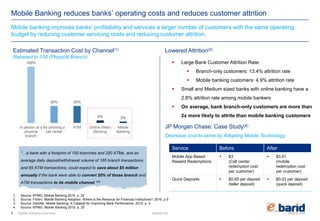

- Mobile banking improves banks' profitability by reducing operating costs through lower transaction fees and reducing customer attrition rates.