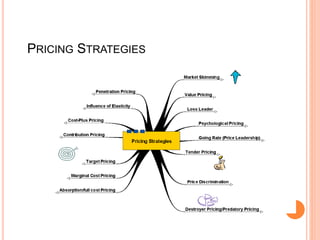

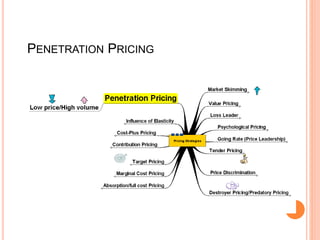

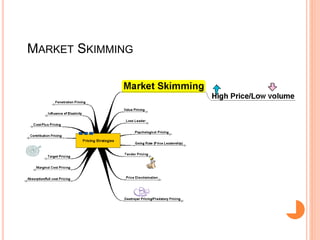

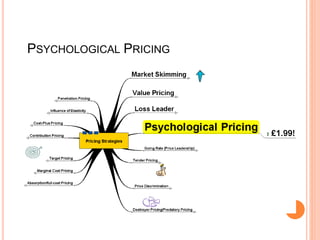

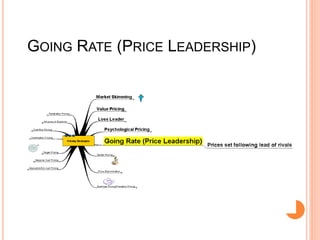

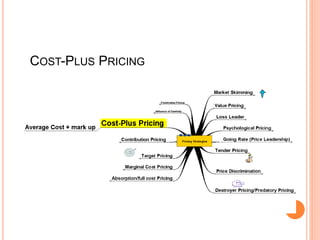

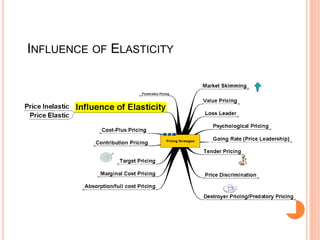

The document outlines several pricing strategies that can be used including penetration pricing, market skimming, value pricing, loss leader pricing, psychological pricing, price leadership, tender pricing, price discrimination, predatory pricing, absorption cost pricing, marginal cost pricing, contribution pricing, target pricing, and cost-plus pricing. It also discusses how price elasticity influences pricing decisions and the relationship between percentage changes in price and quantity demanded.