Download to read offline

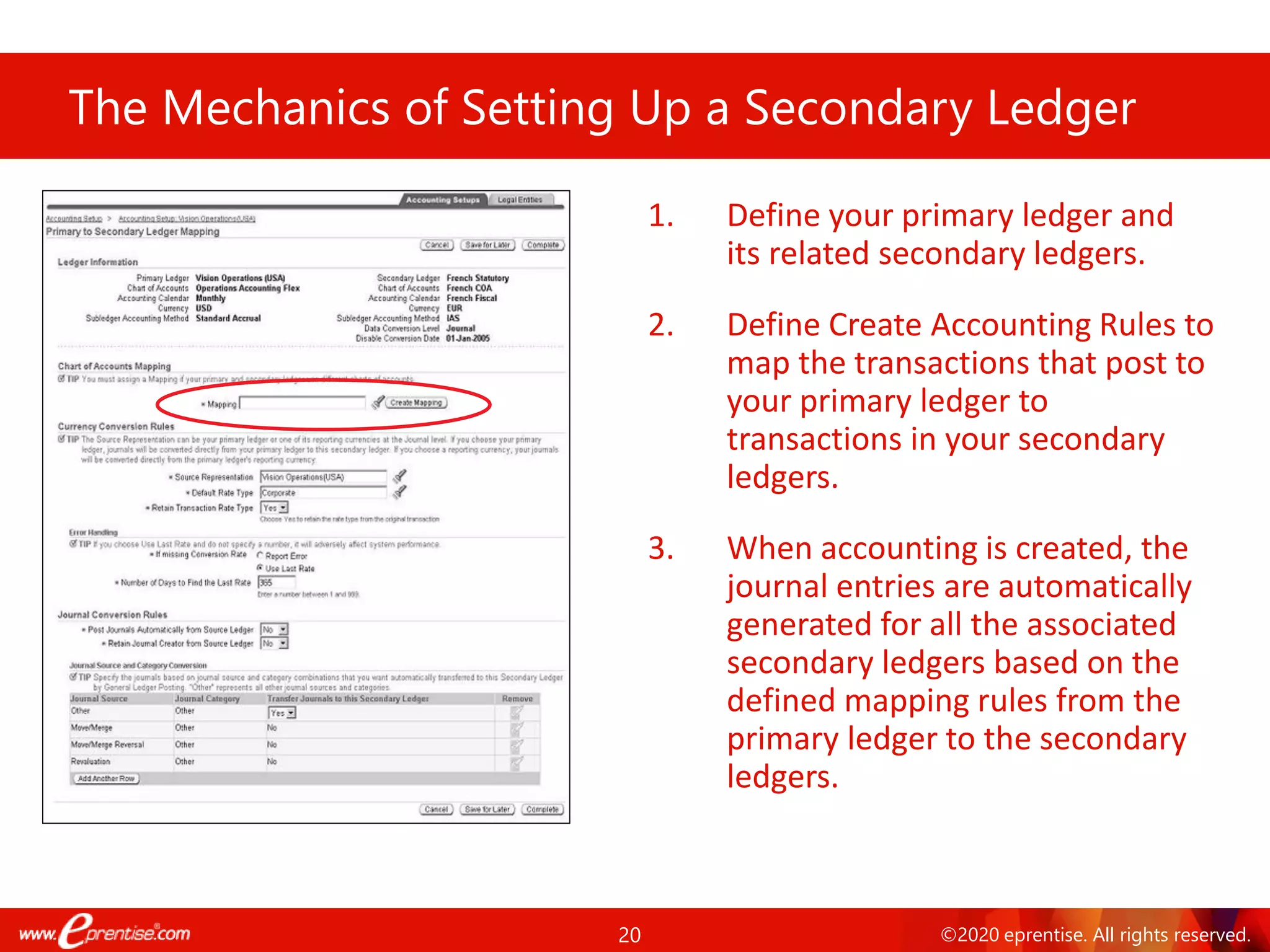

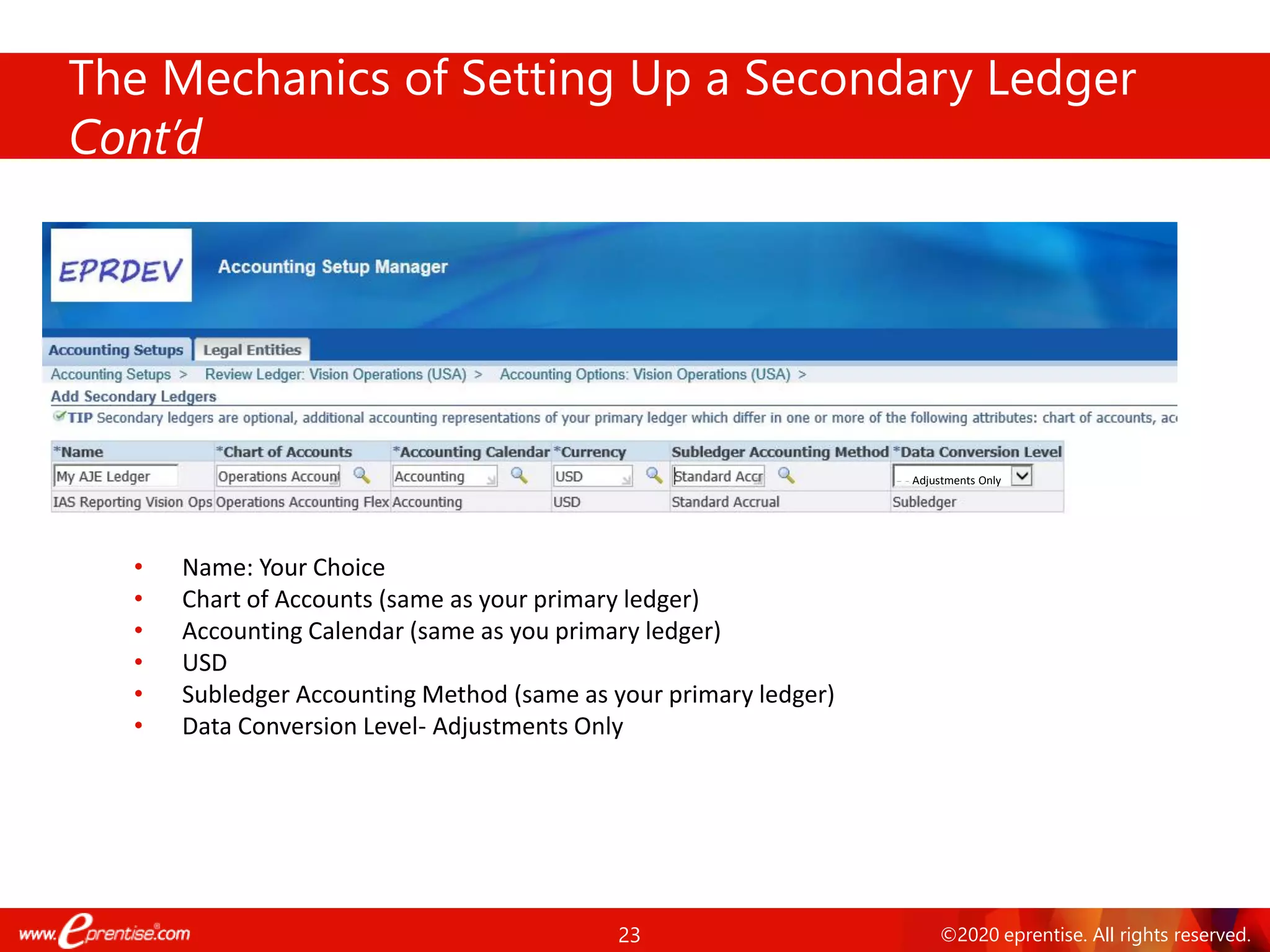

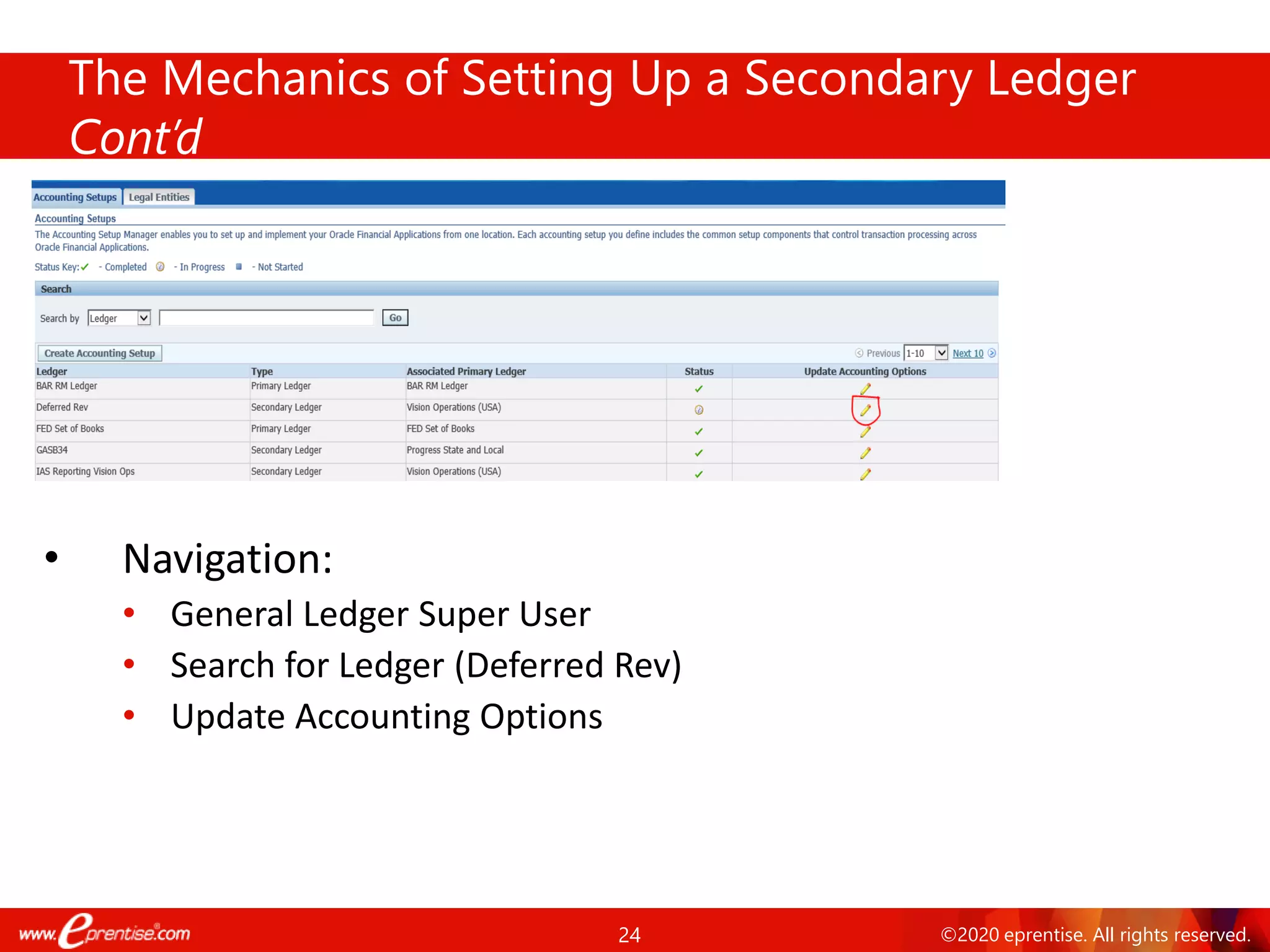

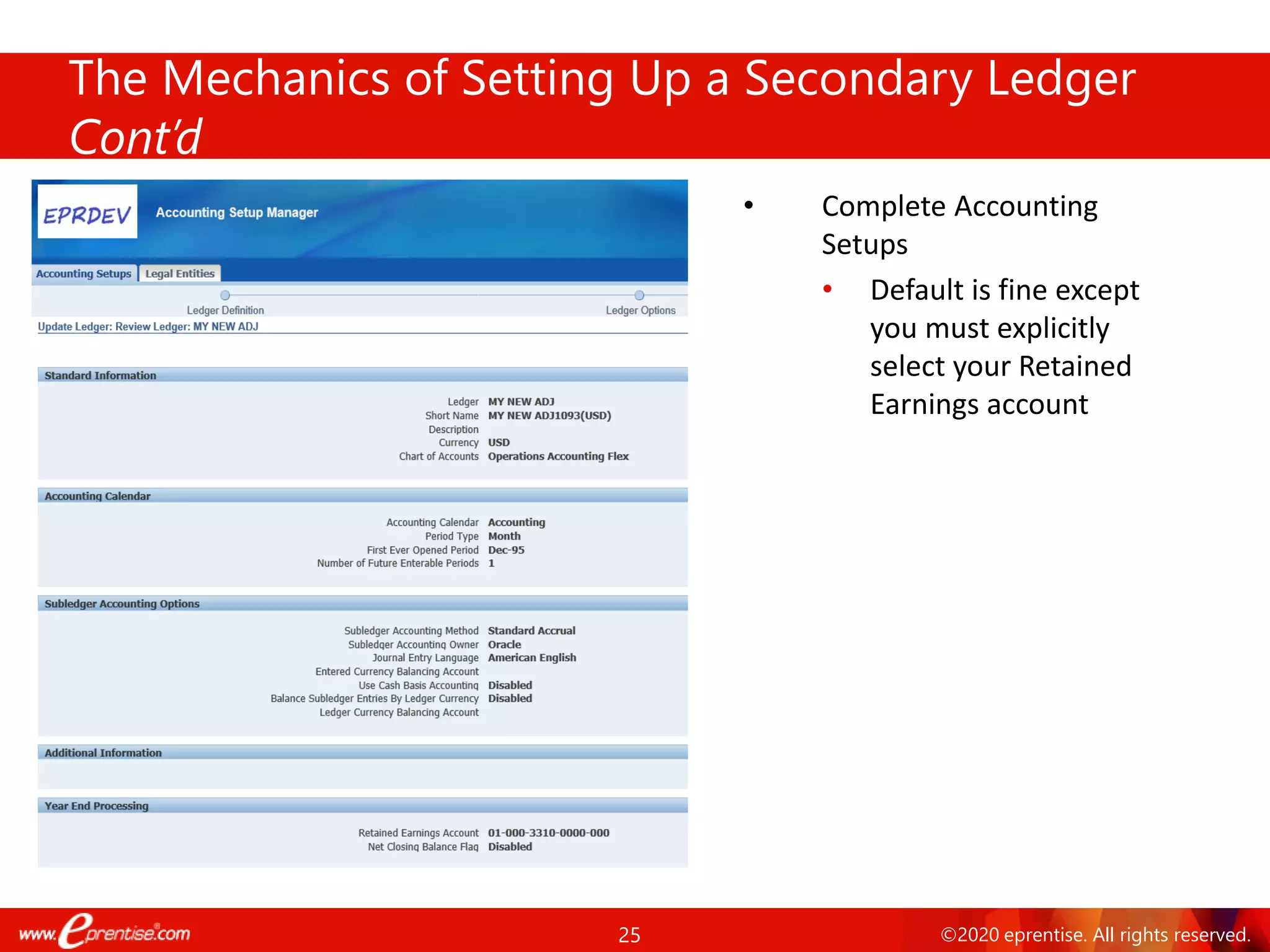

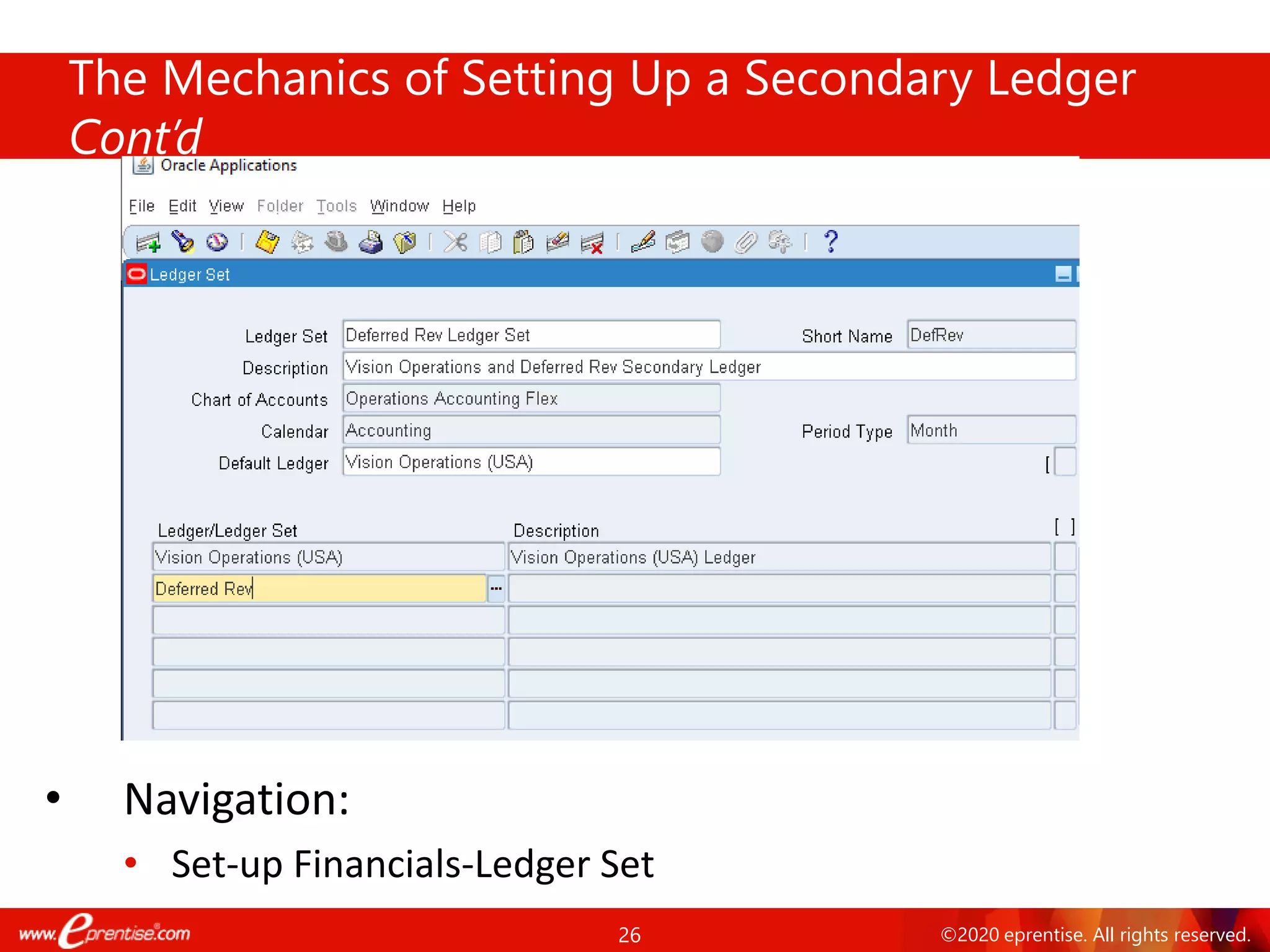

The document outlines the use of ledger sets and secondary ledgers in Oracle E-Business Suite (EBS) R12 to enhance compliance with financial reporting regulations. It discusses the mechanics for setting up secondary ledgers, the challenges of adjusting journal entries, and how these features can improve data accuracy and internal control while reducing costs associated with reporting. The overall emphasis is on leveraging these tools to streamline financial operations and facilitate statutory reporting.