Download to read offline

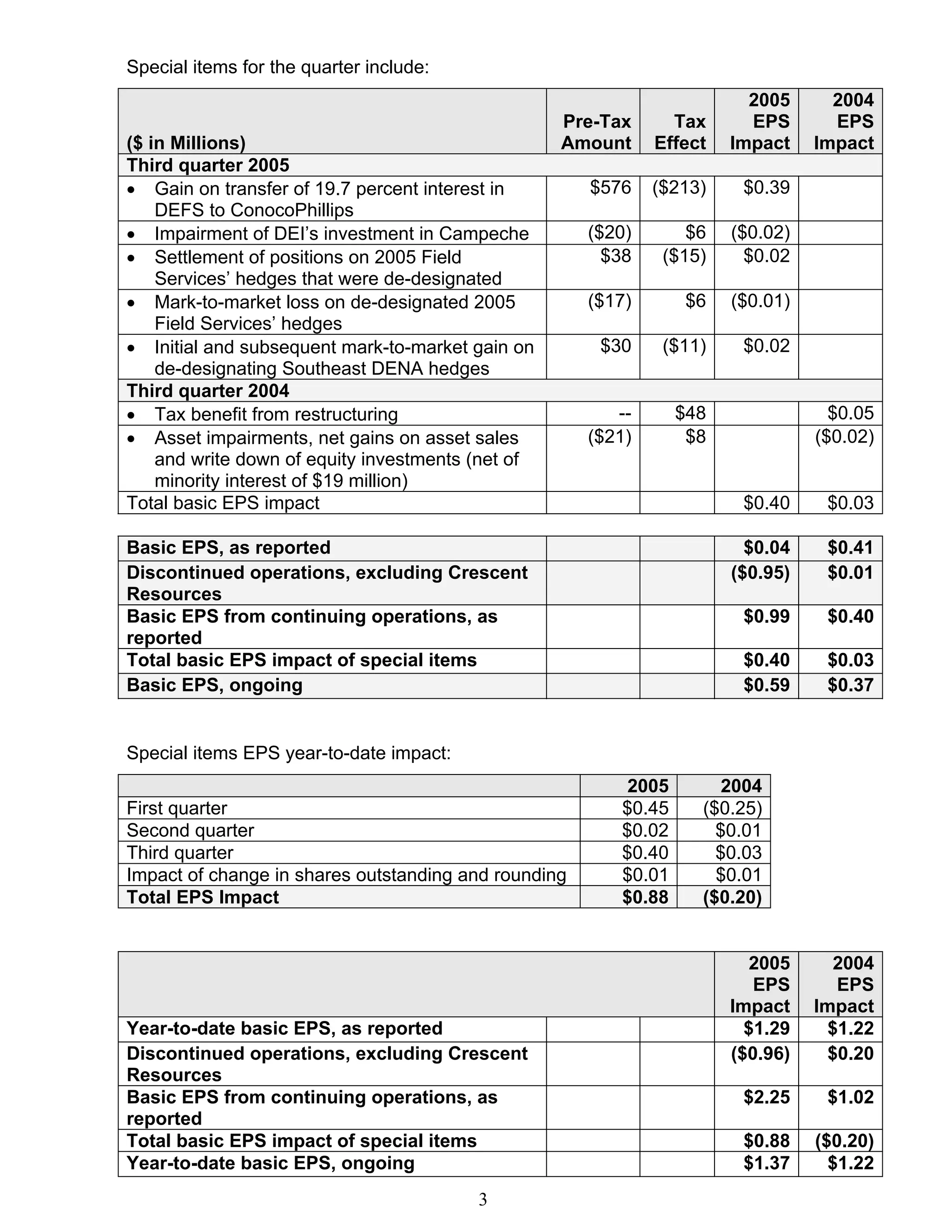

Duke Energy reported third quarter 2005 earnings per share of $0.04 compared to $0.41 in the third quarter of 2004. Ongoing earnings per share, which excludes special items, were $0.59 compared to $0.37 in the prior year. Results were boosted by warmer weather and strong performance in gas and electric businesses, but hurt by charges from exiting the DENA business. Duke Energy remains confident in exceeding its $1.65 per share employee incentive target for the year.